For any entrepreneur, starting an eCommerce marketplace is an exhilarating endeavour. Managing your books and your finance, if you consider yourself an expert like an ecommerce Accountant or, if you are just learning how to track your spending and income, will feel like a burden regardless of what stage you are at in your eCommerce business.

You have to wear several hats, and (for better or for worse) bookkeeping is one of them. Getting the books for your business in order is key because poor management of cash flow is one of the main factors many startups fail.

Do you want to learn your own bookkeeping? This article will teach you everything you need to know about how to keep records for an eCommerce business and how to start increasing your profits right away.

What is Bookkeeping?

In eCommerce, bookkeeping is the record of all debit and credit entries of a specific sort, such as accounts payable or payroll.

There are five basic types of accounts

| Assets | Resources, or things of value owned by a company as the result of its financial transactions, for example, Inventory & Accounts receivable |

| Liabilities | The commitments and debts a business owes to Suppliers, Banks, lenders or other providers of goods and services, for example, Small business loans & Accounts payable |

| Revenues or income | Money that a business makes from sales or rendering a service. |

| Expenses | Cash flows out of the company to pay for assets or services, for example, Utilities, Business insurance & Salaries |

| Equity | The remaining value of an owner’s interest in a company, after all, liabilities, have been subtracted, for example, Stock & Retained earnings |

The first step in small Business Accounting is to set up each account so that transactions may be recorded in the proper category. The general ledger is made up of this. Although your business needs may differ from those of an eCommerce site, you probably won’t use exactly the same bookkeeping procedures. However, numerous distinct accounting techniques are frequently used that you can use for your business.

Difference Between Ecommerce Accounting and Bookkeeping

| Bookkeeping | Accounting |

| The fundamental accounting procedure of keeping an organised record of financial records and transactions is known as bookkeeping. This technique’s goal is to categorise and arrange your financial situation. | To construct financial reports, models, and forecasts, accounting is the process of examining all the financial records that the bookkeeper has produced. in order for you to plan for the future and comprehend the state of your finances today. |

| Key bookkeeping tasks include transaction categorisation, Invoice, Account reconciliation, Balance sheet preparation, Payroll management, Account payables, and receivables management. | The main accounting tasks include Preparation of adjusting entries, Financial information audits, Tax planning and reporting, Financial forecasting and risk analysis, and Preparation of financial statements, reports, and models. |

Accounting’s main goal is to give you the financial knowledge you need to run your organisation more effectively. While Bookkeeping organises the existing data into financial statements that further enhance the accounting process. Any accountant worth their dime will tell you to get your bookkeeping foundation in order before anything else.

Importance of Bookkeeping and Accounting for eCommerce

You need a good structure to manage your money, whether you’re selling goods through an eCommerce website or not. Here are some of the essential benefits of continuously developing sound accounting procedures.

Dependable Plan of Action

Establishing a sound, workable business requires the right accounting and bookkeeping. You can clearly see how your firm operates if you have a system in place for tracking all transactions and expenses. When it’s time to pay your employees, contractors, or the duty bill at the end of the month, you can do so without experiencing any unpleasant surprises.

Determining your Business Goals

Making predictions that foretell your business’s future requires a firm grasp of your financials. Your ability to plan and work more shrewdly will improve.

Readiness of your Tax Assessment and Filing

A professional accountant will save you a ton of time and headaches when documenting your spending annually. You’ll want to maintain good financial records to ensure that your actions comply with all applicable federal, state, and local tax laws and deal charge rules. These rules don’t change; you can have an Accountant based in London or any other part of the world, and they will all tell you the same thing: keep your books in good order.

Additionally, by planning, you can collaborate with your accountant to help you attain a favourable tax outcome. If you wait as long as you can, you most likely won’t have time to complete the work intended to ensure you enhance your derivations.

What Advantages Can Bookkeeping Offer?

