ISAs, or Individual Savings Accounts, have become a go-to choice for many people in the UK looking to save or invest their money smartly. The tax advantages that come with these accounts make them quite popular.

ISAs come in various forms, including Junior ISAs, Innovative Finance ISAs, Cash ISAs, Stocks and Shares ISAs, and Lifetime ISAs. These Individual Savings Accounts (ISAs) cater to long-term or short-term savings, portfolio building, retirement planning, and providing cash for your child’s future.

This comprehensive guide will examine the specifics of each ISA, including its characteristics, eligibility conditions, and special benefits.

What Are ISAs?

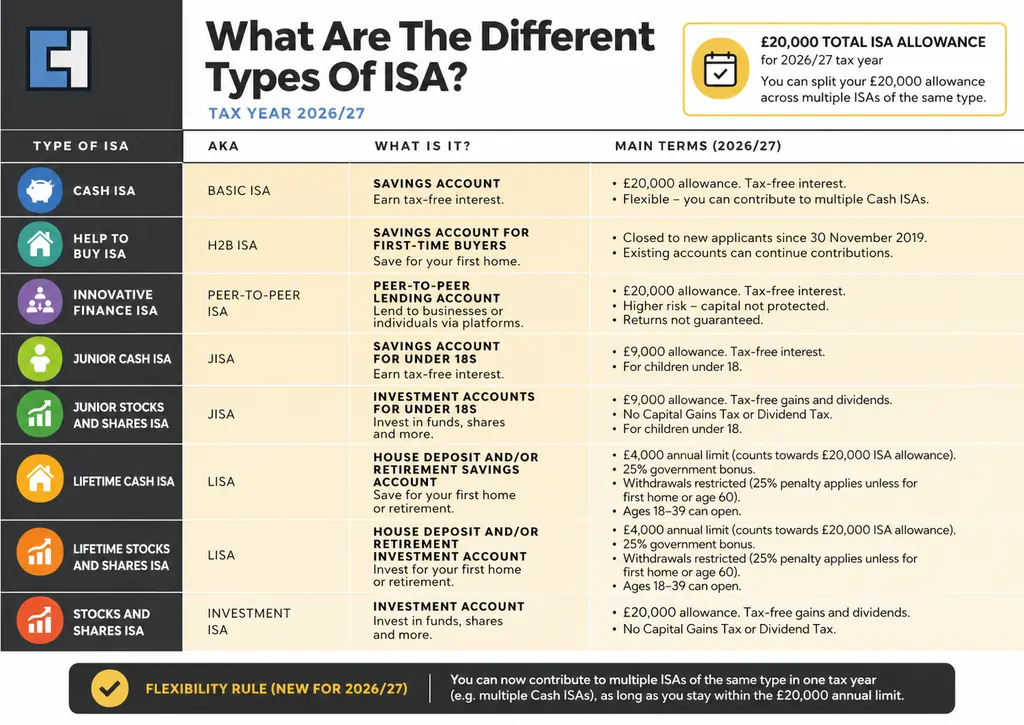

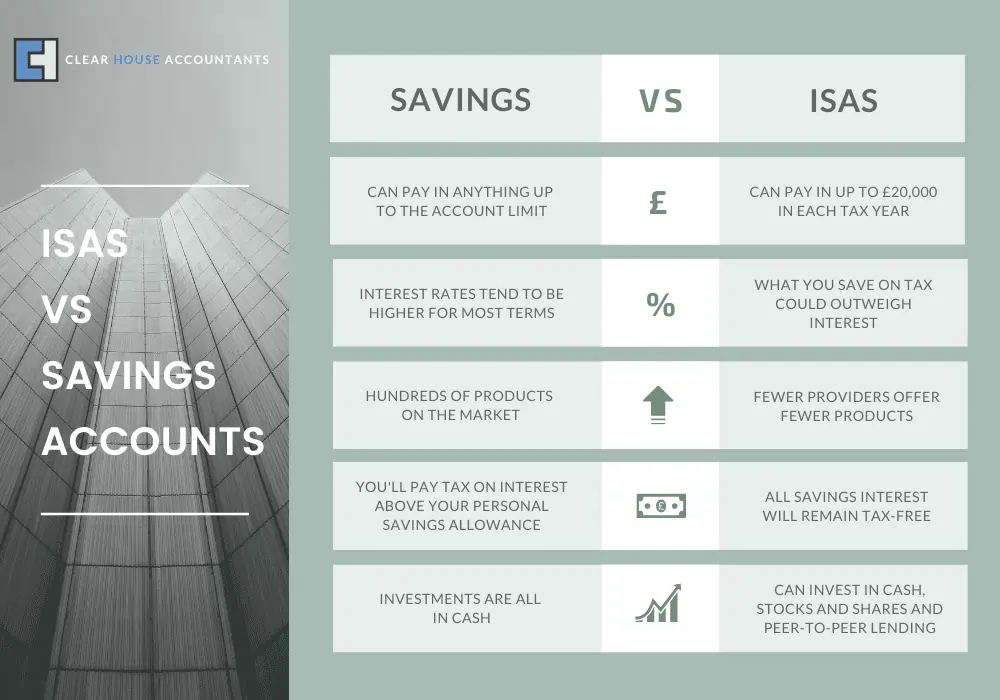

An Individual Savings Account, or ISA, is a tax-free savings account, though there’s a limit to your annual Tax-free ISA allowance. You can choose from a range of ISAs, and there’s no limit to how many you can have. You can contribute to multiple ISAs of the same type within a tax year, provided the overall £20,000 limit is not exceeded, and providers allow it.

- The maximum amount one can contribute in the current tax year, 2026/27, is £20,000.

- Your yearly allowance is reset each time a new tax year begins.

- You can transfer your existing Individual Savings Accounts (ISAs) to your new ISA.

- Children in the age range of 16 to 18 have the opportunity to possess both a Junior ISA and a regular Cash ISA. For Stock ISA an individual must be 18 or over 18.

- Customised options are available to help individuals save for their first home purchase or retirement.

- For flexible ISAs, you can replace withdrawals without affecting your allowance within the same tax year.

The Different Types of ISA Accounts

The main 5 individual Savings Account (ISA) options are available to adults and kids.

- Cash ISAs

- Stocks and shares ISAs

- Lifetime ISA

- Innovative Finance ISA

- Junior ISAs are for children and can be established by their parents.

Cash ISAs

Cash ISAs are very similar to regular savings accounts, and your savings interest isn’t taxed when it comes to Cash ISAs. You’ve got quite a few cash ISAs to pick from, too. They might seem like they all function the same way, but actually vary in terms of profit, access terms and conditions.

Easy Access ISAs

