A recent report confirmed that an average of £1.5 billion is spent on various events and corporate hospitality. The size of the event industry itself is about 35% of the overall UK economy. With such large transactional movements, it makes sense for a Business to understand business entertainment and the impact it can have on its tax position. Our team of specialist tax accountants and researchers have worked hard to curate an in-depth guide explaining how VAT on business entertainment and VAT on staff entertainment work when providing corporate entertainment to businesses, clients, employees, and stakeholders.

What is Entertainment?

Entertainment does not work just for business purposes, but the correct choice of the type of entertainment can help in increasing and expanding your business. There are guidelines set by HMRC for what comes under the definition of entertainment.

- If you have provided free food and drink to the customers or employees

- The provision of free accommodation to the recipient

- If you buy tickets to a cultural event for your overseas customers

- Concert tickets, entry to theatres

- Free entry to clubs and other such facilities

- If you buy tickets for your customers for a sporting event.

- Any costs incurred while hiring third-party organisers to organise the corporate event.

- free Vouchers, samples, and business gifts

What is Business entertainment?

Entertainment in the corporate world is not much different from its real meaning, as it is an act of hospitality offered by a business entity to its clients, stakeholders, or employees for the very purpose of entertainment and goodwill gesture. Business entertainment can be a social activity or an invitation to a dinner or a sporting event, and by organising such events, businesses reinforce their company’s image, brand vision, and values while leaving their guests with a memorable experience to cherish.

Businesses in the UK might not even know how they’ve been providing entertainment to their customers and could have claimed tax reliefs in return, nor do they know about the corporation tax treatment to such events.

Different pitfalls make it hard for businesses to actually claim the corporation tax relief on business entertainment, even if they claim to understand it. Multiple conditions and rules further complicate the identification of allowable expenses for a hospitality business. In some situations, the claimed business expenses can imply that your customers or clients have received “benefits in kind” making them liable to pay the taxes of those benefits. Therefore, consulting your business accountants would help you identify other pitfalls depending on the nature of the business entertainment you intend to provide.

Types of Business Entertainment

There are different forms of entertainment through which you can make your employees and non-employees feel welcomed and pave new opportunities for your business. Entertaining employees and clients through corporate events and dinners is the most common practice in the corporate world, yet not the only entertainment type.

Business entertainment can be the provision of capital assets like yachts and aircraft for transportation or luxury suites for overnight accommodation. Moreover, It can be reserving a seat for your clients for concerts or cultural festivals. If your clients are sports enthusiasts, booking corporate seats in the stadium will help massively put up an empathetic first impression. However, HMRC has some standard rules to differentiate between employees and non-employees that might be different from general perception.

Who are Employees and Non-Employees as per HMRC

HMRC strictly clarifies in its ruling about who is to be considered as employees and who will be excluded from business entertainment.

An employee on whom you may reclaim input tax includes:

- Your employed person, currently on the payroll of the business

- Directors or partners of the business

- Self-employed persons whom you treat with the same subsistence as you treat your employees (subsistence expense only).

- Helpers or caretakers who are considered essential for the operations of events.

In contrast, a non-employee includes retired pensioners, terminated employees, job applicants, and interviewees. Moreover, a person holding some shares in your business but who is not an employee would be considered a non-employee and can be treated as a customer or client.

