The liquidity ratio is a calculation to measure the ability of a company to pay off any short-term obligations with its existing or most commonly referred to as current assets. Within the financial industry, it is also known as a measurement of how liquid a company is.

What is a Liquidity Ratio?

As mentioned above a liquidity ratio is a measurement and a type of financial ratio that helps determine a company’s ability to pay short-term debt obligations. However, this is not the only thing that it determines, the metric helps analyse a company’s liquidity in terms of its current and liquid assets and if those can help the company to cover its current liabilities.

Liquidity Ratios Definition

According to Investopedia, “Liquidity ratios are an important class of financial metrics used to determine a debtor’s ability to pay off current debt obligations without raising external capital.” The liquidity ratio determines this ability by calculating multiple factors. Another meaning of liquidity ratio is to pay the due amount of a company’s liabilities by realising the company’s existing assets to avoid any external debt or risk.

What is Liquidity in Business?

In simple terms liquidity in a business means a company’s ability to raise funds when it needs it. Though there are two factors determining a company’s financial position. Apart from its ability to turn assets into cash to pay for liabilities, it also means a company’s debt capacity. It refers to a company’s financial position of being able to service the current debt or to raise funds through any external debt.

Understanding Liquidity Ratios

Liquidity should be quick and cost-effective. Liquidity ratios are quite effective in comparative form. The analysis of these ratios can be internal or external.

For instance, the internal analysis of the liquidity ratio engages multiple accounting periods reported through the same methods. Comparison of previous periods and current operations can help analyse and track any changes in the business.

A higher liquidity ratio shows the great ability and potential of a company to cover any outstanding debts.

Alternatively, external analysis entails comparing the liquidity ratios of one firm to those of another or an entire sector. This data may be used to assess a company’s strategic positioning versus its rivals when establishing benchmark targets. Compared to other types of ratios, liquidity ratio analysis may not be as effective when looking across industries or businesses of different sizes in different geographical locations.

Why do We Need to Calculate Liquidity Ratios?

There are many reasons why analysts, business owners, and creditors need to calculate liquidity ratios. The main purpose of liquidity ratios is to measure a company’s ability to cover its short-term debts with its current assets. In other words, it measures a company’s ability to meet its current obligations as they come due.

Some of the other reasons for calculating liquidity ratios include:

To Assess a Company’s Financial Health:

A company’s liquidity position is one of the key indicators of its financial health. By calculating various liquidity ratios, analysts and creditors can get a good idea of the company’s overall financial health.

To Assess a Company’s Creditworthiness:

A company’s creditworthiness is another important factor that lenders and creditors consider when extending loans or lines of credit. By calculating liquidity ratios, analysts can get a good idea of the company’s ability to repay its debts on time.

To Assess a Company’s Risk:

A company’s risk is another important factor that analysts need to consider when making investment decisions. A company with a strong liquidity position is less likely to default on its debt obligations than a company with a weak liquidity position.

Types of Liquidity Ratios

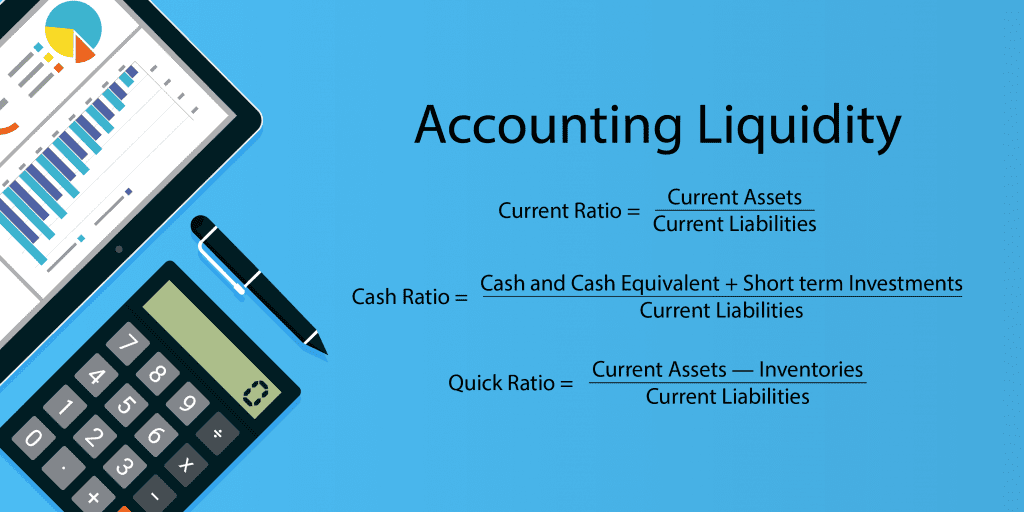

Current Ratio

The current ratio is the most commonly used liquidity ratio. It measures a company’s ability to pay its short-term debts with its current assets. The current ratio is calculated by dividing a company’s total current assets by its total current liabilities.

