Benefits in Kind (BIK) are non-cash benefits provided by employers to employees or directors. Unlike cash payments such as bonuses or commissions, Benefits in Kind take the form of goods, services or privileges, and many are subject to Income Tax and National Insurance Contributions (NICs).

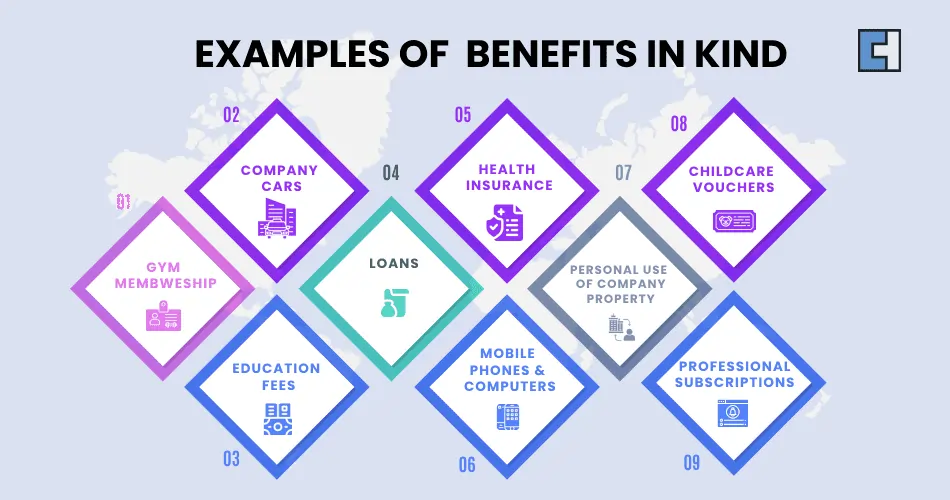

Common examples include company cars, private medical insurance, interest-free loans, gym memberships and living accommodation. While some BIKs are fully taxable, others are exempt or qualify for reduced treatment depending on HMRC rules.

This guide covers how BIK tax works, how to calculate taxable values, who pays the tax, how to report Benefits in Kind to HMRC, and what payrolling BIK means for employers and employees.

Key Takeaways

Taxable vs Exempt Benefits: Most Benefits in Kind are taxable, but mobile phone, cycle-to-work schemes and employer pension contributions are exempt. Others qualify for threshold-based exemptions, such as trivial benefits (under £50) and interest-free loans under £10,000.

Employee Tax Implications: Employees pay Income Tax on the taxable value of their benefits. The tax is collected either through PAYE tax code adjustments or, increasingly, through payroll.

Employer Reporting Responsibilities: Employers must report most BIKs to HMRC via P11D forms by 6 July each year and pay Class 1A National Insurance Contributions (NICs) at 15% by 19 July (22 July if paying electronically).

Payrolling Benefits: Payrolling BIK allows employers to tax benefits through the monthly payroll rather than the end-of-year P11D process. This is expected to become mandatory for most employers from April 2026, subject to HMRC confirmation.

