If you are considering the most suitable structure for your business, or planning a global structure that includes a UK limited company, this guide will give you a clear and comprehensive overview. It explains what a limited company is, the different types available in the UK, the advantages and disadvantages, the tax implications, and the key considerations involved. Where more detailed guidance is required, you will find links to step-by-step resources on forming, running, and closing a limited company. By the end, you will be able to assess whether a limited company is the right structure for your financial position, business model, and long-term objectives.

What is a Limited Company?

A limited company is called a limited company because it offers its owners limited liability. This means it is a separate legal entity, a business that is its own legal person apart from its owners. As a result, the company, not its owners, is responsible for its own debts and legal obligations.

Before moving on, let us take a moment to understand what limited liability signifies.

What is ‘Limited Liability’ in a Limited Company?

Limited liability means that the company’s owners are liable only to the extent of their invested capital. The company will be responsible for paying back any debts incurred by the limited company. In the event of the company’s bankruptcy, the owners would not have to lose any personal assets, making it one of the most recommended and safe business structures.

Types of Limited Companies in the UK

Once you decide to set up a limited company, your next step is to choose the most suitable structure. There are several options available that can be tailored to your personal and business circumstances.

To make this choice clearer, let’s examine each model in detail, which will help you select the right structure for your business with greater confidence.

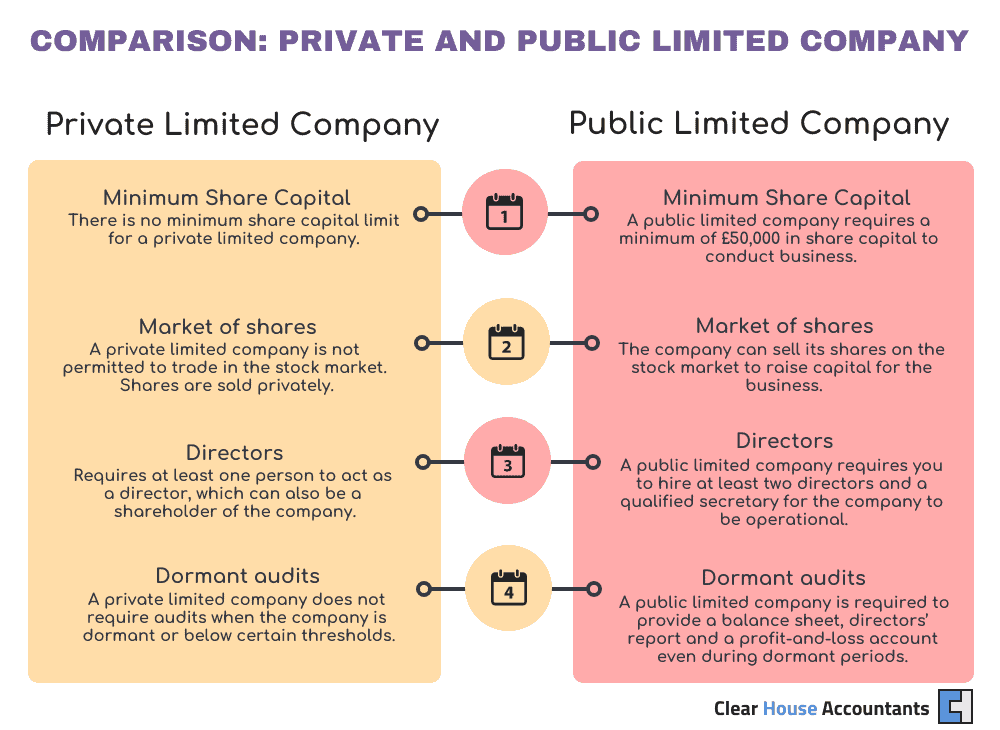

Company Limited by Shares (LTD)

A company limited by shares is the most common type of limited company in the UK. In this company type, the share capital is divided into shares held by one or more shareholders.

