UK taxes are collected at different levels. His Majesty’s Revenue and Customs (HMRC) is the system responsible for collecting and administering taxes at the government level, while councils are responsible for collecting taxes at the local level. The UK collected £1,139 billion in taxes in the financial year 2024/25, i.e., 39% of its GDP.

The primary taxes that uplift the state coffers are Income Tax, Value-Added Tax (VAT), National Insurance Contributions (NICs), Corporation Tax, Council Tax, and Capital Gains Tax.

England, Scotland, Wales, and Northern Ireland all fall under the ambit of the British fiscal system, with some changes in line with the local legal systems of the devolved governments (for instance, Scotland).

UK Taxes Administered by HMRC

HMRC is a non-ministerial government department authorised to collect taxes, pay state support and administer regulatory regimes. The taxes that are managed by the HMRC include:

- Income Tax

- National Insurance Contributions (NICs)

- Inheritance Tax

- VAT

- Capital Gains Tax

- Corporation Tax

- Insurance Premium Tax

- Environmental Taxes

- Stamp Duty

- Land and Fuel Taxes

- Climate Change Levy and Landfill Tax

- Customs Duties

- Excise Duties

UK Taxes Administered by Local Authorities

Council Tax and Business Rates are significant sources of revenue for local councils. These, along with several other fees, penalties and charges, are collected by the local authorities.

People Liable to Pay Tax in the UK

Individuals in the UK pay Income Tax and National Insurance Contributions (NICs) on wages, pensions, property income and interest. UK residents are generally taxed on their worldwide income and gains, while non-residents pay tax on UK-source income and gains.

Companies pay Corporation Tax on profits, and consumers pay indirect taxes such as VAT, fuel duty, and excise duties. Property owners pay Property Taxes, Capital Gains Tax and Council Tax.

Direct UK Taxes

Direct taxes in the UK are taxes that people and companies pay directly to the government based on their property or income. These taxes are non-transferable, meaning each taxpayer is responsible for paying them.

Personal / Individual Taxes

Personal taxes are paid on income, benefits, or gains of a personal or individual nature. These taxes include:

Income Tax

Income tax is paid on income or profits earned by an individual. PAYE (Pay As You Earn) is the system HMRC uses to collect Income Tax and NICs through employers. If income is not collected through PAYE or if extra tax is levied, self-employed and high earners report and pay tax to HMRC via Self-Assessment. UK income tax rates and bands:

| England/Wales/Northern Ireland Tax Band | Taxable Income | Tax Rate Applicable |

| Personal Allowance | 0 up to £12,570 | Nil |

| Basic Rate | £12,571 to £50,270 | 20% |

| Higher Rate | £50,271 to 125,140 | 40% |

| Additional Rate | Over 125,140 | 45% |

National Insurance Contributions (NICs)

UK taxpayers pay National Insurance contributions (NICs) to qualify for certain benefits and the state pension.

Class 1: Employees

Employers deduct Class 1 contributions from employees under State Pension Age and from employees with income over £242 a week from a single job.

Class 1A/B: Employers

Class 1A NICs, 15% (effective from 6 April 2025), are paid by employers on most taxable benefits. Class 1B NICs are payable on all items covered by the PAYE Settlement Agreement (PSA). Class 1B National Insurance is 15% (from 6 April 2025)

Class 3: Voluntary contributions

If you are not working, you can voluntarily pay Class 3 contributions to fill gaps in your National Insurance record and protect State Pension entitlement.

Class 4: Self-employed (profit-based)

If a person is self-employed, they pay Class 4 National Insurance based on the profit through Self-Assessment.

Capital Gains Tax (CGT)

Capital Gains Tax (CGT) is a tax on the profit or gain you make after selling an investment. You don’t have to pay it into tax-advantaged accounts like an ISA or a Self-Invested Personal Pension (SIPP).

Dividend Tax

You pay dividend tax on income received from shares over your Personal and Dividend Allowance.

Inheritance Tax (IHT)

Standard Inheritance Tax is levied at 40% on the property, money or possessions over the £325,000 threshold.

Pension & Retirement Taxes

Your pension is considered a part of your earnings, so it is taxable over your tax-free allowances. If you have invested or saved in an ISA, the gains are tax-free.

