This guide explains how the VAT Domestic Reverse Charge works in the construction sector, when it applies, and how it affects contractors, subcontractors, invoicing, VAT returns and compliance.

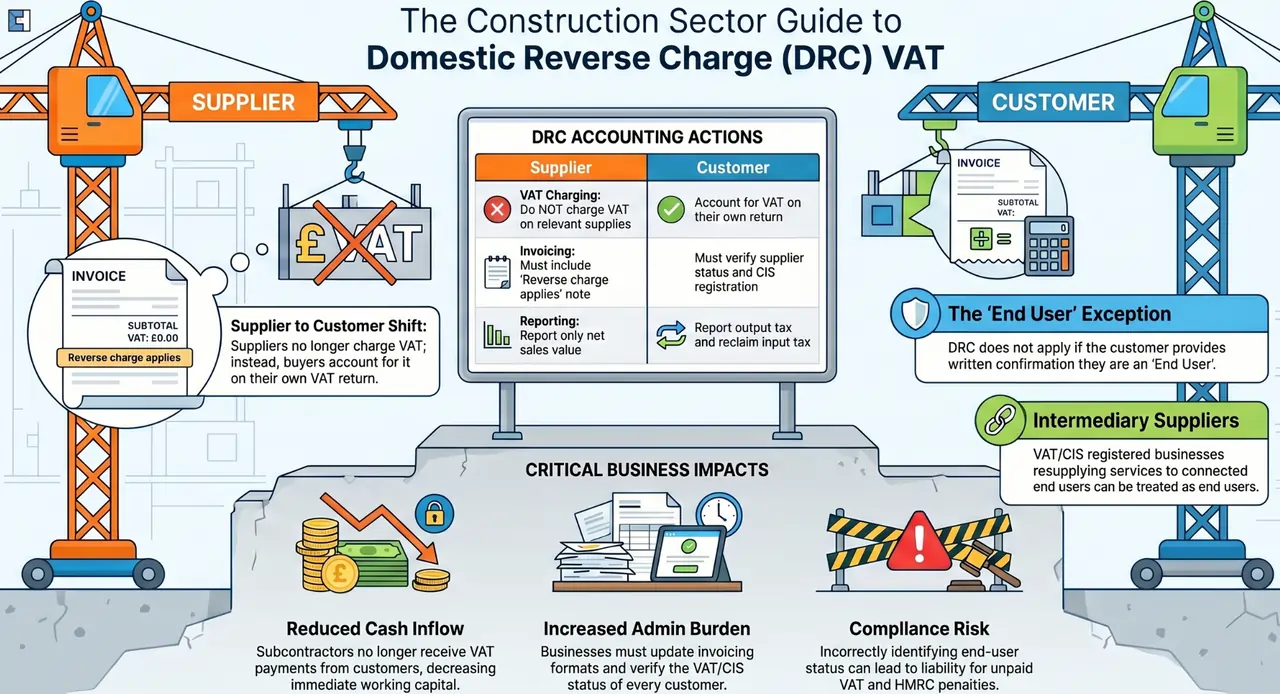

The Domestic Reverse Charge shifts the responsibility of accounting for VAT from the supplier to the customer in construction and building transactions under the Construction Industry Scheme (CIS). It is a VAT anti-fraud measure that changes how businesses manage VAT.

Before looking at the detailed rules, here are some key points construction businesses should know:

- Suppliers do not charge VAT on relevant supplies where the Domestic Reverse Charge applies.

- Buyers are responsible for accounting for VAT themselves on their VAT return.

Does the Reverse Charge Apply? A Quick Checklist

Before you issue or process an invoice, go through this checklist to determine whether the domestic reverse charge applies:

- Is the supplier VAT registered?

- Is the customer VAT registered?

- Is the supply within the scope of CIS?

- Is the supply standard-rated (20%) or reduced-rated (5%)?

- Is the customer not an end user or intermediary supplier?