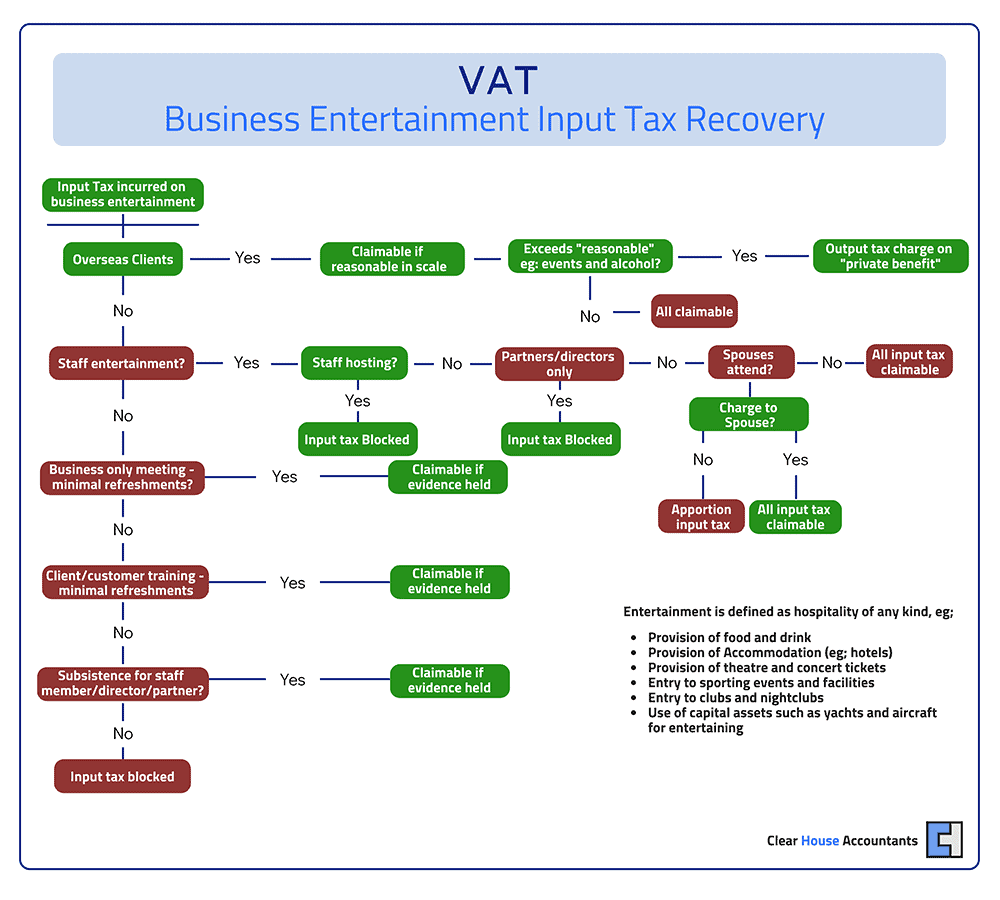

Video: VAT on Business Entertainment

VAT might be one of the most complicated Taxes to understand in the UK, along with its reliefs and exemptions. One such relief is the VAT relief on business entertainment, and this video explores how this relief works.

VAT on Business Entertainment Expenses

An entertainment provided just for the sake of entertainment may not be considered; however, if the entertainment provided was for the sole purpose of business, then HMRC may consider the costs as allowable. HMRC has different considerations for VAT on business entertainment costs and may not allow much tax relief, but in a few exceptional cases.

Exceptional cases exempted for disallowable expenses

Sporting Bodies and Airlines

Sports bodies like FIFA and UEFA use business entertainment to market and increase their viewership. HMRC puts this case in the business entertainment category and allows you to reclaim VAT. Likewise, Airlines can recover the input tax for the provision of food and accommodation for the passengers if their flights are delayed.

Goods and Services

If goods and services are used entirely for business entertainment, you get an exemption from VAT, provided it fulfils the policies set by HMRC. In the case of goods and services used partially for business entertainment and partially for non-business entertainment, VAT becomes due on the full price. However, in both cases, the main goal still gets fulfilled as entertainment helps in making a positive impact on the enterprise, which helps in increasing brand value eventually.

Entertaining Clients or Overseas Customers

Tax relief on client entertainment is not allowed, with the only exception in the case of overseas customers. Additionally, an overseas customer should not be entertained through corporate hospitality events like concerts. Overseas customers technically mean the clients not carrying on a business or ordinary residence in the UK. You can recover VAT incurred on the business entertainment for overseas customers if it is for the sole purpose of business and is within the cost limits of £150 per head.

In cases where the expenditure is necessary and for strict business purposes, the private use may be ignored. Hospitality provided because it would be polite, it’s expected, or because it would improve relationships is not for strict business purposes. However, as mentioned above, the receiver might be subjected to input tax implications if there is a private benefit involved, while removing the chances to recover any input tax.

VAT for Staff Parties

Most organisations in the UK reward their staff with an annual Christmas party or annual dinner. It can be a tax-free benefit for an enterprise if the cost per head is below £150.

There are a few conditions that apply to such tax relief. One is that the event organised is for all staff members and not just for directors or partners. Secondly, the total event costs including costs incurred on normal basic food and drink provision, accommodation, and travel (including VAT) should be under or £150 per head. If the costs hit above the price limit or a few of the staff members miss out, you will be liable for tax implications on input tax.

If you had multiple events in a year for the staff and they all collectively meet the above criteria of being within the price limit and the inclusion of all staff members, then you can recover incurred tax on all events.

Other Tax Implications on Staff Parties

Mixed Gathering

If you have organised an annual party for your staff and allowed them to join the party with additional guests, in that case, you can recover the VAT on input tax on the costs incurred on entertaining employees only. You are not allowed to claim any costs incurred on the guests your staff brought with them.

Staff Acting as Hosts

If the party hosted by your business is not just for the staff members, and your staff also acts as hosts for the guests, then you are no longer eligible to claim VAT incurred. A good example of such a case can be your staff welcoming and serving clients at annual parties.

Director or Partners as the Staff

If your business has only directors and partners with no other employees, then the enterprise is not eligible to claim VAT. However, directors or partners can claim VAT on their meals, travel, and accommodation if they are away from their original workstation for a business trip.

Difference Between Staff and Business Entertainment?

In a nutshell, Business entertainment relates to providing free entertainment to clients, sub-contractors, or vendors. On the other hand, employee entertainment is the provision of free entertainment to your hired staff. In both cases, a few things that remain common are business marketing and positive brand reputation, helping in business growth.

Some General

Marketing Expense:

If you are organising events having both entertaining and marketing purposes, you can still reclaim VAT on the marketing element of the events even if the costs are not allowable for the purpose of entertaining employees. However, you must itemise both elements convincingly for HMRC to actually consider the costs as an allowable marketing expense. A team of expert chartered accountants can help you claim those expenses while staying compliant.

Admission Fee:

If you organise an event that is chargeable to those attending, for example, an admission fee, then technically, you become eligible for full VAT relief on the event. However, whilst this is reasonable for a conference, a token charge for a restaurant meal will be difficult to pass off as an organised conference.

One important thing to know is that you can claim up to 83% of the tax paid for guests if you charge a minimal amount on their meals. In this case, entertainment is not free, so VAT is claimable. However, an expert VAT accountant can analyse better depending on events and businesses, as this guide is curated considering general criteria.