In this UK Personal Tax guide by Clear House, you’ll explore Income Tax, NICs, Capital Gains Tax, dividends, pensions, Inheritance Tax, savings interest, student loans, HICBC, and personal tax allowances. The guide also covers tax rates, allowances, and filing rules.

Before we discuss each tax in detail, let’s start with the basics of personal taxes!

What are UK Personal Taxes?

UK Personal taxes are levied directly or indirectly on individuals (not companies) on their personal income, gains, assets, and spending. These are further divided into categories.

- Direct personal taxes: paid directly by you, like Income Tax, National Insurance, Capital Gains Tax, Dividend Tax, IHT, etc.

- Indirect personal taxes: these are added to the price of goods/services and collected by businesses, such as VAT, fuel duty, and excise duties.

Where Do You Fit?

If you’re not sure where to get started, you can jump straight to taxes that matter most to you. You can just click on the taxes you are interested in.

Employees: If you are an employee, you might focus on Income Tax and National Insurance (NI). It covers how you are taxed and how much salary is deducted through PAYE.

Self-Employed (Freelancers): If you are self-employed or a freelancer, you can explore Income Tax, NICs, and Self-Assessment to report and pay your taxes.

Landlords: If you are a landlord with rental income, you can check how Income Tax (tax on rental income) and Capital Gains Tax work.

Company Directors: Directors can explore the details of Dividend Tax and Income Tax to learn how they are taxed .

Investors: Investors who invest in shares or assets can visit the Capital Gains Tax, Dividend tax, Foreign Income Tax, Chargeable Event Gains, and Saving Interest Tax, along with the Personal Saving Allowance, to minimise their taxes.

Beneficiaries: Estate beneficiaries can get detailed information on thresholds, exemptions and reliefs related to Inheritance Tax (IHT).

Pension Holders and Retired Personnel: They can explore Income Tax, Pension Tax, and Retirement Tax to learn about the tax implications and available relief.

High Earners: Our guide covers the High Income Child Benefit Charge (HICBC), Capital Gains Tax, Foreign Income Tax, Chargeable Event Gains, Income Tax, and Self Assessment Reporting requirements.

No matter which category you fall into, understanding personal taxes helps you make informed decisions for a safe and secure future. Read on to explore how learning personal taxes protects you.

Why Personal Taxes Matter

Complying with Personal tax helps you save money, avoid costly mistakes, and reduce stress. Getting it wrong can be financially and emotionally costly. It impacts major financial decisions.

Income Tax and NICs reduce your take-home pay. You pay Capital Gains Tax and Dividend Tax when selling shares or buy-to-let. Stamp Duty Land Tax is applied when buying a house. Pensions are also taxed when withdrawn.

Non-compliance, like missing a Self-Assessment deadline, can lead to penalties, interest, and even HMRC enquiries. However, good personal tax planning can save you from punishments and reward your time and attention.

Income Tax – The Core Personal Tax

Income Tax is the main personal tax in the UK, charged on most types of income. For employees, it is usually deducted from salary through PAYE. You pay this tax on profits from your business, interest and dividends from your savings and investments and when you buy-to-let.

Income Tax is charged based on your tax rate and band over your Personal Allowance of £12,570.

National Insurance Contributions (NICs)

National Insurance is a tax applied to earnings and self-employed profits. You start paying when you are 16 and earn over a certain amount. Class 1 National Insurance is deducted through PAYE from employees’ earnings, and employers also pay contributions.

Self-employed individuals pay Class 2 and Class 4 National Insurance based on their business profits.

Individuals in the UK pay tax on cryptocurrency and foreign income. Gains from crypto-assets are subject to CGT at 18% or 24% (2026/27). UK residents are generally taxed on their worldwide income. Depending on your circumstances, you may need to report foreign income through Self Assessment. For non-UK residents, UK-sourced income is taxable. Income earned outside the UK can sometimes be exempt.

Learn more about Income Tax and National Insurance in these guides.

If you sell, exchange, or gift an asset or valuable possession and make a gain over the tax-free allowance (£3,000 for individuals), you’ll need to pay CGT. Read on to explore CGT.

Capital Gains Tax (CGT)

Capital Gains Tax (CGT) is the tax on profit or gain by selling, giving, exchanging, or disposing of an asset. You only need to pay CGT over your Capital Gains tax-free allowance (£3,000). CGT rates depend on your income tax band and the type of asset.

If you’re new to Capital Gains Tax, looking for changes to CGT when selling property, or want to minimise your CGT, read these guides.

Now that you know the tax on property or asset gain, let’s explore whether you are exempt from paying tax on interest earned through savings.

Savings Interest Tax

Interest earned from savings is taxable. You can earn tax-free interest using allowances: your Personal Allowance (£12,570), which applies across your total income, Starting Rate for Savings (up to £5,000 if other income is £17,570 or less), and Personal Savings Allowance (£1,000 for basic-rate, £500 for higher-rate, £0 for additional-rate taxpayers).