- Has written confirmation of end user or intermediary status been requested and either not received or confirmed as not applicable?

If the answer to all six questions is yes, the domestic reverse charge applies. If any of the above answers is no, normal VAT rules apply.

When the Reverse Charge Applies

If a customer or business is registered for VAT and CIS and has no written confirmation of the end user, or is without an intermediary status, the domestic reverse charge for VAT is applicable to them.

As a supplier, if you believe your customer is an end user but they have not confirmed it in writing, you need to apply the reverse charge instead of charging VAT normally. There may be a risk of incorrect VAT treatment if the status is misidentified.

Read on to explore how it impacts your cash flow.

How the Reverse Charge Affects End Users

If your business is registered for VAT and Construction Industry Scheme (CIS) and you are not involved in resupplying construction services, your business or group of businesses is classified as an end user.

If you are a contractor or a subcontractor, learn how CIS is implemented to combat tax evasion in the building and construction industry.

In this case:

- Reverse charge won’t be applied to you.

- The supplier will account for VAT in a normal way.

- You must notify the supplier in writing that you are an end user.

If you fail to notify, the reverse charge will apply instead of the normal VAT rules.

Let’s find out how intermediary suppliers are affected by it.

Are you still not VAT-registered? Learn what happens if you don’t register for VAT.

Reverse Charge Rules for Intermediary Suppliers

To be considered an intermediary supplier, a business must be VAT and CIS-registered. Additionally, it is necessary to be involved in buying construction services and resupplying them to a connected end user. To be eligible as intermediary suppliers, businesses must:

- Have a relevant interest in the same land where construction work is going to happen (e.g., landlord or tenant)

- Be part of the same corporate group or undertaking as mentioned in section 1161 of the Companies Act 2006 on the government legislation website.

Intermediary suppliers can be treated as end users, and upon notifying suppliers (in writing), the reverse charge won’t apply to them.

Explore what MTD for ITSA is, how to sign up, quarterly reporting, its impacts, key requirements, exemptions, and what to do to stay compliant in this guide.

How the Reverse Charge Affects Cash Flow

Under this rule, sub-contractors do not receive VAT from customers. This will reduce the gross amount entering your business, thereby affecting your overall cash flow. Here are some of the major impacts:

- Reduced cash inflow

- Availability of less working capital

- Potential need for cash flow planning

- Applying to monthly VAT returns for quick VAT recovery

If you are struggling with cash flow as a result of the reverse charge, get expert VAT advice from our expert VAT accountant.

If you are suffering from cash flow problems, explore how an accountant can help overcome your worries and how cash flow forecasting impacts your business growth.

How the Reverse Charge Affects VAT Returns

Suppliers will not charge VAT and report only net sales value on their VAT returns. In contrast, customers must report the output tax and, if eligible, reclaim it as input tax. Since it shifts accounting responsibility from the supplier to the customer, it increases their administrative responsibilities.

Find out how the domestic reverse charge affects each VAT return box:

For Suppliers:

- Box 1 (Due VAT on sales): Do not include any VAT on reverse charge supplies in this box.

- Box 6 (Net sales value): Include the total net value of reverse charge supplies here..

For Customers:

- Box 1 (Due VAT on sales): Add the output VAT you calculated on the reverse charge supply.

- Box 4 (VAT reclaimed): Reclaim the VAT amount as input tax in this box.

- Box 6 (Net sales value): Do not add the reverse charge purchases here.

- Box 7 (Net value of purchases): Include the net value of reverse charge purchases.

Making mistakes in these boxes is one of the most frequent compliance errors HMRC notices in construction VAT returns. If you want to efficiently manage these requirements, get our VAT return services.

If your business is struggling with registering or submitting VAT returns due to complex procedures, give this guide a read.

Reverse Charge Invoicing Requirements

While invoicing, suppliers must show the net amount and VAT rate (not charge it). They need to write a note such as “Reverse charge applies” or “Customer to account for VAT” to indicate that the domestic reverse charge applies.

