What is Postponed VAT Accounting?

The end of the Brexit transition period (Dec 31, 2020) has brought many changes for UK VAT-registered businesses. A new system, “Postponed VAT Accounting,” is introduced for those who import goods into the UK.

Now businesses can record the VAT on their VAT Return rather than paying it instantly upon entry of the goods into the UK and claiming it later, effectively replacing the EU Reverse Charge mechanism. Importers have to pay VAT on any imports exceeding £135.

Previously, they would have to pay the import VAT immediately to avoid having goods held in customs, leading to a negative cash flow. To prevent this negative cash flow, the UK government introduced this postponed accounting for import VAT, also known as Postponed Import VAT Accounting (PIVA).

It is important to remember that postponed VAT doesn’t mean postponing the important declarations, which include sending the complete information to HMRC about your goods by up to 175 days on a supplementary declaration.

How Does It Work?

Postponed import VAT accounting (PIVA) allows businesses to declare and immediately recover import VAT in their regular VAT returns. However, If you want to use the postponed VAT accounting, you need to fill out several fields accordingly for both; customs declaration and VAT return.

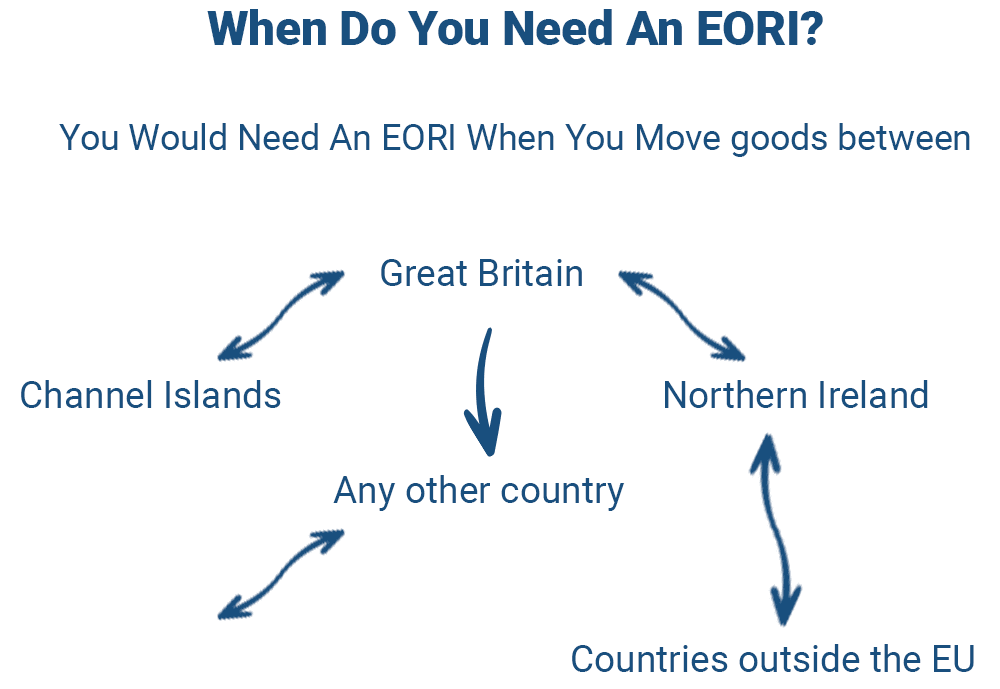

What is an EORI?

EORI stands for Economic Operations Registration and Identification Number. This EORI number is required if you are moving goods for a business purpose from one place to another, such as

- Great Britain (England, Scotland and Wales) or the Isle of Man and any other country (including the EU)

- Great Britain and Northern Ireland

- Between Great Britain and the Channel Islands

- between Northern Ireland and countries outside the EU

However, you don’t need an EORI number if you are moving goods for personal reasons. You can check your EORI number online as well.

How Can You Get an EORI?

To get an EORI number, your business needs to “be established” or “have a presence” in the country you want to import or export into, in this case, the UK. Your presence in the country includes:

- A registered office

- A central headquarters

- A permanent business establishment – premises where your business’s various customs-related activities can take place also, your HR and technical resources are permanently located there.

When would You Need an EORI?

You need an EORI number in case:

- You need to appoint someone to deal with your customs. Also, if you are ‘established’ in the country, you’re importing to or exporting from

- You need to make customs declarations.

- You want to use customs systems, such as the CHIEF system and the Import Control System Northern Ireland (ICS NI)

- You want to apply for a customs decision.

Why Was Postponed VAT Accounting Introduced?

The UK government introduced the postponed VAT accounting scheme to help reduce the negative impact on small businesses cash flow by delaying the VAT payment. Commercial goods over £135 entering the UK would be held at customs until VAT and customs were cleared.