Savings & Investment Taxes

Savings are not taxed in the UK. Interest on savings is taxed as income. The profit made from the investment is taxed. Income and gains from savings and investments are taxable in the UK. With tax-free allowances, many people pay small amounts of taxes on savings and investments. Learn the current UK tax rules for these taxes.

Tax on Saving Interest

You can earn some interest from your savings tax-free. If your interest goes over your tax-free allowances, like the Personal Allowance, starting rate for savings and Personal Savings Allowance, you need to pay tax on it. Your tax band also lets you know how much tax you owe on your savings interest.

If your interest income/profit exceeds the threshold, you’ll pay tax at the standard Income Tax Rate. Then you may have to file your Self-Assessment Tax Return.

Tax on Bonds, Gilts, and Other Investment Income

Whatever you earn from bonds, excluding ISA, SIPP, or other tax-free wrappers, is taxable, and you need to pay income tax. Profit received as interest from gilts is also subject to income tax. This applies to all, whether you purchase bonds directly from a company or bond funds.

You need to report income and capital gains on your annual tax return or via an online CGT service if you have earnings from bond funds.

Stamp Duty Reserve Tax (SDRT) on Share Transactions

If you transfer ownership of chargeable securities, you need to pay stamp duty or Stamp Duty Reserve Tax (SDRT). Generally, the stamp duty is 0.5%, but it can go up to 1.5%.

Chargeable Gains on Life Insurance Policies

If you are getting profit or gains on life insurance policies as a chargeable event, they are considered income and are taxable. Chargeable gains are treated as savings income, and the policyholder can benefit from the Personal Savings Allowance.

Property Taxes

Property taxes are among the highest in the UK and contribute materially to overall tax revenue.

Stamp Duty Land Tax (SDLT)

SDLT is a tax charge on property purchases above a certain threshold. Scotland and Wales have their own property tax, rather than SDLT, which applies only in England and Northern Ireland. SDLT arises if:

- Freehold property is bought.

- A new or existing leasehold is bought.

- A property is purchased through a shared ownership scheme.

- Transfer of land or property occurs in exchange for payment.

Most buyers pay no SDLT on the first £125,000 of the property price. The remaining value is taxed progressively: 2% on £125,001–£250,000, 5% on £250,001–£925,000, 10% on £925,001–£1.5 million, and 12% on any amount above £1.5 million.

If you own another residential property at the time of purchase, you usually pay an additional 5% surcharge on each band (higher rates apply).

For non-residential land and properties, the nil-rate threshold is £150,000 (with different progressive rates above that).

Land and Buildings Transaction Tax (LBTT) – Scotland

Land and Buildings Transaction Tax (LBTT) is the Scottish equivalent of Stamp Duty Land Tax, payable when you purchase residential property or land in Scotland.

The tax is calculated progressively across different rate bands. Only the portion of the purchase price that falls within each band is taxed at that band’s rate.

Land Transaction Tax (LTT) – Wales

You pay LTT when buying land or property in Wales if the price exceeds the threshold. The current nil-rate threshold is £225,000 for both residential (main home only) and non-residential properties.

If you already own a residential property, higher rates usually apply unless you’re replacing your main home. LTT is self-assessed. You must file a return and pay any tax due (even if no tax is payable in some cases).

Annual Tax on Enveloped Dwellings (ATED)

ATED is an annual tax levied on entities owning high-value UK residential properties. This tax normally applies to companies, trusts, partnerships, open-ended investment companies, and other collective investment schemes that own property.

Non-Resident Capital Gains (NRCGT)

All non-residents (including individuals, partnerships, personal representatives, trustees and collective investment schemes) who dispose of UK land and property need to pay Non-Resident Capital Gains Tax. Granting a lease, a free transfer, or a gift of property attracts CGT. Both direct and indirect disposals of any interest in UK land fall under the scope of NRCGT for non-resident taxpayers in the tax year of disposal.

Tax on Empty Homes / Second Homes

You usually have to pay Council Tax on empty homes. The payment rate depends on how long your property has been empty. Short-term exemptions are there for major repairs, probate, marketing and armed forces cases.