Current Ratio = Current Assets / Current Liabilities

Quick Ratio or Acid Test Ratio

The quick ratio is a more accurate portrayal of liquidity than the current ratio. The quick ratio, on the other hand, only takes into account a subset of current assets. Cash, accounts receivables, and Marketable Securities are included in it. The quick ratio does not take into account current assets that are less liquid, such as inventory and prepaid expenses. This makes the quick ratio a more accurate test of a company’s ability to cover its short-term obligations.

Quick Ratio = (Cash + Accounts Receivables + Marketable Securities) / Current Liabilities

Cash Ratio

The liquidity ratio is the third test of financial solvency. This calculation only considers a firm’s most liquid assets, which are cash and marketable securities. They are the assets that a company can readily use to meet short-term obligations because they are the most readily available to it.

You may consider the current ratio, quick ratio, and cash ratio as easy, medium, and hard in terms of how stringent the liquidity test is.

Cash Ratio = (Cash + Marketable Securities) / Current Liabilities

Net Working Capital (NWC) % Revenue

Net working capital (NWC) is the difference between current operating assets (cash & equivalents removed) and current operating liabilities. The NWC metric reveals whether a firm has cash tied up in its operations or enough cash on hand to cover its immediate working capital requirements.

- A positive NWC means that more cash is tied up in operations and less free cash flows.

- Negative NWC means that less Cash is tied up in operations and more free cash flows

From a liquidity standpoint, however, a negative NWC is preferable to a positive NWC. There is no specific number that all firms aim for; rather, the optimal NWC level varies based on the company’s industry and business model. Higher ratios are generally regarded negatively

The higher the NWC/Revenue ratio, the more current assets are locked up in the business. This reduces liquidity and can make it difficult for a company to collect cash payments from customers or sell off inventory.

Net Working Capital (NWC) % Revenue Formula

NWC % Revenue = NWC / Revenue

Net Debt

The net debt indicator determines how much of a firm’s short- and long-term debt obligations might be paid off right now using its current cash balance. Net debt is not a liquidity ratio (i.e., it includes long-term debt) but it is still a useful indicator of liquidity for a business.

It’s possible for two companies with an identical amount of debt in their capital structure to have different net debt balances, yet one has a lower net debt balance. This implies that this firm has more liquidity (and reduced risk) than the other.

Net Debt Formula

Net Debt = Total Debt – Cash & Equivalents

How to Calculate Liquidity Ratio?

How to Calculate Current Ratio

The current ratio is calculated as follows:

Current Ratio = Current Assets / Current Liabilities

The current ratio is calculated by dividing a company’s current assets by its current liabilities. If the existing assets are £400,000 and the existing liabilities are £200,000, the current ratio is 2:1.

Current assets are liquid assets that can be converted to cash in a year, such as cash, money market funds, account receivables, short-term deposits, and Marketable Securities. Financial obligations that are due within a year are referred to as current liabilities.

A higher current ratio is clearly best for the firm. A good current ratio is 1.2 to 2, which means that the company has 2 times more current assets than liabilities to repay its debts.

A current ratio below 1 means that the company doesn’t have enough liquid assets to cover its short-term liabilities. A ratio of 1:1 indicates that current assets are equal to current liabilities and that the business is just able to cover all of its short-term obligations.

Acid Test Ratio Calculations

The acid test ratio or the quick ratio calculates the ability to pay off current liabilities quickly. The acid test ratio or quick ratio measures how likely a company is to be able to pay off its current liabilities with its quick assets. Quick assets are current assets that can be converted into cash within ninety days. This excludes items such as inventory, supplies, and prepaid expenses.

To calculate the acid test ratio, use this formula:

Acid Test Ratio = (Cash and Cash Equivalents + Current Receivables + Short-Term Investments) / Current Liabilities

Use the following formula to calculate the acid test ratio if the balance sheet does provide a current assets breakdown.

Acid Test Ratio = (Total Current Assets – Inventory – Prepaid Expenses) / Current Liabilities

Liquid assets are a company’s cash reserves and non-liquid investments, such as term deposits. If the acid test ratio is lower than 1, it indicates that the firm does not have enough liquid assets to pay off its obligations. It implies that the business is now too dependent on inventory if the difference between the acid test ratio and the current ratio is substantial.

Since the inventory values vary across industries, it’s a good idea to find an industry average and then compare acid test ratios for the business concerned against that average.