How BIK Tax Works

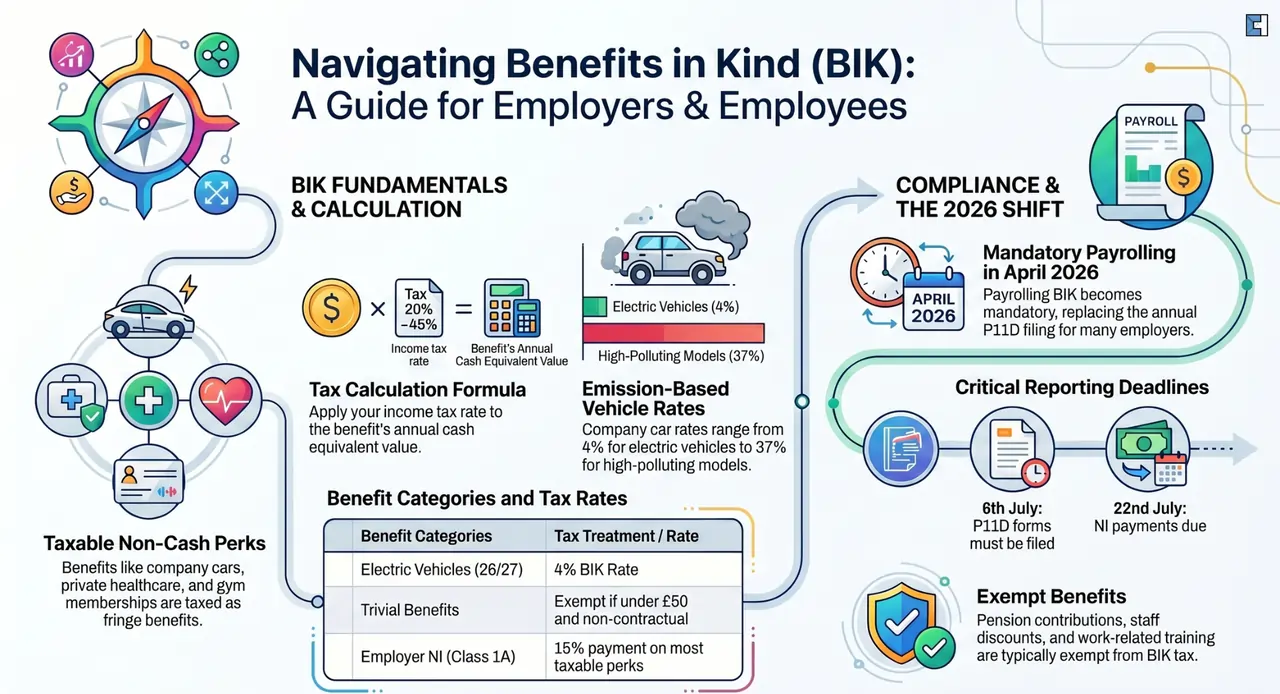

If you receive a benefit in kind, you are liable to pay income tax on the taxable value of the benefit. You can apply your income tax rate (20%, 40%, or 45%) to the cash equivalent of the benefit to calculate BIK. If an employer fails to report the correct BIK or to report it on time, they may face penalties, including fines and interest on unpaid taxes.

Who Pays Benefits in Kind Tax?

BIK tax is split between employees and employers:

Employees

- Employees pay Income Tax on the cash equivalent value of their benefit.

- The rate depends on their Income Tax band.

- Tax is usually collected through an adjustment to the employee’s PAYE tax code, or through payroll, where the employer operates it.

Employers

- Employers pay Class 1A National Insurance Contributions (NICs) at 15% on most taxable Benefits in Kind.

- This is reported and paid via the P11D(b) form, with payment due by 19 July (or 22 July if paying electronically).

- Employers do not pay employee Income Tax; they are responsible only for Class 1A NICs and for reporting the benefit correctly.

Example:

An employer provides private medical insurance worth £1,200 per year. The employee pays Income Tax of £240 (at 20%) on this benefit. The employer pays Class 1A NICs of £180 (at 15%).

Explore the key aspects of PAYE forms and Income tax, National Insurance and the information you need to ensure that you are paying the correct amount of tax in these guides.

Common Examples of Benefits in Kind

Company Cars: Vehicles provided for personal use by the employer.

Health Insurance: Employer-paid medical services or private health insurance; however, some qualified life insurance policies are not treated as a taxable in-kind benefit for directors.

Childcare Vouchers: Financial support provided by the employer to cover childcare costs. If your employer does not provide support, there are childcare schemes that the government provides that you can avail. The scheme closed to new applicants in October 2018 and was replaced by Tax-Free Childcare.

Gym Memberships: Access to fitness facilities or an on-site gym paid for by the employer.

Personal Use of Company Property: Allowing personal use of company-owned assets, such as property or equipment.

Loans: Interest-free or low-interest loans granted by the employer.

Education Fees: Payment of tuition or other educational expenses by the employer.

Mobile Phones & Computers: Devices provided by the employer if being used for personal benefits.

Professional Subscriptions: Membership fees for professional organisations or subscriptions paid by the employer.