Easy access ISAs represent the most straightforward kind of cash ISA. They are specially designed to give you free access to your money whenever you desire. Typically, these ISAs permit an unlimited number of deposits and withdrawals with no penalties, although it’s essential to remember that some may have certain restrictions.

In most cases, easy access ISAs come with fluctuating interest rates. It means your initial rate can increase or decrease over time.

Fixed-rate ISA

This type of cash ISA is where your initial deposit is stashed away for a set period and earns a fixed rate of interest during that time. This period could be anything from one to five years, with longer terms usually offering higher interest rates.

Note: If you try to withdraw from your fixed rate ISA before the period ends, you could pay an interest penalty, and your ISA might even be closed after a warning.

Notice ISA

This option can provide you with higher interest rates than a standard, easy-access ISA, and it offers you more flexibility to withdraw money than a fixed rate ISA might allow. However, to withdraw money, you’ll need to notify the bank in advance, with notice periods generally ranging from 30 to 180 days. If you withdraw without adequate notice, you’ll face a penalty, the scale of which often matches the notice period.

Regular Savings ISA

A regular savings ISA might be your best bet if you want to save smaller amounts regularly. This type of ISA offers a better interest rate, provided you commit to making traditional, minimum deposits. However, if you withdraw prematurely, you might face a penalty.

Stocks and Shares ISAs

A stocks and shares ISA, also known as an investment ISA, invests your deposited money into funds, bonds, and shares. Even though stocks and share ISA can potentially boost your savings as the stock market grows, it’s crucial to remember that risk is involved. Your investment might lose value.

Like cash ISAs, the Financial Services Compensation Scheme (FSCS) typically offers protection up to £85,000 if your stocks and shares ISA provider collapses. However, this protection doesn’t cover any losses incurred from your investment or market performance. It is better suited to individuals who can afford to take risks with their money and have a long-term investment perspective.

Lifetime ISA

The Lifetime ISA (LISA) operates on the principle that the Government provides a 25% bonus on LISA deposits, capped at £1,000 per year for contributions up to to £4,000/year. The savings and the Government bonus accrue tax-free interest, which can be compounded monthly, annually, or on the anniversary date.