Interest is taxable, but you may be able to earn some interest tax-free using available allowances. This includes banks, peer-to-peer lending, unit trusts, government bonds, building societies, and gilts. Tax is paid at your normal income tax rate (20%, 40%, or 45%) on interest beyond tax-free savings.

Tax is usually collected through tax code adjustments or PAYE. If you have untaxed income or large amounts, you may need to report it through Self Assessment. Interest earned in certain National Savings accounts and ISAs is tax-free and does not count towards your savings interest.

If you have invested in a company as a shareholder, you will pay dividend tax on your income earned from shares. Read on to learn more.

Dividend Tax

Dividends Tax is levied on the income you receive from owning shares in a company. Some of the dividend income is tax-free each year. The current dividend allowance is £500. The tax you pay on dividends above this allowance depends on your income tax band: 10.75% for basic rate taxpayers, 35.75% for higher rate taxpayers, and 39.35% for additional rate taxpayers from April 2026.

You may need to report dividends through Self Assessment if they exceed your allowances or are not fully taxed at source

Learn how dividend tax works in this detailed guide.

Inheritance tax can be overwhelming when you don’t know what it is. Let’s find it.

Inheritance Tax (IHT)

Inheritance Tax is applied to the estate (money, property, or possessions) of a deceased person. If your estate is below £325,000, or if the excess goes to your spouse, civil partner, charity, or community, it is generally non-taxable.

The standard Inheritance Tax of 40% (standard rate)is charged on part of the estate above the IHT threshold.

If you are looking for ways to reduce your Inheritance tax? Don’t miss this post.

If you are planning for retirement, you must not miss out on the retirement tax.

Pensions & Retirement Taxation

Pension or retirement income is taxable. You will pay Income Tax over the Personal Allowance. Income from an ISA is tax-free. From age 55 (57 from April 2028), you can usually get 25% of your pension tax-free, if it does not exceed the Lump-Sum Allowance (LSA) of £268,275.

Income Tax is usually deducted from pension payments by your provider, and you may need to submit a Self Assessment tax return depending on your income sources and level.

Pension income can add to your total income. This may push you into higher tax bands, reduce allowances, or trigger other charges. Planning and getting advice from a personal tax accountant can help you save tax.

If you want to maximise your retirement savings, don’t miss these guides.

In addition to these personal taxes, there are other miscellaneous taxes you need to be aware of.

Other Personal Taxes in the UK

These are some of the other Personal Taxes in the UK:

Student Loan Repayments

You repay these loans when your income exceeds a certain threshold. Repayments are usually made at the same time as tax or National Insurance when you are an employee. Repayments are usually made through PAYE or Self Assessment and are based on your income above the relevant repayment threshold.

High Income Child Benefit Charge

If you or your partner receives Child Benefit and either of you earns over £60,000 a year, the higher earner may pay the High Income Child Benefit Charge. This charge is 1% of your Child Benefit for every £200 of adjusted net income over £60,000.

If one of you earns £80,000 or more, you need to pay it back in full.

Crypto & Foreign Income

Individuals in the UK pay tax on cryptocurrency and foreign income. Gains from crypto-assets are subject to CGT at 18% or 24% (2026/27). UK residents are generally taxed on their worldwide income. Depending on your circumstances, you may need to report foreign income through Self Assessment. For non-UK residents, UK-sourced income is taxable. Income earned outside the UK can sometimes be exempt.

If you’re new to cryptocurrency, this post will show you how to start investing and why it’s worthwhile.

Chargeable Event Gains

Chargeable event gains are taxed as income. These may relate to a life insurance policy, capital redemption policy, or life annuity contract. Chargeable event gains on bonds are treated as savings income and taxed at the normal income tax rate (20%, 40%, 45%).

If you qualify for the starting rate for savings, up to £5,000 of income may be taxed at 0%, depending on your other income. Your non-savings income must be within certain limits after your Personal Allowance. You may also benefit from the Personal Savings Allowance (£1,000 for basic-rate, £500 for higher-rate, £0 for additional-rate taxpayers), which can reduce the tax payable on these gains.

Chargeable event gains are reported on Self Assessment. You may benefit from TSR relief to reduce the effective tax rate.