Features of a Private Company Limited by Shares

These are some of the key features of LTD:

- Separate legal entity

- Limited liability

- No minimum share capital requirement

- Shares not offered to the public.

- Ownership via shares

- Name must include “Limited” or “Ltd”

- At least one shareholder and one director

Why Form a Company Limited by Shares?

- If you want to start a business and generate profit for personal use, form an Ltd.

- You can sell a percentage of a business to others.

- As a shareholder, you are not liable to pay the company’s debts.

- An Ltd structure offers a professional impression and boosts credibility, attracting investors.

Company Limited by Guarantee (CLG)

A company limited by guarantee, unlike a company limited by shares, is typically chosen by non-profit organisations or charities. In this structure, surplus income is reinvested in the business rather than distributed to owners.

Features of a Company Limited by Guarantee

- Separate legal entity

- Limited liability

- No shareholders or share capital

- Members are the guarantors.

- Typically used for non-profits.

- Minimum one director required

- Governed by the Companies Act 2006

Why Form a Company Limited by Guarantee?

- You need to set up a non-profit organisation or a charity, such as a club or association.

- CLG retains surplus income for reinvestment or to perform non-profit objectives.

- The personal assets of guarantors are protected by limited liability. Guarantors only owe the business’s debts up to the amount they guarantee.

- The status and credibility of a business are recognised and improved when incorporated. Investors prefer to work with non-profit structures.

Public Limited Company (PLC)

This company structure is typically favourable for large businesses. They can offer shares to the public to raise large amounts of capital. Ownership of a public limited company is divided into shares. Shareholders are just liable to pay up to the value of their shares.

Features of a Public Limited Company

- Shares can be offered and sold to the public.

- Minimum allotted share capital of £50,000

- Trading certificate required

- Must include PLC or Public Limited Company

- Requires at least two directors.

- Company secretary required

- Unlimited shareholders

- Strict governance & disclosure

Why Form a Public Limited Company?

- A public limited company can raise large share capital. Anyone can buy the shares of a public limited company.

- The risk of company ownership is borne by public shareholders.

- Banks and financial institutions are willing to extend finance to a public limited company.

- There are more growth and expansion opportunities with public limited companies.

- Shares of PLC are easily transferable.

- Smooth exit strategy for the founders.

Advantages of a Limited Company

Here are some of the advantages of a limited company:

- Better tax planning: if you are a shareholder and a director of your company, you can take advantage of better tax planning opportunities.

- Separate Legal Entity: A business has its own legal entity, meaning you will not be held liable for the business’s actions and decisions, but your liabilities as a director will remain.

- Limited Liability: One of the most significant advantages is the limited liability it offers. Not having to pay off a business’s debts with your personal assets is always a huge advantage. A limited company promises you that you will only be liable for the money you have invested and nothing more.

- Securing Investments: If you are a public limited company, you can always issue new shares to secure additional investment for the business after the original investment is exhausted. People tend to trust investing in a registered company more than investing in a sole trader.

- Transfer of Ownership: The process of transferring ownership in a limited company is relatively straightforward. All you need to do is sell or gift your shares to the person you want to make an owner.

- Company Name Protection: The name of your limited company is legally protected by the compliance of Companies House.

- Hassle-Free Loans: Doing business with a limited company instils confidence and lends the company credibility, which might make it easier for an established company to secure loans for the business.

Disadvantages of a Limited Company

Let’s have a look at the disadvantages of a limited company:

- Mandatory Incorporation: Setting up a limited company requires incorporation with Companies House, which may incur extra expenses and take up much of your time.

- Naming Restrictions: Companies House has strict rules and regulations regarding your business name, which can be quite annoying at times.

- Public Disclosure: Public limited companies are required to submit their annual reports and statements to Companies House and HMRC, which are then posted on their websites for the general public and competitors to see.

- Records: Limited companies are required by law to keep strict records, including, but not limited to, maintaining records of board meetings and documenting every decision made.

- Notifying Companies House for Everything: The limited company is required by law to inform Companies House of every change to its management, capital, or the flotation of new shares on the market.