If your property is furnished and is not your main residence, it is considered a second home. You might be charged up to 2 times your normal Council Tax as a second home premium. Discounts or exemptions are applied to annexes, job-related homes, planning restrictions, recent probate, or marketing for rent/sale.

UK Business Taxes

Every business in the UK needs to pay tax on its profits. The type of tax you pay depends on your business structure. Typically, businesses pay seven types of taxes.

Corporation Tax (CT)

Corporation tax is the main type of business tax paid by businesses on business income, investment income, and gains from the sale of assets. If a business makes around £50,000 or less, it is subject to a small profit rate of 19%. For businesses earning profits between £50,000 and £250,000, a 25% main rate tax is levied.

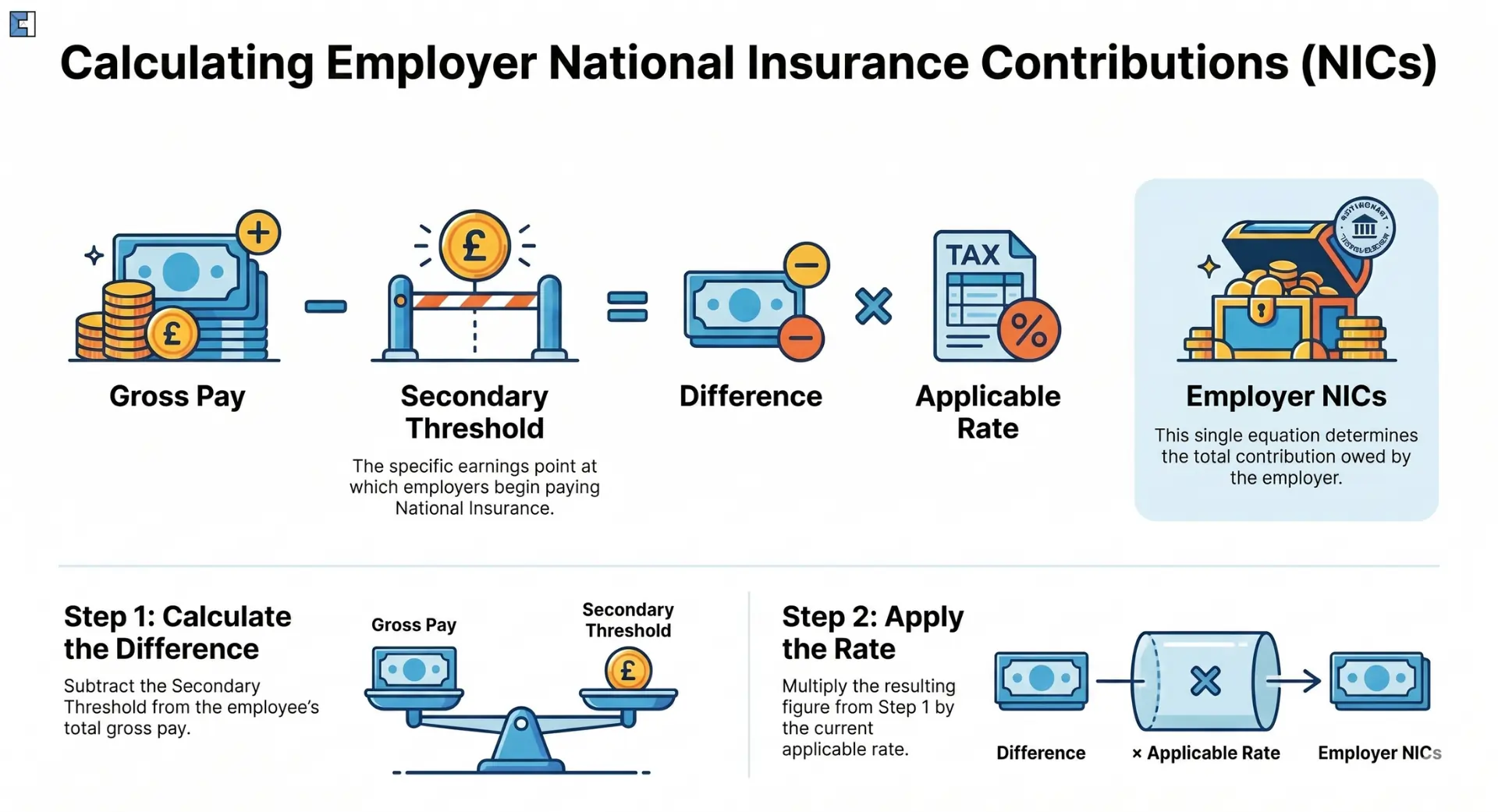

Employer National Insurance Contributions

Employers’ National Insurance contributions (NICs) are payments you make to HMRC for your employees who earn over a certain threshold. Employees pay their own Class 1 NICs, which are deducted from their pay by the employer. As an employer, you need to pay Class 1 secondary NICs, an extra amount based on employees’ earnings.

The current rate of employers’ NICs is 15%, and the secondary threshold is £5,000 per year.

Employer NICs = (Your employee’s gross pay − the Secondary Threshold) × Applicable rate

Apprenticeship Levy

The apprenticeship levy is paid at a rate of 0.5% by employers with an annual pay bill over £3 million. This levy is used to invest in apprenticeship training for the workforce. In Scotland, the UK Apprenticeship Levy funds modern apprenticeships. In Wales, this levy is used by the Welsh Government to encourage Worked-Based Learning (WBL) providers to deliver apprenticeships.

Construction Industry Scheme (CIS) Deductions

Contractors (sole traders, partnerships, or limited companies) must register with the Construction Industry Scheme (CIS) if they pay subcontractors for construction work, or if their business doesn’t do construction work but has spent over £3 million on construction in the 12 months.

While paying subcontractors, you need to make deductions. You need to make deductions of 20% for registered subcontractors, 30% for unregistered subcontractors and 0% if the subcontractor has ‘gross payment’ status.

These deductions are paid to HMRC and count as advance payments towards subcontractors’ tax and National Insurance Contributions.

Business Rates (National Non-Domestic Rates)