How to Calculate Benefits in Kind Tax

To calculate the Benefit in Kind (BIK) tax for standard benefits, determine the cash equivalent value of the benefit and multiply that by your income tax rate.

Annual BIK Tax Due = {Cash Equivalent Value} X {Income Tax Band}

For most Benefits in Kind, you take the following steps to calculate:

- Step 1: Determine the Cash Equivalent Value. The cash equivalent value is the cost to your employer of the benefit provided.

- Step 2: Employee Contributions. If you contribute to the cost of the benefit, this will need to be adjusted for.

- Step 3: Apply Your Tax Rate to the Remaining Value. The value that remains will be multiplied by your personal income tax rate.

Practical Example: Private Medical Insurance

An employer pays £1,200 per year for an employee’s private medical insurance. The employee pays no contribution.

- Cash equivalent value: £1,200

- Employee at basic rate (20%): £1,200 × 20% = £240 tax per year

- Employee at higher rate (40%): £1,200 × 40% = £480 tax per year

- Employer’s Class 1A NICs (15%): £1,200 × 15% = £180

Practical Example: Interest-Free Loan

An employer provides a £15,000 interest-free loan. The HMRC official rate is, for illustration, 2.25%.

- Taxable benefit = £15,000 × 2.25% = £337.50

- Employee at 20%: £337.50 × 20% = £67.50 tax per year

Note: Loans with a combined outstanding balance under £10,000 throughout the tax year are exempt from BIK tax.

Company Car BIK

Company car taxation is one of the most important areas of Benefits in Kind. The tax liability can vary based on the vehicle type, its CO2 emissions, and the fuel. Learning how the calculation works helps both employers and employees make more tax-friendly decisions.

How Company Car BIK is Calculated

Company car BIK is not based on the cost to the employer. Instead, it uses two key variables:

- The car’s P11D value (list price including options, VAT, and delivery, but excluding road tax and first registration fee)

- The appropriate percentage, which is determined by the CO2 emissions of a vehicle

Annual BIK Value = P11D Value × Appropriate Percentage (CO2 rate)

CO2 Emissions and Appropriate Percentage

HMRC publishes CO2 percentage bands each tax year. As CO2 emissions increase, the appropriate percentage rises. As a result, you need to pay a higher BIK value and more tax. Vehicles using petrol and diesel fuel generally attract higher percentages than other vehicles.

Company Car: BIK Calculation (Petrol Vehicle)

Car P11D value: £30,000

CO2 emissions: 120g/km (example appropriate percentage: 30%)

Annual BIK value: £30,000 × 30% = £9,000

Employee at basic rate (20%): £9,000 × 20% = £1,800 tax per year

Employee at higher rate (40%): £9,000 × 40% = £3,600 tax per year

Employer’s Class 1A NICs (15%): £9,000 × 15% = £1,350

BIK on Electric Vehicles

Fully electric vehicles (EVs) have a lower BIK tax, which makes them one of the most favourable company car choices. This has made EVs more popular through employer schemes, particularly in combination with salary sacrifice arrangements.

Company Car: BIK Calculation (Electric Vehicle)

Car P11D value: £40,000

CO2 emissions: 0g/km (example appropriate percentage: 2%)

Annual BIK value: £40,000 × 2% = £800

Employee at basic rate (20%): £800 × 20% = £160 tax per year

Employee at higher rate (40%): £800 × 40% = £320 tax per year

Compare this with the petrol example above: a higher-value EV can generate less BIK tax than a lower-value petrol car.

Fuel Benefit

If an employer also pays for private fuel used in a company car, a separate fuel benefit charge applies. This is calculated using the same CO2 appropriate percentage applied to a fixed ‘fuel benefit multiplier’ set by HMRC each year. For many employees, private fuel benefits create a large tax liability and are often not effective unless private mileage is very high.

Fuel Benefit Calculation

HMRC fuel multiplier: £27,800

CO2 appropriate percentage: 30%

Annual fuel benefit: £27,800 × 30% = £8,340

Employee at 20%: £8,340 × 20% = £1,668 additional tax per year

Employees should carefully assess whether a private fuel benefit is cost-effective given their actual private mileage.

