It might seem as if loaning money to your corporation firm is the simplest approach, but it has legal and tax implications.

According to a recent study, one home-based business is established every twelve seconds. There are 38 million home-based companies in the UK. Capital is one of the most essential elements in starting a company. People choose to lend money to their own firms, and this should be assured during the early stages of your company’s development.

Many individuals mix up lending and investment. Continue reading to learn more about loaning money to your own firm.

How to Lend Money to Your Own Company:

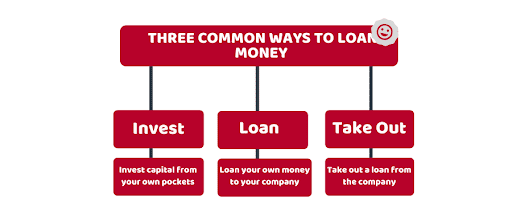

Most business owners use the following three methods to lend money to their own firms:

- You can raise money from your own resources.

- You may lend your company money if you have it available.

- Take out a loan from the firm.

You can’t avoid tax consequences even if you loan your firm from your own funds.

Requirements for Loaning Money to Your Own Corporation

There are four conditions that you must fulfill in order to qualify your debt for a loan rather than equity if you want to lend money to your business:

- Debt should be recorded as a written obligation that must be repaid by a certain date or amount on demand.

- The debt cannot be converted into stock for the company or any other equity interest.

- The organisation must establish interest rates and payment deadlines according to corporate earnings, decision-making processes, and other criteria.

- The lender must be a corporation, individual, estate, trust, or tax-exempt entity that is an eligible shareholder.

A “back-to-back” loan is when a bank or individual refuses to lend money directly to your business but will accept personal guarantees. If the lender requires personal guarantees in order to loan money, back-to-back loans are an option. In a back-to-back loan, the lender provides money to the shareholders, who then lend it to the company. When a back-to-back loan is utilised, tax consequences are considerably better than if a corporate loan is taken out.

Lending Money to Establish Your Own Company:

In the event that someone wants to start their own business and is looking for a loan. At the start, one must gather lots of information on the hazards and benefits of loaning your firm. You may either seek advice from friends and relatives or borrow money from a bank.

Consider the worst-case scenarios before commencing a loan application in case the firm closes. Let’s look at some of the ins and outs of borrowing money from the following lenders:

- Friends and Family.

- Commercial Loan from the Banks.

- Loaning Money to Your Own Company

Friends and Family:

Before asking friends and family for money, consider the consequences because the risk alert is extremely high. You will not have to worry about money if you are unable to pay back the amount, but your relationships may be jeopardised as well.

Another important factor to consider is the issue of borrowing from a bank. The paperwork should include all necessary information about terms and conditions, interest, payments, and any other concerns you may have regarding your payment ability. On average, 66% of firms fail every ten years, 50% every five years, and 30% every five years.

To avoid difficulties over interest in the same way as any other sort of loan procedure, the objective is to keep interactions at a distance and to comply with all rules. You

Commercial Loan From the Bank:

Most businesses prefer Loaning money to their own corporation from a bank since this minimises risk and eliminates tax and legal risks. The bank will begin by asking the applicant to investigate business plans, marketing methods, and finances. Your personal assets might also be inspected.

Lending money through the Small Business Administration (SBA) is another alternative. They give loans to startup firms.

Finally, Loaning from your Own Pocket:

If you’re looking for the simplest and cleanest approach to lending money to your business, you’ll still be weighed down by debt whether you do it yourself or with a lender. The consequences and ramifications will not change. Since the firm is required to pay each month’s installments of repaying and interest.

To avoid the disorder of a law violation, this has to be taken more seriously and documentation with regular inspections must be done in the same manner as it is with any other lender. In this situation, the greatest business idea is to hire a third party who keeps track of paperwork.

We comprehend that creditors are paid back first if a firm fails, leaving you without any assurance of receiving your money on time.

Furthermore, the element of interest is beneficial to the company since it lowers taxes. The interest is viewed as an increase in revenue, which may alter your tax status and result in you paying greater taxes.