- Withdrawals: As limited companies are separate legal entities, their liabilities are theirs to bear, and their profits are theirs to retain. Meaning an owner cannot willfully withdraw finances from the company for personal requirements. The owners can only withdraw as dividends, issued in amounts proportional to the number of shares they hold.

How to Form a Limited Company

To set up a limited company, choose a company type and name, assign directors, shareholders/guarantors, and a business address. You need to complete the paperwork, such as the MOA and AOA.

Then you need to register your limited company with Companies House and identify the persons with significant control (PSCs). Once incorporated, you need to establish a statutory register and issue share certificates to shareholders (or membership certificates to members).

Then register the limited company with HMRC within 3 months for Corporation Tax and, when necessary, Payroll/VAT.

Taxation of a Limited Company in the UK

As a limited company, you are subject to paying Corporation Tax at 19% on taxable profits under £50,000. When your gains or profits are over £250,000, you’ll need to pay the main rate of 25% as per 2025/26. A limited company can claim Marginal Relief against these two thresholds.

Limited companies also pay other taxes:

VAT: if your 12-month taxable turnover exceeds £90,000 or you expect to reach it within the next 30 days, you’ll need to charge VAT and pay HMRC.

NICs and PAYE: a limited company with employees needs to pay PAYE via a payroll scheme and NICs.

Capital Gains Tax: if you make a profit while disposing of any business asset.

Limited companies need to pay taxes based on their business nature and the trade they perform, such as Company Car Tax, Income Tax, Dividend Tax and other taxes. A limited company needs to register for tax with HMRC and file quarterly or annual returns.

Unlike sole tradership or partnership, a limited company is a tax-efficient business structure. Owners can minimise their personal tax and NICs by receiving a salary and dividends from their company, keeping surplus income in the limited company’s accounts, and withdrawing it later.

Who Owns a Limited Company?

A limited company is owned by shareholders (also called members) in a company limited by shares. Guarantors are the owners of a company limited by guarantee. Owners of a limited company can be individuals, multiple members or corporate entities. Directors (commonly referred to as owners) are responsible for operations and business decisions.

The financial liability of limited company owners is limited to the fixed value of their shares or guarantees.

How to Close a Limited Company in the UK

There are several ways to close a limited company. A solvent limited company can be dissolved by voluntary striking-off (dissolution) or Members’ Voluntary Liquidation (MVL). For insolvent companies, Creditors’ Voluntary Liquidation is the most common option. Compulsory Liquidation and Administration are other ways of closing an insolvent limited company.

Conclusion

Setting up a business is not as complicated as people sometimes make it sound, but it does require scrutiny, dedication, and patience. Now that you know the basics of a limited company, you can start, but it is advisable to take it slow and make the right decisions with the right help. If set up correctly, a limited company might be what you need to achieve financial success.

Additional Resources

FAQs

Should a company register for VAT even if it is not required?

VAT registration is not always mandatory, but voluntary registration can provide financial and business advantages.

A company must register for VAT if its taxable turnover exceeds the HMRC threshold (£90,000 for 2024/25). However, even if turnover is below this threshold, voluntary registration can be beneficial. It allows the business to reclaim VAT on expenses, improves credibility with clients, and prepares the business for future growth. This is especially useful when working with VAT-registered clients.

When should a company register for PAYE?

PAYE registration is required when a company pays salaries, including director salaries.

A company must register for PAYE as soon as it starts paying employees, including directors. This allows the company to deduct and report Income Tax and National Insurance Contributions to HMRC. Even if the director is the only person being paid, PAYE registration is necessary to remain compliant and avoid penalties.

When should a company file a company tax return?

A company must file a Corporation Tax Return every year after registering for corporation tax.

Once registered for Corporation Tax, the company must submit a CT600 tax return annually, even if there is no profit. The return is due within 12 months of the accounting period end, and any tax owed must usually be paid within 9 months and 1 day. Filing on time ensures compliance and avoids HMRC penalties.