How to Calculate Cash Ratio?

The cash ratio, also known as the cash-asset ratio, is a measure of a company’s liquidity. It tells us how much cash and cash equivalents the company has on hand to pay off its current liabilities. This information is useful for lenders and creditors who want to know how easily the company can service its debt.

The formula for calculating the current ratio is as follows:

Current Ratio = (Cash + Cash Equivalent) / Current Liabilities

If the cash ratio is equal to 1, then the business has enough cash and cash equivalents on hand to pay off all debts. If the cash ratio is less than 1, however, there is not enough money available to cover short-term debt obligations.

A company’s cash ratio is the amount of cash they have available to cover all short-term debt. If a business has a cash ratio greater than 1, it means it will still have money remaining after they pay off its debts. But, sometimes a high ratio can show that those extra funds are not being used in ways that will make a profit – like investing them in something safe instead of taking risks for higher interest rates.

What Is an Example of a Liquidity Ratio?

| Particulars | Amount |

|---|---|

| Cash and Cash Equivalent | 4000 |

| Short-term investments | 550 |

| Receivables | 1000 |

| Stock | 4200 |

| Other Current Assets | 200 |

| Total Current Assets | 8300 |

| Accounts Payable | 2200 |

| Outstanding expenses | 800 |

| Tax payable | 1100 |

| Deferred revenue | 900 |

| Total Current Liabilities | 5300 |

1. Current Ratio = Total Current Assets / Total Current Liabilities

Current Ratio = 8300 / 5300 = 1.56

2. Acid Test Ratio = (Total Current Assets – Stock) / Current Liabilities

Acid Test Ratio = 8300 – 4200 / 5300 = 0.77

3. Cash Ratio = (Cash + Cash Equivalent) / Current Liabilities

Cash Ratio = 4000 / 5300 = 0.75

From the above example, we can conclude that company ABC has a current ratio of 1.56, which means that it can pay off its current liabilities 1.56 times with its current assets. The acid test ratio is 0.77, which means that the company can pay off its current liabilities 77% with its quick assets. The cash ratio is 0.75, which means that the company has enough cash on hand to cover 75% of its current liabilities.

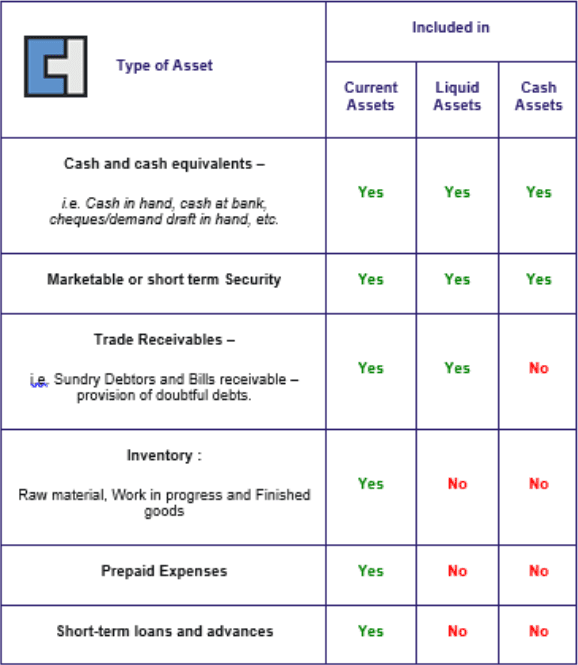

Assets Included in the Current, Liquid, and Cash Assets:

The following table will help you to understand the type of assets which are included in these assets

How to Interpret a Liquidity Ratio?

A liquidity ratio can provide one of three financial indicators, depending on which indicator is utilised.

A firm’s Liquidity Ratio is one:

When a company’s current assets equal its current liabilities, it has a liquidity ratio of one. In other words, the current assets may be used to pay off 100% of the company’s immediate short-term debt.

Liquidity Ratio of Less Than One:

If a firm’s liquidity ratio is less than one, it does not have enough cash (or cash equivalents) to meet its short-term debt obligations. For example, a liquidity ratio of 0.75 indicates that the business has only sufficient cash on hand to pay 75% of its short-term liabilities. This might be an indication of impending financial difficulties.

Liquidity Ratio Over One:

If a company’s current ratio is greater than one, it has more than enough liquid assets to cover its short-term obligations on the balance sheet. For example, a liquidity ratio of two (or the equivalent) on a financial statement indicates that the firm has enough cash assets (or the equivalent) to pay its obligations twice over.