Making an Investment in Your Small Business

Investing the money rather than taking a loan is another alternative. The cash goes into your owner’s equity account (for a sole proprietorship or partnership) or shareholders’ equity (for a corporation).

If you withdraw your funds, you’ll be taxed on any profits gained in the stock’s price rise. You will be taxed on any further payments received in the form of bonuses, dividends, or draws. There is no tax consequence for the firm on this investment.

If you withdraw your money, you’ll have to pay capital gains taxes if the stock’s value has risen. You will be taxed on any additional funds in the form of bonus payments, dividends, or draws if you receive them. This investment does not incur any tax liability for the company.

In bankruptcy or in other cases, both lenders and shareholders have a claim on a company’s assets. Shareholders’ claims are satisfied after creditors are paid.

Factors that you should think about before making a business contribution.

There are several things to consider when determining whether the owner’s contribution was a debt or equity. These factors include:

- Is the document’s title set to “loan” or “investment”?

- A maturity date: A loan’s presence usually implies the presence of a maturity date.

- The payment source. Is the payment a dividend or a loan?

- The lender’s right to force payment: What will happen if the loan isn’t repaid? Will there be fines? Is it possible to foreclose on a mortgage? This should be stated in the loan documents. This phraseology would not be found in a share of stock.

- In both cases, the lender’s right to take part in management applies. A lender shouldn’t be on a company’s board of directors (conflict of interest). As a rule, stockholders do not play a role in management as part of their purchase agreement.

- The lender shouldn’t have more rights to get paid than other creditors. This language may be found in the paperwork and refers to company bankruptcies as well as collection tactics.

- The aim of the document: A paper is beneficial in this area.

- The capitalisation of the (supposed) borrower’s/business’s) assets: In other words, does this seem reasonable? For example, in a partnership, partners should make similar contributions; allowing someone into a partnership without adequate investment may be problematic.

- The ability of the borrower (the business) to borrow funds from other lenders.

Whatever you choose – loan or investment – it’s critical that you make your contribution clear as a loan with a contract or a capital investment with appropriate paperwork so the tax consequences of the deal are obvious and you don’t run into any issues with HMRC.

Loan vs. Investment: Risks and Benefits to You

Every choice has its consequences, especially if the firm can’t pay you back or offer dividends. The biggest danger is that you will not receive your funds.

Investing is always a riskier proposition. There’s no assurance that an investment will continue to be profitable for the investor or even that he’ll break even on it. Borrowing is frequently less dangerous, particularly if the loan is secured by a valuable asset.

What if the company’s finances are unable to be paid (for example, in a bankruptcy)?

- You are a creditor if you lend money to a company. You may or may not be able to get your funds back in the case of an unsecured (no collateral from the firm) loan, depending on whether it was secured or not.

- If your firm goes bankrupt, you are 100 per cent exposed to the loss of your cash and there is little or no chance of getting it back.

It’s also important to figure out whether the organisation is new or has been around for a while.

- If you’re a small business owner, your investment allows the company to utilise your money without having to repay it right away.

If your company is up and running with a solid cash flow and positive credit standing, borrowing may be preferable.

Is it Permissible for a Director to Loan Money to the Company?

Yes, you may. In fact, this might be a preferable alternative to obtaining a business loan from your bank.

Loans are recorded in company directors’ loan accounts. If the firm provides credit to the directors, this is recorded in the same location for accounting purposes.

In all cases, we advise that you set up a loan agreement between the director(s) and the targeted, limited company – which are separate legal entities. There is no need to do this, but it creates a paper trail that may be beneficial in the future.

Even if you don’t use model formation documents, check to see whether your Articles of Association prohibit the company’s directors from giving loans.

Conclusion

In conclusion, the act of loaning money to your firm comes with advantages and risks. Your business becomes the lender, but you create debt for it, which it will pay in monthly instalments if your company fails and you go bankrupt; there’s no assurance that you’ll be repaid before the creditors. So, this must be considered carefully before taking out a loan. Always seek expert advice from an Accountant who specialises in Limited Companies to get advice specific to your situation.

Additional Resources