Why Some Vehicles Create Higher Tax Liabilities

High CO2 emissions have a direct impact on the appropriate percentage, raising the BIK value even if the car’s list price is not high. For example, a £25,000 petrol SUV with high emissions can generate more BIK tax than a £40,000 electric vehicle. Employers and employees should consider the BIK tax in their vehicle decisions, not just the monthly lease cost.

To explore a full comparison of company car versus car allowance options, see our complete guide: Company Car or Car Allowance: Which Is Better For You?

Taxable and Exempt BIK

HMRC classifies benefits into three categories. Understanding this structure can help employers and employees plan more effectively.

1. Fully Taxable Benefits

| Benefit | Notes |

| Company cars | Based on the P11D value and CO2 emissions |

| Private medical insurance | Full cost to the employer is taxable |

| Living accommodation | Based on the annual property value |

| Gym memberships | Off-site or external gyms |

| Personal travel paid by the employer | Non-business travel only |

| Assets for personal use | 20% of market value per year |

| Non-qualifying gifts and vouchers | Where not meeting the trivial benefit rules |

2. Exempt Benefits (0% Tax)

| Benefit | Notes |

| Employer pension contributions | Within annual allowance limits |

| Cycle to Work Scheme | Must meet HMRC conditions |

| One mobile phone per employee | Contract must be in the employer’s name |

| Business travel expenses | Wholly and exclusively for business |

| Work-related training | Must be relevant to the employee’s role |

| Workplace parking | Provided at or near the place of work |

| Eye tests and corrective equipment | Where VDU use is required for the role |

| Office facilities | Used at the employer’s premises |

| Staff discounts | On the employer’s own goods and services |

3. Threshold-Based Exemptions

| Benefit | Threshold | Conditions |

| Trivial benefits | Under £50 per benefit | Not cash, not contractual, not performance-related |

| Interest-free loans | Under £10,000 total outstanding | The combined balance must remain below the threshold all year |

| Staff annual parties/events | £150 or under per head (incl. VAT) | Open to all employees; covers total event cost, including transport and accommodation |

What Is Not Considered a Benefit in Kind?

Examples include:

- Salary and wages

- Bonuses

- Commission payments

- Overtime payments

- Statutory payments

These are taxed through payroll as earnings rather than Benefits in Kind.

Salary Sacrifice and BIK

Salary sacrifice is a formal arrangement between an employer and employee. Here, the employee agrees to give up part of their gross salary in exchange for a non-cash benefit. As the benefit replaces gross salary, both the employee and the employer can save National Insurance and, in some cases, Income Tax.

How Salary Sacrifice Works

Under this arrangement:

- The employee agrees to reduce their gross salary by a set amount in writing.

- The employer provides a benefit like electric vehicles or others in exchange for that amount.

- The employee pays Income Tax and NICs only on the reduced salary, not merely on the sacrificed amount.

- The employer also saves on Employer NIC on the sacrificed portion.

Tax Treatment of Salary Sacrifice BIKs

For most benefits that fall under salary sacrifice, the normal BIK rules apply. However, a specific set of ‘exempt’ benefits is tax-friendly even when provided through salary sacrifice. These are called Qualifying Salary Sacrifice Arrangements.

Electric Vehicles via Salary Sacrifice

Electric vehicles are one of the most tax-efficient salary sacrifice benefits. As fully electric cars have a low BIK rate, adding salary sacrifice to EV vehicles can result in lower tax and NIC for both the employer and the employee compared to buying or leasing a vehicle on a private basis.

Example of EV Salary Sacrifice

Employee gross salary: £50,000

Monthly EV lease cost via salary sacrifice: £500

Without salary sacrifice:

Cost to employee: approximately £500/month from net pay = £833/month gross equivalent

With salary sacrifice:

BIK value: £800 per year | Income Tax (40%): £320 per year

Plus salary sacrifice: £6,000 per year

Approximate total annual cost to employee: £6,320 (compared to £9,996 equivalent outside salary sacrifice)

Note: This is just an example. Individual outcomes vary based on salary, tax band, vehicle P11D value and specific scheme terms.