Solvency Ratios vs Liquidity Ratios

In contrast to liquidity ratios, solvency ratios assess a company’s capacity to fulfil all of its financial obligations and long-term debts. Solvency refers to a firm’s overall capacity to pay debt obligations as well as continue operating. Liquidity is concerned more with current or short-term financial accounts; solvency is concerned with a firm’s capability to meet all of its financial obligations and long-term debts.

A company is solvent if its total assets are more than its total liabilities and liquid if its current assets exceed current liabilities. Solvency doesn’t have a direct relation to liquidity, but analyzing a company’s liquidity ratios can give some insight into expectations for solvency.

The solvency ratio lets you know if a company is bringing in enough money to cover its debts. To figure out the solvency ratio, divide net income and depreciation by short-term and long-term liabilities. A high solvency ratio means the company is more likely to be able to payback any money it owes investors.

3 Ways to Use a Liquidity Ratio

The liquidity ratios of a company can tell you several things.

1. Solvency:

Liquidity ratios are similar to solvency ratios. If a firm does not have enough liquid assets to repay short-term debt and liabilities promptly, it may be on the verge of bankruptcy.

2. Profitability:

Startups often endure debt early on, but an established business needs to be profitable to stay afloat. If a company cannot maintain a steady cash flow years in, it may not be designed for profitability.

3. Billing:

Because their customers do not pay their invoices on time, some businesses have difficulty maintaining a fair amount of cash on hand. The Days Sales Outstanding (DSO) ratio compares the volume of accounts receivable to the daily revenue a firm generates. Accounts receivable is considered a “liquidity drain” by some accounting and investment bankers, but it is important to the fast ratio, which is popular among accounting managers.

How to Improve Liquidity Ratio?

Cut Down on Overhead Expenses.

There are a number of different types of overheads that you might be able to cut down on, such as rent, utilities, and insurance. You may also consider where you’re spending your time and effort. Going paperless is one way to save time and money by eliminating the need to submit and acknowledge paper checks if your firm has a paper trail.

Get Rid Of Unnecessary Assets

Surplus business equipment can be an unnecessary financial burden. By selling this equipment, you can receive a small amount of capital and reduce the average cost of future equipment repairs.

Change the Frequency With Which You Make Payments.

If you pay ahead of schedule, negotiate special pricing with your vendors for early payments. This might save you hundreds to thousands of dollars. On the other hand, offering your consumers early payment discounts is an option.

A Line of Credit may be Beneficial for You.

A line of credit could help you cover gaps in cash flow due to payment schedules. Some business lines of credit offer access to up to £100,000 per year, with no annual fee for the first year. Doing your research and shopping around for the best possible terms is key before deciding on a lender to work with.

Re-examine Your Debt Obligations.

Switching to long-term debt might be more advantageous for you if you have short-term obligations. You may make smaller monthly payments and get more time to pay off the entire sum if you switch to long-term debt. On the other hand, converting long-term debt to short-term debt might increase monthly payments, though it also could mean your debt will be paid off more rapidly. Also Research options like loan consolidation and refinancing, which may assist in reducing monthly payments immediately while simultaneously saving you money down the road.

Conclusion

Liquidity ratios are an important part of business health. By utilizing some of the methods above, you can improve your liquidity ratio and, as a result, increase solvency and profitability while also reducing financial burdens. If you are struggling with making payments on time or you have other debt-related concerns, talk to a financial advisor to get started on a plan that will work for you.

FAQ’s

What Is a Good Liquidity Ratio?

The liquidity ratio measures a company’s ability to pay off its debt obligations. A strong liquidity ratio is indicated by a number higher than 1, which tells us that the company is financially healthy and unlikely to have any money-related problems in the near future.

A high liquidity ratio indicates that a business has a good safety margin to meet its current liabilities. Creditors and lenders often use the liquidity ratio when making decisions about extending credit to businesses.

What does high liquidity ratio mean?

A company is said to have high liquidity if it can easily pay its short-term debts, while a low liquidity score suggests that the company may soon go bankrupt.

Is a high liquidity ratio bad?

In general, a higher liquidity ratio is better than one that is lower. However, if the value is too high, it may be an indication of trouble. A liquidity ratio of 1:1 indicates that the firm has just enough of the measured liquid assets to cover all of its present obligations.

What happens when the liquidity ratio is low?

If a company has a low liquidity ratio, it may be struggling financially. On the other hand, if the ratio is very high, the company might be too fixated on liquid assets instead of reinvesting in its growth.

What causes low liquidity?

Cash and other liquid assets are required when they become short because of a liquidity crisis. A liquidity crisis is caused by widespread maturity mismatching among banks and other firms, resulting in a lack of cash and other liquid assets when they are needed. Large, unfavourable economic fluctuations or typical cyclical fluctuations in the economy may be responsible for triggering liquidity crises.