The Annual Tax on Enveloped Dwellings (ATED) is a tax companies and other corporate bodies must pay if they own UK residential property worth more than £500,000. However, several ATED reliefs and exemptions are available, and if they qualify, you can claim them while submitting a return.

Properties held within a corporate structure not only attract ATED but also have implications for corporation tax. It’s vital to consider how these taxes interplay to avoid unexpected liabilities.

What does ATED mean?

But what is ATED? the simple answer is that all non-natural persons (NNPs) who own homes in the UK must pay annual tax on enveloped dwellings every year. If the property value exceeds certain thresholds, it will be subject to ATED. However, individuals who own their homes personally are not required to pay this tax; it only applies to properties held by companies or other corporate entities.

When Does ATED tax Apply, and when do I file ATED returns?

ATED applies to residential properties in the UK owned by NNPs that are valued at more than the following thresholds:

- £500,000 (from 1 April 2016 onwards)

- £1,000,000 (from 1 April 2015)

- £2,000,000 (from 1 April 2014)

The property’s cost, if purchased after specified valuation dates, or its value at those dates are used to determine the taxable value.

What is a Dwelling?

Annual Tax on Enveloped Dwellings defines a house as any property that is used as a home or could be used as one. This includes properties that are still being built or converted into homes. Buildings used for living but don’t meet the ATED definition of a dwelling include hotels, boarding houses, and student housing.

ATED Rules on Filing Requirements

Starting April 1 each year, an ATED return must be made beforehand. For example, the tax return for April 1, 2024, through March 31, 2025, must be sent in on or after April 1, 2024. The tax for the time covered by the return is due by April 30 for the chargeable period covered by the return.

Smart tax planning is essential when dealing with enveloped dwellings, especially with ATED in the mix. By carefully planning and having a clear understanding of property accounting, you can make the most of available reliefs and reduce your overall tax burden.

ATED Filing Around Taxable Value and Valuation Date

To meet ATED requirements, properties are revalued every five years. These are the current value periods:

- For 2023-24 to 2027-28: The value at 1 April 2022, or if acquired after 1 April 2022, is its cost.

- For 2018-19 to 2022-23: The value at 1 April 2017, or if acquired after 1 April 2017, its cost.

- Up to and including 2017-18: The value at 1 April 2012, or if acquired after 1 April 2012, its cost.

- The Pre-Return Banding Check (PRBC) service from HMRC lets you check if your value is correct.

When managing properties within a company structure, known as enveloped dwellings, it’s vital to grasp the impact of the Annual Tax on Enveloped Dwellings (ATED). But just as important is considering how a simple assessment can influence your overall tax returns. Such assessments can uncover opportunities to claim reliefs, optimise tax efficiency, and ensure compliance with general tax obligations and those specific to enveloped dwellings

