A value-added tax (VAT) is a universal consumption tax based on the value added to goods and services at each stage of production and sale. It applies to almost all goods and services bought and sold for use or consumption in the UK. Items sold for export or services provided to clients in other countries are generally zero-rated and do not include VAT. The VAT treatment of services supplied to overseas customers depends on place-of-supply rules and may be outside the scope of UK VAT rather than zero-rated

Key Points About VAT

VAT is a wide-ranging tax covering all commercial operations, including the production, advertising and distribution of products and services. Businesses below the VAT registration threshold are not required to charge VAT on their sales.

VAT-registered businesses collect VAT on taxable sales and may recover eligible VAT on business purchases. The final economic burden usually falls on the end consumer.

Levied as a percentage of the purchase price, the tax burden is spread across the entire manufacturing and distribution process.

From April 2022, MTD for VAT is compulsory for all VAT-registered businesses to keep records digitally and submit returns using compatible software, regardless of turnover. Learn more about MTD for VAT and MTD for ITSA in our guides.

A partial payment method enables VAT-registered businesses to deduct from the VAT they have collected the tax they have already paid to other taxable parties on purchases made for their commercial operations. This ensures the tax is neutral regardless of the number of transactions.

Although the customer pays VAT as part of the purchase price, it is the seller, as the ‘taxable person’, who is responsible for accounting for and paying that VAT to HMRC. This is why VAT is an indirect tax.

Register your business for VAT and comply with HMRC rules with our VAT registration and VAT compliance services!

Explore our guides on postponed accounting, VAT registration, handling returns and managing VAT before registration:

How Does VAT Work?

VAT is charged based on the full selling price at each stage of an item’s production, distribution and sale. Each level in the supply chain assesses and collects the tax. This approach differs from a sales tax system, where the consumer is the only party responsible for paying the tax at the end of the supply chain.

For any earlier tax payments made by the taxable person, the VAT fraction of the sale price may be reduced. This prevents double taxation by taxing only the value added at each step of manufacture and distribution.

Since the ultimate price of the product equals the sum of the values added at each previous stage, the final VAT paid is the sum of the VAT paid at each stage.

New to VAT? Learn the VAT registration requirements and how to file VAT Returns in these guides.

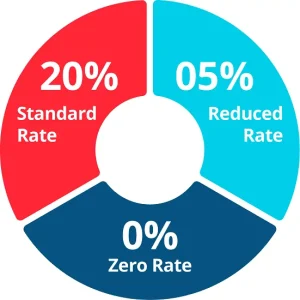

What are the VAT Rates?

The UK applies different VAT rates depending on the type of goods or services supplied. There are three categories:

Standard Rate

The standard VAT rate in the UK is 20%. It applies to the vast majority of goods and services, including certain food items excluded from zero-rating, such as ice cream, confectionery, and crisps.

Reduced Rate

The reduced VAT rate of 5% applies to goods and services, including children’s car safety seats, domestic energy-saving materials and mobility aids for older people. The tourism and hospitality industries are no longer classified under the reduced rate and are now subject to the standard 20% rate.

Zero Rate

Zero-rated goods and services have a nominal VAT rate of 0%. VAT is not applied to their sale, though they are still technically VAT-rated supplies. Items and services that are zero-rated in the UK include:

- Children’s footwear

- Medical and aid equipment (certain categories)

- Magazines and books

VAT rates can change, so always check the most current rates in effect.

VAT on Education can get complicated as few services are exempted from VAT, and you might have to pay VAT for others. Learn more in this guide.

Different Types of Value-Added Tax

VAT covers multiple business operations and can be complex to understand. Each type demands careful consideration to ensure accuracy and compliance. Some of the main types are:

- VAT on Land and Property

- Construction VAT

- VAT on Imports and Exports

- International Services VAT

- VAT on Buying or Selling a Business

Learn more about VAT Domestic Reverse Charge and Import One-stop-shop in these guides.