Here are some of the main advantages of setting up reliable accounting and bookkeeping systems and procedures, regardless of whether you sell goods through any eCommerce site or retail store

- Gain insight into your finances

- Create a more successful, sustainable, and financially sound

- Set up definite growth benchmarks

- Recognise trends and early warning signs of impending issues

- In tight or unpredictable situations, better control of financial flow

- Create projections for cash flow and inventory

- Based on verifiable information, not on your gut, run your business

- Avoid frightful tax notices, fines, and penalties

- Increase client lifetime value by utilising data

However, the biggest benefit is that it keeps your business afloat.

The Right Way to Do Bookkeeping

Make sure you do good bookkeeping if you’re going to devote time to it. Your books won’t become a mess if the tiny details are done correctly from the start.

You Have to Separate Your Business and Personal Finances

It’s challenging to keep track of your income and expenses when your finances are mixed up. A separate account makes it simple to keep track of your transactions, generate financial reports, and calculate your tax deductions. At tax time, you won’t have to wonder if the IKEA purchase was for your office chair or your home room furniture.

Select a Suitable Bookkeeping System

Simply record each transaction as income or expense and add to or subtract from your cash balance to keep track of your inflows and outflows using single-entry accounting. Double-enter accounting records for each transaction in two accounts, debit and credit, to ensure that your income, expenses, assets, and liabilities are in balance.

The consistency of your bookkeeping is more crucial than the approach you choose. Choose a strategy and stay with it.

Create a Chart of Accounts

A general ledger keeps track of your financial transactions. It makes finding transactions simple without having to sift through your bank and credit card statements. It can be further divided into sub-ledgers for transactions involving assets, liabilities, equity, revenue, and expenses. To ensure that you and your accountant don’t get lost in the future, identify the sub-ledger names and purposes in a chart of accounts.

You Should Have All the Things on the Record

Record every transaction, regardless of how big or small, frequent or irregular. Yes, that includes the coffee you purchased using corporate funds while on a work trip. Organise your expenses into categories with distinct, clear tags to see trends in cash inflow and outflow.

It is recommended to keep the receipts and invoices of the last six years, but your business might have other requirements and the necessary documentation to keep a record of. In that case, your accountant can help you identify those documents, or you can hire professional accountants.

Constant Attention

Maintaining consistent and continuous attention to it makes bookkeeping easier. When you’ve allowed stuff to accumulate for weeks or months without being attended to, cleaning up can be difficult, much like keeping your home tidy. To close your books at the end of each work day, week, month, quarter, and year is a good practice to get into. This habit keeps your funds organised and enables you to identify mistakes early on.

Create financial reports (income statement, balance sheet, and cash flow statement) every month and every three months to track the development and trends of your company.

What Does an eCommerce Bookkeeper Do?

A bookkeeper ensures that your financial records are up to date, that transactions are correctly categorised, and that financial reports are sent on schedule.

When it comes to hiring a bookkeeper, you have many options number one, you can hire one in-house as a full-time employee, use a freelance bookkeeper, and last but not least, work with professional bookkeeping services providers like Clear House Accountants.

You can experience some unease over the hiring procedure; this is plausible!

The services that accountants and bookkeepers provide are very different from one another. Depending on your abilities and the extent of the work your accountant completes, your requirements will also change.

The quality of the outputs also depends on the quality of the inputs. Because of your unique capacity to offer them the greatest information and resources from your eCommerce business, the consultation session, for instance, with a tax advisor or accountant, can be more in-depth and precisely suited to your unique business requirements. You can transition from receiving advice based on generalisations to receiving guidance based on your specific role within your company and your specific growth plans.

What to Ask Your Bookkeeper?

- Are they authorised and certified?

- What level of knowledge is required to complete the tasks?

- Do they have to have prior experience in your sector or specialised field?

- Which communication method do they use? Is that how you prefer to communicate?

- How quickly do they typically deliver and respond?

Here are some queries to ask when interviewing potential bookkeepers: whether you’re bringing someone in-house, outsourcing your bookkeeping to a service provider, or hiring a freelance bookkeeper.

How to Master Small Business Bookkeeping

A crucial component of small business finance is comprehending and monitoring your financial data. Because of this, if you own a business, you either need to take bookkeeping lessons or hire someone to do it for you.