HMRC Self-Assessment: How Simple Assessments Impact Your Tax Returns

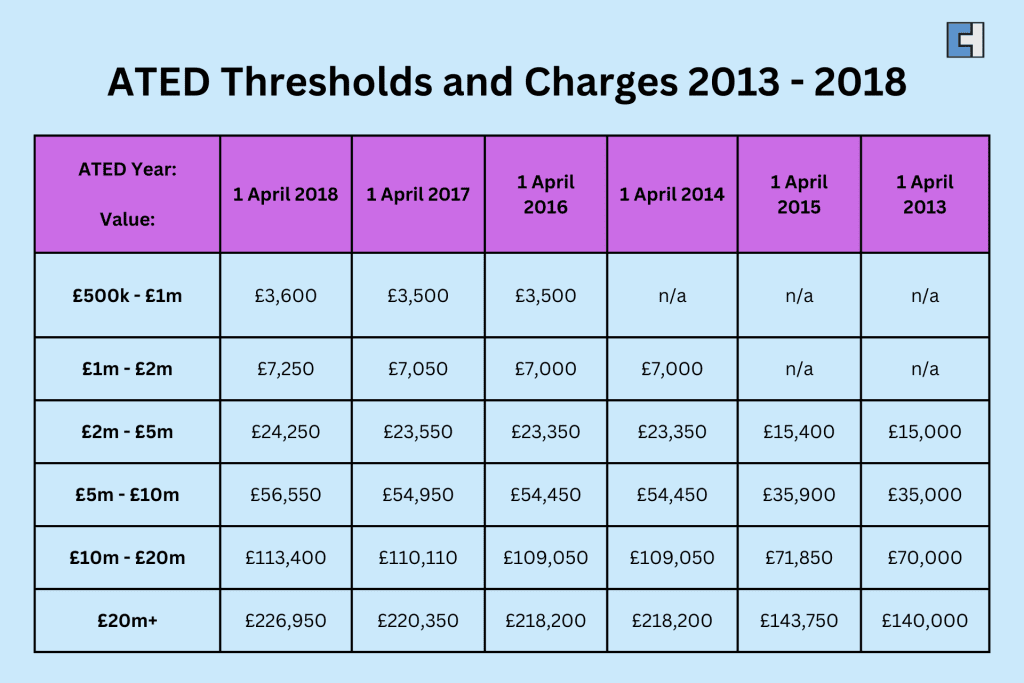

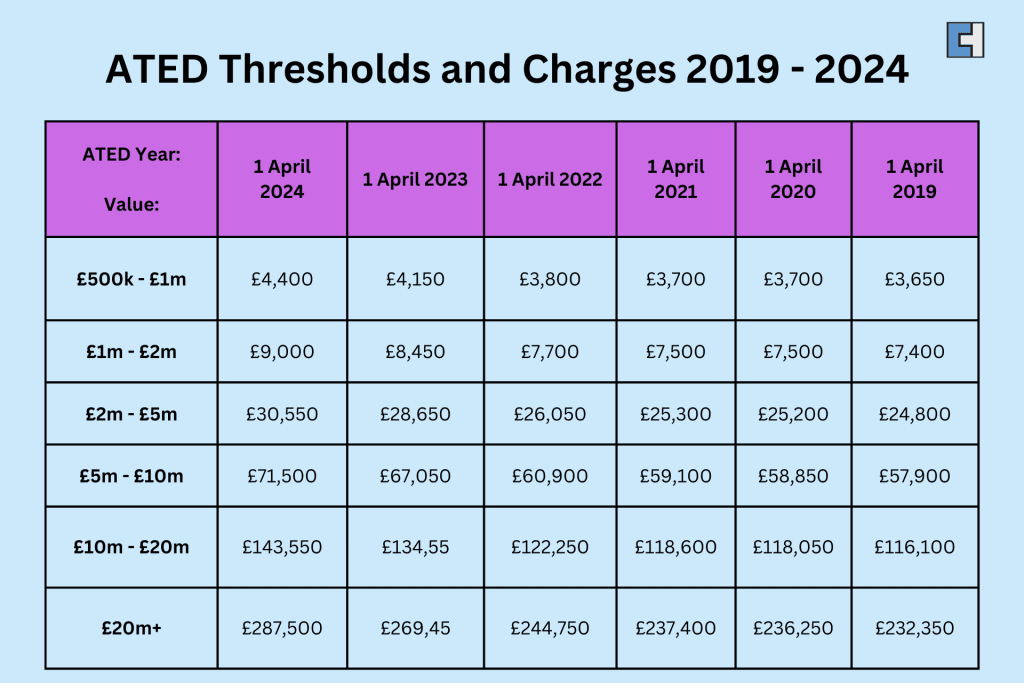

ATED Thresholds and Charges

The ATED charge is based on the property’s taxable value, and rates rise over time.

The table below shows how much the annual ATED fees are based on the different bands of valuation:

ATED Relief and Exemptions

There are different reliefs that can lower or get rid of the ATED charge. Some of these are:

- Property developer relief: Homes that are being remodelled or that a real estate company is holding on to sell them later.

- Rental business relief: Commercial properties that property renting companies rent out to other people.

- Farmhouse Relief: Farmhouses where farmers live and work.

- Properties that trading companies own and let their employees use.

- Qualifying housing co-operatives and charitable companies exemption: Housing co-ops that meet the requirements can also get help starting April 1, 2020. There are exceptions for public bodies, national purpose groups like the trustees of the British Museum, and charitable companies that hold property for charitable purposes.

In addition to ATED exemptions, there are other exemptions and reliefs available in different areas of property tax, such as Stamp Duty Land Tax (SDLT). Leveraging these can significantly reduce your overall tax burden.

ATED Penalties

The ATED late filing penalties are the same as those in schedules 55 and 56 of the Finance Act 2009 for late filing and payment and the same as those in schedule 24 of the Finance Act 2007 for mistakes that cause a loss of tax. Following these rules is very important to avoid getting fined.

Acquisitions, Disposals, and Improvements

People who own the property or changes made to it during the ATED chargeable periods can affect its taxable value and the tax charge associated with it. You can find detailed information to ensure that these steps are taken properly.

De-enveloping

Firms can “de-envelope” properties and give them back to shareholders if they want to. It is important to give this choice a lot of thought because it will have big effects on taxes. When de-enveloping properties, it’s essential to consider the potential ATED-related Capital Gains Tax (CGT) implications. If the property’s value has increased since it was first enveloped, the sale may trigger a CGT liability. Understanding how CGT interacts with ATED can help in making informed decisions about whether to de-envelope.

As a Non-Resident Landlord, you might also want to read more about the Non-Resident Landlord Scheme and if it applies to you.

Conclusion

Businesses and other NNPs who own homes in the UK need to be aware of ATED. Your yearly tax bill can change greatly if you follow the filing rules, get an accurate valuation, and claim all available tax breaks. If you want ATED technical guidance, you can use the ATED helpline or speak to a specialist tax accountant, who will help you register for ATED, provide ATED guidance, and help you with ATED submission.

Additional Resources