VAT Schemes

If your business is registered for VAT, you may be eligible to join a VAT scheme. The following are schemes you might want to consider:

- Flat Rate Scheme

- Annual Accounting Scheme

- Capital Goods Scheme

- Margin Scheme

- Retail Scheme

If your business is VAT-registered, you can join VAT schemes. Read our article to see how various schemes work and how you can use them.

Why Should You Register for VAT?

Registering for VAT allows your business to reclaim the VAT you pay on purchases. Businesses that are registered for VAT must include VAT on their sales invoices. If you are not registered, you still pay VAT on your purchases, but cannot reclaim it.

You must register for VAT if your VAT-taxable turnover exceeded £90,000 in the last 12 months, or if you expect your turnover to exceed £90,000 within the next 30 days.

Non-UK businesses making taxable supplies in the UK must register for VAT regardless of turnover. If you are a UK-based business, the normal VAT threshold applies.

VAT planning is crucial to save more on VAT and to avoid hefty fines and penalties. Get expert VAT advice with our professional VAT specialists.

How to Register for VAT?

There are two ways to register for VAT:

Through an Agent

You can have a VAT accountant or agent handle your VAT returns and liaise with HMRC on your behalf. Even when working through an agent, you may also register for a VAT online account once you have your VAT number and select the ‘VAT submit returns’ option.

Online

You may register for VAT by opening a VAT online account, often known as a Government Gateway account, to submit your VAT returns to HMRC.

VAT registration obligations vary depending on your business type. For example, community pharmacies, used car dealers, food businesses and the entertainment industry each have specific considerations:

Explore the latest VAT changes for community pharmacies, learn about VAT on used cars, food and business entertainment in these guides.

What if You Don’t Register for VAT?

If you fail to register for VAT when required, or cannot manage VAT complexities correctly, HMRC could issue significant penalties that may also damage your business reputation.

Services and Transactions Subject to VAT

Most goods and services are subject to VAT. The following are examples of taxable transactions:

- Sale of goods and services

- Hire or rental of goods

- Selling corporate property

- Gift-giving and bartering (in specific circumstances)

- Commission

Services Exempt from VAT

Some services are not subject to VAT, including financial, insurance and credit-related operations, training and education, and membership fees for certain organisations. Commercial property transactions may be subject to VAT where the landlord or seller has opted to tax the property. Without an option to tax, such supplies are generally exempt.

Conclusion

Value-added tax (VAT) is a consumption tax levied on the value added at each stage of producing goods or services. Each business in the value chain receives a tax credit for the VAT already paid, preventing double taxation. The final consumer bears the ultimate cost.

VAT was principally developed to eliminate the double taxation and cascade effects that were common under older sales tax systems. The consumer pays VAT progressively through each stage of the supply chain, from primary production to final sale.

Additional Resources:

Frequently Asked Questions About VAT

What is the current VAT rate in the UK?

The standard VAT rate in the UK is 20%. A reduced rate of 5% applies to certain essential goods and services, and a zero rate (0%) applies to items such as children’s clothing, books and most food.

Is VAT always 20% in the UK?

No. While 20% is the standard rate, a reduced rate of 5% applies to qualifying goods and services, and some items are zero-rated at 0%. Certain services are also fully exempt from VAT.

What is the VAT registration threshold in 2026?

The VAT registration threshold in 2026 is £90,000 of taxable turnover in a rolling 12-month period. If your taxable turnover exceeds this amount in any rolling 12-month period, or you expect it to do so within the next 30 days, you must register for VAT with HMRC.

What is the VAT deregistration threshold in 2026?

If you anticipate your taxable turnover will drop below the 2026 deregistration limit of £88,000, you may be eligible to cancel your registration. This process is not automatic; you are required to submit an application to HMRC. Furthermore, businesses that cease trading or no longer provide taxable goods and services must also deregister. It is essential to evaluate how this decision affects your ability to reclaim VAT, your market pricing, and your ongoing compliance requirements before proceeding.