Fortunately, learning how to handle your books is not only doable but also has several significant advantages. You may still retain the fundamentals and take things on your own if you’re new to keeping track of your finances and need help to engage a bookkeeping firm or independent bookkeeper.

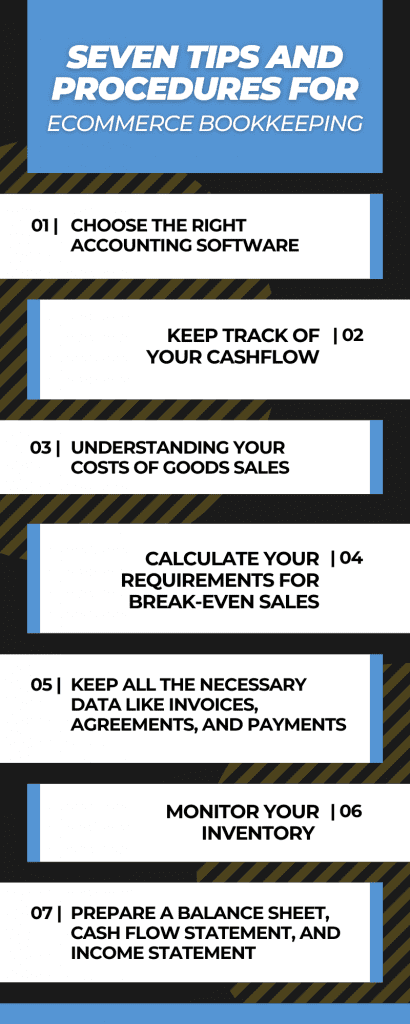

Seven Tips and Procedures for E-commerce Bookkeeping

Successful day-to-day operations of any firm depend on good bookkeeping. It deals with routine business operations, including inventory management, financial data recording, storage, and recovery, among others. Advanced bookkeeping programming software play a bigger role in the more important aspect, making it easier to manage and retrieve real-time data.

Choose the Right Accounting Software

To accurately record all pertinent information and data for your business reports, surveys, and evaluations, you should use accounting software. When dealing with bookkeeping alone, several of these applications include navigation support in their customer service as well. They enable you to streamline procedures for collecting receipts, managing stock, and receiving payments for e-invoices.

It may be beneficial to take into account bookkeeping software like XERO and QuickBooks because they permit multiple individuals to work simultaneously on the same data, which can more efficiently streamline processes.

Keep Track of Your Cashflow

You must first consider the inflows and outflows of cash for your company (such as sales) (e.g., overhead and operational expenses). You should be able to add up your credits and debits at the conclusion of each tracking period with ease. You should be as open and honest about your cash inflows and outflows as you can.

Additionally, you need to consider where your debts are going if you want to keep a positive cash flow. A good bookkeeping system can allow you to identify one-time costs that appear to be recurring too regularly, such as excessive fees from a merchant partner, as well as obligatory recurring charges (such as website upkeep, platform fees, and digital marketing costs).

This brings us to the second thing you should keep an eye on: the trajectory of your earnings and expenses. Any sudden increases in revenue need also be taken into account, as do any sudden increases in costs. This relates to what we said earlier about making wiser financial decisions.

Explore effective financial strategies to optimize your startup’s cash flow and support sustainable growth.

Understanding your Costs of Goods Sales

A multitude of indicators important to e-commerce enterprises depend on knowing your COGS and getting it as accurate as you can. COGS is first and foremost a component of the formula for calculating gross profit margin: gross margin = sales – COGS. Having accurate COGS is essential because the gross margin is such a crucial KPI.

The direct expense that retail organisations, especially those that operate online, incur to sell goods is known as the COGS, or Cost of Goods Sold. Direct labour, manufacturing, raw materials, vendors, and suppliers are all included in this. Additionally, it covers the freight charges, customs tariffs, and other fees necessary to deliver the product to your warehouse.

COGS does not include the freight charges you incur to distribute goods to clients or the expenditures associated with R&D. Similar to how packaging used to ship things to clients is excluded, even when packaging for the product itself is included. Marketing expenses and other indirect costs of selling items are excluded.