UK VAT-registered businesses can apply for import VAT under PVA without any authorisation requirement if:

goods are imported for business purposes and relate to taxable supplies made by the business

The business provides its EORI and VAT registration number details and declares it uses PVA on its customs declaration.

Do You Have To Use PVA?

However, the use of the postponed VAT accounting scheme is optional. You can pay the VAT right at the moment when the goods enter free circulation in the UK — at the port of entry, for example, or after release from a customs warehouse.

If you choose not to take advantage of the postponed VAT accounting scheme, you will need to obtain monthly C79 reports from the HMRC. These reports are the alternative to PVA and still are necessary to import goods from non-EU countries.

However, it is suggested that businesses should utilise this scheme as it provides significant cash flow benefits compared to the alternative of paying the import VAT when the goods are imported.

How Can You Use PVA?

To use postponed VAT accounting, an importer needs to enter a code on the import declaration. This code will allow the VAT on import liability to be accounted for by the importer in their VAT Return. The VAT Return includes new boxes (fields) to record this information. The importer should not enter the relevant code if an importer wants to pay VAT at the time of importation.

How to Tell HMRC that You Want to Use PVA?

There is no specific process to opt for PVA, and you do not need to tell HMRC in advance if you want to start accounting for import VAT on your VAT return. You must confirm in your customs declaration that you are using the PVA scheme.

If you choose the CHIEF system (Customs Handling of Import and Export Freight) on your declaration:

- Enter your EORI number starting with ‘GB’ (Great Britain), which includes your VAT registration number into BOX 8, or, if applicable, your VAT registration number in box 44h.

- Enter ‘G’ as the method of payment in Box 47e, which confirms your selection of the PVA scheme.

On your declaration, If you opt for the Customs Declaration Service (CDS):

Enter your VAT registration number. However, VAT will only be recorded against your EORI and at the declaration level.

How to Complete your VAT Return When Using PVA?

After selecting PVA on your customs declaration, you need to account for import VAT after completing your VAT return for the accounting period, including the date you imported the goods.

To complete your VAT return, you will need

- Details of any customs entries you have made in your records

- Online schedule of imports to download monthly instead of a C79

Entries will be made as follows:

Amount of Postponed Import VAT based on the PVA statement published by HMRC. It is the import VAT that the business has postponed.

Box 1

Include the postponed VAT for the period for which the VAT return is done. Should match with the monthly statement

Box 4

Include the VAT that has been reclaimed for the VAT period on the imports that have been accounted for in the PVA.

Box 7

Include the full value of the imported goods for the period, excluding any VAT.

Postponed VAT on Your Customs Declaration

Custom declarations are complicated, however, many businesses hire transporters or customs agents to complete the customs declaration process. Your agent should know that you opt for the PVA scheme in such a case. You must pay the VAT on the spot if the box is filled incorrectly. Also, you should keep records of your previous VAT returns.

For postponed VAT on the customs declaration, you need to enter your:

- EORI number.

- Your “GB” (Great Britain) or “XI” (Northern Ireland) EORI number

- Your UK VAT number

- Use code “G” in Box 47e (method of payment) – it allows you to use the Postponed VAT Accounting scheme; therefore, customs will not hold your goods.

Postponed VAT Accounting and Northern Ireland

Northern Ireland is considered a part of both the UK and the European Union (EU). Therefore, it has specific VAT and custom conditions for businesses.

PVA rules for trade in goods and services

- The trade of goods between Northern Ireland and Ireland is unchanged.

- The movement of these goods remains intra-Community supplies and acquisitions; therefore, PVA is unnecessary.

- The reporting obligations for these trade transactions remain the same.

- The Electronic VAT Refund (EVR) system is available for VAT expended in Northern Ireland with goods.

- For B2B imports with a value below £135, postponed import VAT accounting is necessary.

- EU simplifications, such as call-off stock and triangulation, will continue to apply.

What are the Benefits of Postponed VAT Accounting?

PVA has significantly improved the cash flow for thousands of importers. At first glance, this scheme seems quite complex — you pay the applicable import VAT afterwards rather than upfront. However, from an accounting point of view, there is much more for importers.

Technically, when the importers account for the VAT on their return, their input and output VAT balance out effectively. Furthermore, instead of paying import VAT immediately, they can reclaim it later by paying the VAT by accounting for it on their return without making a physical cash payment.

Additional Resources

Conclusion

Overall, this scheme is considered a welcome measure as it aims to reduce a negative cash flow impact on businesses by avoiding the goods being held in customs until VAT is paid. Consequently, the businesses now have the potential to see cash flow benefits if they already import goods from outside of the EU, as it removes the need to account for import VAT. It is however always advisable to speak to a good VAT Accountant to ascertain the advice that’s most suitable to your situation.