However, there are specific criteria and limitations associated with opening a LISA. Eligibility requires:

- You should be between 18 and 40, with the first deposit made before reaching 40.

- You can make contributions up to £4,000 per year until age 50.

- After turning 50, the Government bonus ceases, but the savings continue to earn interest.

- Withdrawals from the LISA are permitted only for purchasing a first home, reaching the age of 60 or above, or being terminally ill with less than a year to live. Any other early withdrawal may result in 25% withdrawal charge as a penalty.

- When using your LISA to buy your first home, the property value mustn’t exceed £450,000.

If you opt for a Lifetime ISA (LISA) as a retirement savings vehicle, you can withdraw funds from your account at age 60. Utilising the savings for your needs is permissible, although the LISA is primarily intended to provide financial support in retirement.

Innovative Finance ISA

In the realm of peer-to-peer lending (P2P), an Innovative Finance ISA (IFISA) allows individuals to lend their deposited funds to individuals or small businesses, or to invest in crowdfunding projects, for a predetermined period.

The aim is to generate tax-free returns on the initial investment after the specified timeframe. It’s important to note, however, that returns are not guaranteed, and there is a level of risk involved with the invested capital. Unlike a stocks and shares ISA, an IFISA does not protect the FSCS in the event of the provider’s collapse.

How Do You Transfer an ISA?

You can move your ISA savings to a different provider, including another type of ISA, whenever you wish, depending on the provider’s terms.

If you have money saved from previous tax years, it will not affect your allowance. Any money, no matter how big or small, can be transferred at your discretion. For instance, you can transfer £15,000 from your old cash ISA to a new stocks and shares ISA, and you can still make a further £20,000 contribution in the same tax year.

All contributions made in the current year, including any growth associated with them, must be transferred in full. After the transfer is finished, you will still have some permissions. There are a few important things to remember when moving your ISA. First off, taking physical withdrawals of the funds is not recommended, as it may result in losing tax-free status; instead, use the official ISA transfer process.

When you switch to a new provider, you may be required to pay an additional fee for the initial set-up or advice. If you possess a Lifetime ISA, it is essential to be aware that transferring to another type of ISA (before your 60th birthday) is considered a withdrawal, resulting in a fee application and 25% withdrawal charge.

How Do You Open an ISA? | Setting up an ISA

Different banks give you several ways to operate an Individual Savings Account (ISA). You can easily open an ISA in the UK if you’re a UK resident or Crown servant abroad. You can go to a local branch, send an application by mail, use their online platform or a mobile app, or even call them.

Usually, you’ll need to deposit an initial amount to open an ISA, which can vary from as little as £1 to thousands of pounds. However, some ISAs might require you to commit to a minimum regular deposit each month.

The provider of the ISA will also require certain personal information from you, such as your complete name, address, national insurance number, and signature. You must thoroughly read the ISA provider’s declaration and carefully comprehend any limitations or fees associated with withdrawing funds from your ISA.

How many ISAs can you have?

Since April 2024, new reforms have allowed an individual to open multiple ISAs of the same type in one tax year, depending on the provider’s terms and conditions. Once the new tax year begins in April, you can open one of each category again. Consequently, over several years, you may accumulate many ISAs.

No matter how many ISAs you open, your tax-free ISA allowance is limited to £20,000 per tax year. It’s also important to note that even if you have multiple ISAs of the same type, you can only pay into one each tax year. If you have multiple ISAs, you might choose to pay into the one with the highest interest rate.

Can you withdraw from an ISA and deposit the funds later?

With a ‘flexible’ ISA, you can withdraw and replace funds within the same tax year without using up your allowance. This includes deposits from previous years; repaying them before the tax year ends doesn’t affect your current annual limit.

However, reinvesting money taken from a non-flexible ISA counts as a new contribution toward your allotment. Transferring funds to a standard account ends their tax-exempt status, making them subject to HMRC tax rules and your personal savings allowance.

Conclusion

In summary, without paying income tax on interest or investment returns, Individual Savings Accounts (ISAs) offer incredibly flexible and tax-advantageous methods for people to increase their wealth. They provide several solutions to suit different risks and savings goals.

When deciding what to buy, it’s critical to understand the subtle differences between the types of ISAs. Your goals and financial status should guide the decisions you make. When selecting the best individual savings account (ISA) for you, don’t forget to consider your risk tolerance, investment horizon, and specific savings objectives.