Other Common Salary Sacrifice Benefits

- Pension contributions

- Cycle to Work Scheme

- Childcare (legacy voucher schemes)

- Additional annual leave purchase

Salary sacrifice arrangements must be in writing and cannot reduce pay below the National Living Wage. Employers should make sure that scheme documentation is accurate to comply with HMRC requirements. Speak to a specialist payroll adviser before applying or making changes to a salary sacrifice arrangement.

Learn more about this employee benefit option where workers can exchange a portion of their monetary salary for non-monetary benefits in this guide.

How to Report Benefits in Kind to HMRC

When reporting BIK to HMRC, employers need to include the value and the tax rates applied. This covers employee information, the type of benefit and its cash value. Employers must also submit a P11D(b) form for benefits not covered through payroll, and pay 15% Class 1A National Insurance on most taxable perks.

The P11D submission deadline is 6th July, and the Class 1A NIC payment is 19th July (or 22nd July if paying online). Employers should file within these deadlines to avoid penalties.

| Requirement | Deadline |

| Employee copy of P11D | 6 July |

| HMRC P11D submission | 6 July |

| Class 1A NIC payment | 19 July |

| Electronic payment | 22 July |

Payrolling Benefits in Kind

Introduced in 2016, Payrolling BIK will be mandatory from April 2027. It helps employers to account for monthly tax payments instead of completing an annual P11D form. The BIK value is included in the employee’s monthly taxable salary, so tax is collected gradually through payroll.

Before the tax year starts, employers must register through HMRC’s online service, which will then update employees’ tax codes accordingly.

You should contact our payroll accountant to understand the latest implications and avoid any extra tax burdens. Your payroll services provider can complete this registration on your behalf.

Benefits of Payrolling For Employers

- Makes reporting simple and reduces end-of-the-year paperwork

- No need to submit P11D forms for payroll benefits; P11D(b) may still be required

- Compliance with HMRC requirements

- BIK value is included in employees’ taxable pay, deducting tax when benefits are provided

Note: Regular deductions, rather than lump-sum payments, may cause some fluctuations in the employer’s cash flow.

If you are an employee or employer and want to learn about deductions from your gross pay or earnings, you should read the guides below.

Benefits of Payrolling For Employees

- Tax on benefits is deducted throughout the year, improving budgeting and reducing year-end liabilities.

- Revised payslips will clearly show benefit values and the relevant tax deductions.

- HMRC will update tax codes to deduct the correct amount of tax throughout the year

- Employees no longer need to wait for P11D forms to determine their BIK tax obligations.

Learn whether National Insurance Contributions are applicable to pension income in this guide.

Benefits in Kind for Directors

Directors are generally taxed on Benefits in Kind in the same way as employees. However, directors often receive benefits such as company cars, private medical insurance, loans and living accommodation, making BIK compliance particularly important for owner-managed businesses.

Payroll Implications for Employers

Employers who want to implement payroll should review their payroll systems to accommodate BIK values in monthly payroll calculations. Payroll software will need to hold benefit values for each employee and add these to taxable pay each pay period. Employers should also inform employees before payroll begins, as their tax codes will change.

Difference between Cash Benefits and Benefits in Kind

| Cash Benefits | Benefits in Kind | |

| Form | Direct payments like bonuses | Non-cash perks and advantages |

| Tax treatment | Taxed as income through payroll | Valued by HMRC and added to taxable income |

| Examples | Salary, bonuses, commission | Company cars, health insurance, gym memberships |

Conclusion

Understanding benefits-in-kind taxes helps both employers and employees to properly manage their tax liabilities. Employers need to correctly calculate BIK values, meet all HMRC requirements, and provide accurate reporting to avoid penalties, fines and interests.

You need to review your payroll systems to check compliance. Salary sacrifice arrangements, especially for electric vehicles, also offer meaningful tax efficiencies worth exploring with a qualified adviser.

You can contact our tax advisers for specialist advice on BIK.