You can develop a more thorough understanding of which products are profitable when you compute COGS on a product, SKU, or category level. Additionally, you can compare data from other time periods to understand how profitability is altering. You can alter your price methods from here, as well as your marketing and purchasing plans.

Calculate Your Requirements for Break-even Sales

When sales equal expenses, that is when a business reaches its break-even point. When you see that your company is at that stage, it’s important to carefully examine all of your expenses, including your rent, labour prices, and material expenditures, as well as your grading system.

Think about the following: Are your costs either too high or too low to reach your initial investment goal in a reasonable amount of time? Is your company runnable? You need the following information to comprehend how to calculate the starting investment point:

- Fixed fees

- Variable expenses

- The item’s price at retail

What separates fixed expenses from variable costs? Regardless of how many deals you close, fixed expenditures remain ongoing expenses. You must cover expenses like rent and insurance in order to keep your firm operating.

Variable expenses, however, fluctuate depending on a number of circumstances. Your variable costs rise as you generate more revenue. Direct materials and direct labour may be part of these expenses. The break-even point is determined by dividing your total fixed costs into unit cost and variable cost per unit. Keep in mind that business expenses and variable costs are simply per unit, whereas acceptable costs are the overall costs.

Keep All the Necessary Data like Invoices, Agreements, and Payments

A significant portion of bookkeeping involves maintaining and organising data. It’s easy in theory, but it can save owners a lot of trouble in the long run. For instance, the tax office asked for more details regarding particular transactions you made three years ago. You can present your materials right away because they are already well-organised.

The correct software streamlines everything more effectively. Consult your bookkeeping or accounting team for advice on which accounting software would work best for your company and, most importantly, on how to use it. Data entry, record keeping, data consolidation, and general record organisation are all made easier with the correct software.

Monitor your Inventory

For your e-commerce firm, having a trustworthy inventory management system is essential, both when looking at your COGS as a whole and when looking at it on a more detailed level. You require current and precise information on inventory levels in order to properly register your COGS. This is crucial for tax purposes as well as for better decision-making.

You can maintain precise inventory levels across several platforms by using an inventory management system like Unleashed Software or DEAR Systems. Although many procedures are automated by these tools, it can still be helpful to physically walk through your inventory and perform a stocktake periodically.

Prepare a Balance Sheet, Cash Flow Statement, and Income Statement

You can get help from a bookkeeper in keeping financial records for your company. Maintaining accurate and up-to-date financial records will allow you to maintain reliable information that will considerably aid you in anticipating any major issues before they arise.

To keep track of all money owed to you, keep receipts and issue reminders to your clients on time. This will significantly enhance your company’s cash flow, allow you to see any abnormalities, and assist you in avoiding any future cash shortages.

Conclusion

Bookkeeping for an eCommerce Business is as important as it is for a retail business. Though, to operate a profitable online store, you don’t need to be an accounting whiz. In light of this, it’s a good idea to familiarise yourself with the fundamentals of bookkeeping for online retail enterprises so that you will know what to anticipate and what to pay attention to while you’re busy starting your firm.

There are quite a few tools and methods mentioned above that can help you run your eCommerce business smoothly and efficiently. Clear House Accountants is a leading firm in the UK that ensures eCommerce businesses with accurate and timely bookkeeping services.

Additional Resources

FAQs about Bookkeeping for an eCommerce Business

Can I use QuickBooks for eCommerce?

Your e-commerce company’s bookkeeping is made easier using QuickBooks. You can download your payouts and add them to your accounts using QuickBooks. To access specific sales orders, use the Orders tab in QuickBooks.

How do you record Sales in eCommerce?

You must either create a ledger for the e-commerce operator beforehand or on the spot while recording the invoice in order to record a sales invoice for sales made through an e-commerce operator. You can make the necessary updates to the ledger if one has already been produced.

What is Bookkeeping in an eCommerce Business?

The act of daily documenting your company’s financial transactions into arranged accounts is known as bookkeeping. It may also refer to the many recording methods that companies may employ. For a number of reasons, bookkeeping is a crucial step in the accounting process.