Practical Invoice Example:

For a clearer understanding, take a look at this example invoice.

| Description | Amount / Details |

| Construction services | £10,000.00 |

| VAT | Reverse charge applies (customer to account for VAT to HMRC) |

| Invoice Total | £10,000.00 |

As per the VAT Act 1994, Section 55A applies. The customer needs to account for the VAT of £2,000.00 (20%) directly to HMRC.

You need to update accounting systems and invoice formats to show reverse charge requirements. The risks of non-compliance will increase when an invoice is inaccurate.

Not sure whether the reverse charge applies to your invoices? Our VAT experts can review your supply chain, comply with the obligations and thoroughly check your invoices for accuracy. Speak to our VAT Construction Specialists today!

This comprehensive guide gives a complete overview of the invoice process.

How the Reverse Charge Applies to Different Workers

Labour-only sub-contractors offering supplies are treated as reverse charge if the supplies are within the scope of the CIS and all other conditions are met. In addition, they should not charge VAT on the invoices.

Reverse charge does not apply to employment businesses. They are treated as supplying staff, not as providing construction services. Therefore, businesses need to carefully classify whether they are supplying staff or supplying services. Incorrect classification can lead to errors that result in hefty fines and penalties from HMRC.

Reverse Charge Rules for Contracts and Mixed Supplies

Along with construction services, if goods are supplied, they’ll be treated as a single supply. In this scenario, the reverse charge will apply to the full invoice amount. If the reverse charge element is 5% or less of the total value of supply, it may be disregarded, and normal VAT rules applied.

It applies where the reverse charge element is only a minor part of the overall supply. Businesses can agree to treat future work on the same site under reverse charge. They need to carefully review the contract structure and refrain from artificially splitting invoices.

If you are new to contracting and want to explore how to become a contractor in the UK, explore our in-depth guide.

Reverse Charge and VAT Accounting Schemes

A business cannot use the VAT Cash Accounting Scheme for transactions that fall under domestic reverse charges, as confirmed by HMRC VAT Notice 731. On the other hand, under the VAT Flat Rate Scheme (FRS), sales subject to the Domestic Reverse Charge (DRC), like certain construction services, must not be included in your flat rate turnover calculation.

As a result, many construction businesses will change their accounting methods and review the suitability of VAT schemes for their businesses.

Common Reverse Charge Errors and Compliance Risks

Applying the reverse charge can be difficult for many businesses. There is a risk of misclassifying VAT, incorrect VAT treatment, and the possibility of incurring liability for unpaid VAT. HMRC may issue penalties for genuine errors and will investigate cases of suspected deliberate non-compliance, such as repeated wrong VAT treatment.

To avoid costly mistakes, you can talk to our specialist VAT advisors for accuracy and compliance.

Special Construction Reverse Charge Scenarios

These are some special construction reverse charge scenarios businesses should be aware of:

- Snagging work: the VAT treatment usually follows the reverse charge treatment of the underlying construction supply.

- Design & build companies: may qualify as intermediary suppliers.

- Scaffolding: depends on the contract structure

- Utilities & public bodies: often treated as end users if they are not resupplying construction services so status must be confirmed.

Please note that the VAT treatment may differ based on the context of the work and requires careful contract and supply chain analysis.

Key Business Implications

Businesses need to recognise that the domestic reverse charge creates:

- Operational responsibility: They need to verify customer status and documentation

- Financial impact: Businesses might suffer from reduced cash flow but increased VAT reclaims

- Administrative burden: It will add to their administrative burden with more complex systems, invoicing, and reporting.

If you want to make decisions to create meaningful results for your business, give our financial planning guide a read.

Bottom Line

The domestic reverse charge system shifts the responsibility of suppliers to customers. It removes the temporary cash flow benefits received by subcontractors and increases compliance and administrative burdens. In addition, it needs strong documentation and communication across the construction and building sector.