Personal Tax Allowances & Reliefs

These are some of the major personal tax allowances and reliefs:

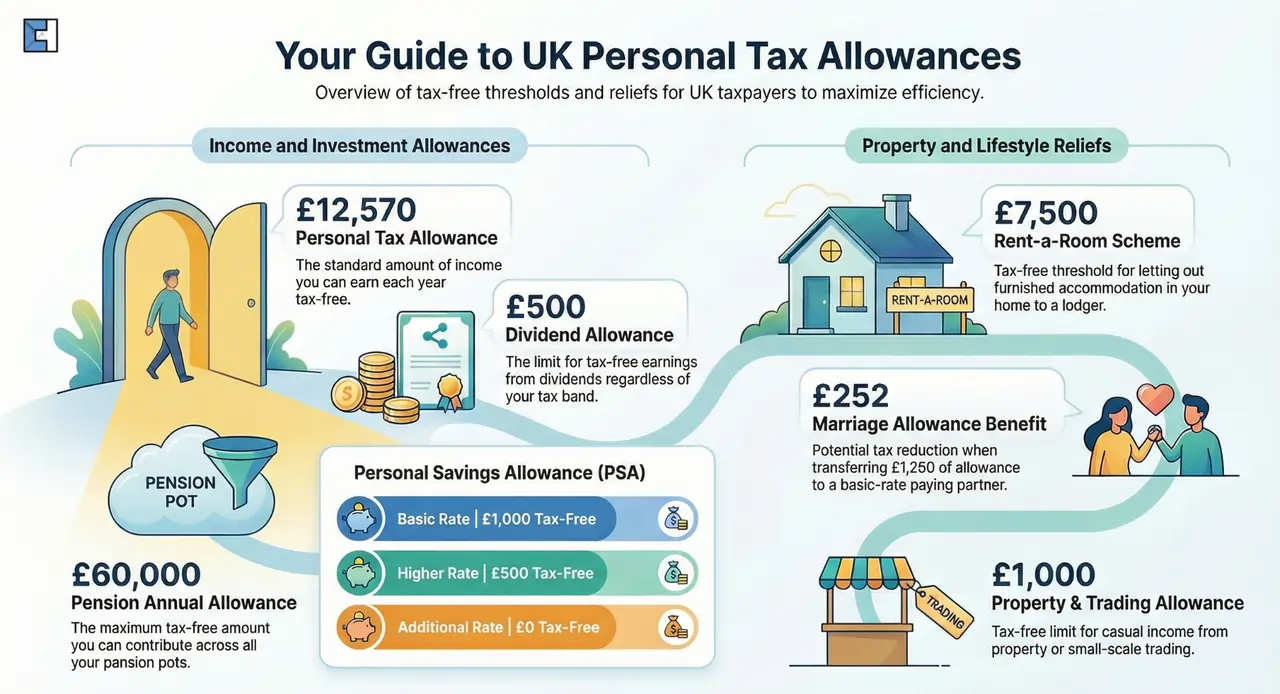

Personal Tax Allowance

The personal tax allowance is the amount of income exempt from tax. The current threshold of this allowance is £12,570. Income over this amount is taxable. The tax you pay in a year depends on your earnings over your personal tax allowance.

Personal Saving Allowance

With Personal Saving Allowance (PSA), you can earn interest on your savings tax-free. This allowance is applied based on your Income Tax band. Basic-rate taxpayers can earn £1,000 in savings interest; higher-rate taxpayers can earn £500; and additional-rate taxpayers do not get an allowance.

Dividend Allowance

Dividend allowance is the amount you earn from dividends without paying any tax on them. Currently, the allowance is £500. How much you pay on dividends over your dividend allowance depends on your Income Tax band.

Marriage Allowance

This allowance allows you to transfer £1,260 of your Personal Allowance to your spouse or civil partner. It brings down your tax by up to £252 in the tax year. To avail this allowance, you must be married or in a civil partnership, you don’t pay income tax, and your partner pays income tax at a basic rate.

Married couples and civil partners can save tax through valuable allowances and reliefs. Read this guide.

Blind Person’s Allowance

This allowance is an extra amount added to the annual Personal Allowance of blind or severely sight-impaired individuals. In 2026/27, the Blind Person’s Allowance is £3,250.

Property or Trading Allowance

The property allowance lets you get £1,000 tax-free from property or trading income each year. You do not need to declare this income on a tax return if it is £1,000 or less.

Rent-a-Room Scheme

The Rent a Room scheme allows owners, occupiers and tenants to let furnished accommodation to a lodger and receive up to £7,500 a year tax-free. You don’t need to be an owner to benefit from this scheme.

Pension Annual Allowance

Many people get relief from pension savings. Your annual allowance is the maximum amount you can save in your pension pots tax-free in a tax year. The annual allowance is £60,000 in a tax year. This allowance covers all your pensions.

Other personal allowances for individuals include Gift Aid and Pension Lump Sum Allowance.

Personal Tax Filing & Deadlines

Wondering when to file your personal tax? You’ll normally need to register for a Self Assessment tax return by 5 October following the end of the tax year in which you became eligible. For paper tax returns, the deadline is 31st October. The online tax return deadline is 31st Jan. To pay any due tax (including the first payment on account), the deadline is 31 January. The last date of the second payment on account (if applicable) is 31 July.

Conclusion

This comprehensive guide explains all major UK personal taxes. It will help employees, self-employed, landlords, investors, or pensioners protect their finances and avoid costly mistakes. If you are struggling with your personal tax compliance, a qualified personal tax accountant ensures accurate Self-Assessment, maximises allowance, minimises liabilities, protects you from penalties and handles your finances effectively.