Self-Employed Individuals Should Be Wary of the Pension Gap

A major concern for most developed economies arises when too much emphasis is laid on the present and not much thought is given to the future. Sometimes, self-employed individuals are busy making a living, completely focused on the present, not paying much attention to the uncertainty that comes with age. The pressure of work, the desire to succeed and the limitless energy can make someone at their prime age forget that while working hard in the now is good, planning for retirement is also key.

It is understandable that our inward drive for success and prioritisation for generating profits can force us to overlook the monetary investment that is required for our long-term savings, but this simple act of ignorance can prove to be catastrophic in the long run.

Recent figures have revealed that more than 60% of self-employed individuals in the UK are not monetarily contributing to their long-term pension savings. According to research by an investment company, 3 in 10 self-employed individuals in the UK save nothing at all and are on the brink of poverty or social insecurity if their business collapses or terminates. This can be due to the fact that these self-employed individuals feel no compulsion to save and are under no obligation to register under any pension scheme ,unlike full-time employees working in a firm who have more options under the auto-enrolment regime. If you are a business that employs people and needs an auto-enrolment scheme set up, we recommend that you speak to a competent accountant or payroll accountant.

The more one tends to ignore the importance of savings now, the more it will be difficult for them to save and increase their long-term savings later. The solution lies in developing a habit of saving every month, no matter how little the amount is.

If you are thinking about increasing your savings by utilising tax-efficient strategies, it is advisable to hire a personal tax accountant who will be able to advise you on smart tax-saving solutions, enabling you to keep a larger chunk of your income aside for long-term savings.

According to the Office for National Statistics, the total number of self-employed Britons has risen from 3.3 million to almost 5 million from 2001 to 2018. This rise indicates people’s preference for flexibility and freedom in their work, whilst maintaining a balance between their social and business lives.

There is, however, a considerable number of people who are concerned about the resources they will be able to save for their retirement. The time constraint and the need to grow their business are what delay self-employed individuals from thinking about saving in a pension plan.

It’s not easy to save when there are a lot of financial obligations to be met, such as repaying loans, meeting the running costs of the business and costs incurred in paying for different training courses. There is just too much on their list that forces one to neglect the importance of savings.

If you are self-employed and saving in a pension scheme, or just saving you should take these precautionary steps:

Put aside a short-term cash reserve. The cash reserve will provide a cushion during times of crisis, this is highly recommended for those not having a fixed income and who are highly dependent on a variable income source.

Apply for income protection insurance. The reason we emphasise having income protection insurance is for the individual to have protection from unforeseen situations. The protection insurance guarantees safety for the self-employed worker and their family if something bad happens. If we compare a typical employee working in a firm in the UK, that employee will have insurance and cover for situations that may arise due to their inability to work, either because of sickness or termination from employment. These protections save them resources and give them time to recover or pursue new employment opportunities.

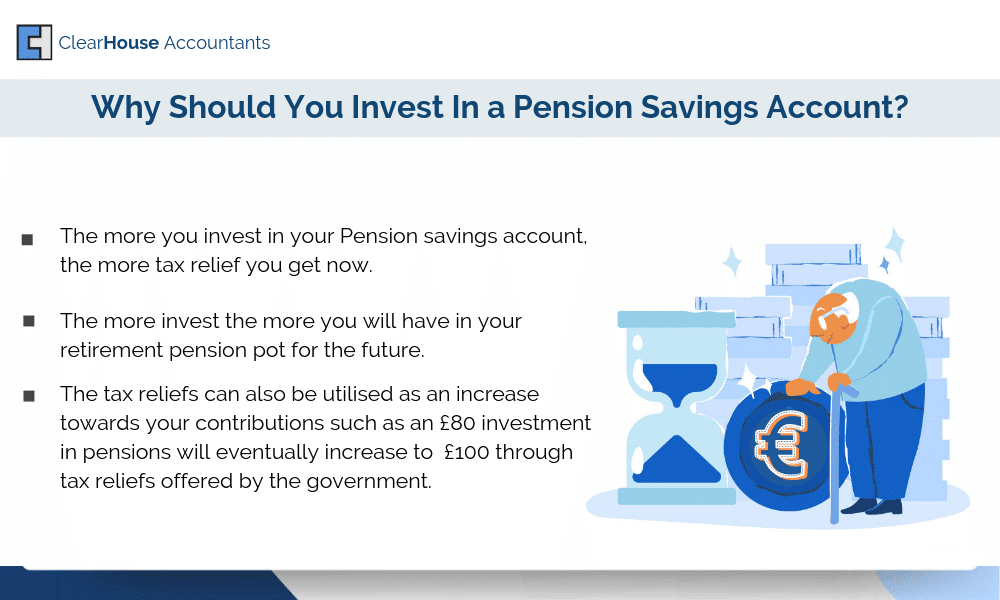

Last but not least, plan for retirement. It’s advisable to keep things simple; it’s fine if you save cash throughout the year in your savings account. It is advisable that you start saving for your pension effective immediately, as it’s going to benefit you in the long run. The more you invest in your pension savings account, the more tax relief you get now and the more you will have saved in your retirement plan for the future.

To get you a clear idea of the tax benefits, your £80 investment in pensions will eventually increase to £100 through tax reliefs offered by the government, but only if you are a compliant taxpayer. The higher your rate of tax, the more you are able to get in tax reliefs whilst submitting annual tax returns. A similar type of bonus may be enjoyed if you invest in the newly introduced ‘lifetime individual savings account’, but that requires you to be under the age of 40 for eligibility.

It becomes very frustrating when you have a lot of options on the table to consider and you just have to choose one, in this case, you may want to seek advice from a tax accountant or an CHACC accountant about the optimal steps you can take.

It is not the best plan to have a retirement plan that depends entirely on the money generated by selling a business after retirement. Each business is unique and can take ages to sell or can be overpriced; therefore, it is considered a risky retirement option. It is advisable for you to create and pursue a proper pension plan or register under a state-run protection programme if you have not yet planned anything.

You may seek the expertise of a tax accountant to get a full review of your personal pension plan and your drawdown plan once the pension is due to be extracted. Your accountants may also help you to discover potential benefits and reliefs that come along when you register under a particular pension scheme.

Clear House Accountants are professional accountants who have been working for a considerable number of years with self-employed individuals. Our team of in-house tax accountants guide our clients on how they can adopt pension schemes while utilising tax reliefs. Speak to us to learn more

Additional Resources