If you own non-domestic properties like shops, offices, pubs, warehouses, factories or holiday rental homes/ guest houses, you’ll have to pay business rates for using the building or part of it for non-domestic purposes. Business rates differ in Scotland and Northern Ireland.

They are calculated by multiplying the property’s rateable value (set by the Valuation Office Agency) by the business rate multiplier. The business rates multiplier is set annually by the government. There are two business rate multipliers. The standard non-domestic rating multiplier is higher to pay for small business rate relief. The small-business rate multiplier applies to small businesses.

Certain properties are exempt from business rates, such as farm buildings or places used for the welfare of disabled people. You’ll get a business rate bill in Feb or March each year from your local council. You can get business rates relief from your local council.

Digital Services Tax (DST)

DST is applied to a group’s businesses that provide social media service, search engine or any online marketplace to UK users. The businesses will pay Digital Services Tax when the group’s worldwide revenue from these digital activities exceeds £500 million and when £25 million of that revenue is derived from UK users.

If any group’s revenue crosses this threshold, its revenue derived from UK users will be taxed at a rate of 2%. The allowance limit is £25 million, meaning the first £25 million of revenue from UK users will not be subject to the Digital Services Tax. This tax can be calculated under an alternative calculation.

Personal and Business Taxes

Income Tax and National Insurance Contributions (NICs) are the second-largest source of tax revenue for the UK government (after VAT in most recent years), followed by Capital Gains Tax and other taxes.

Self-Employment Taxes (Income Tax + Class 4 NICs)

Self-employed individuals need to pay Income Tax and Class 4 NICs on the profits (after allowable expenses and capital allowances). Income Tax is calculated based on personal tax bands for employees.

Class 4 National Insurance is charged at 6% on profits between £12,571 and £50,270, and at 2% on profits above £50,270.

IR35 / Off-Payroll Working Rules

IR35 or off-payroll working refers to tax regulations designed to prevent tax avoidance through a middleman. It ensures that the worker (contractor), acting as an intermediary, pays the same Income Tax and National Insurance as an employee would.

Company Dividends for Owners

Dividends are taxable. They are subject to income tax and declared on the Self-Assessment tax return. After April 2026, the dividend rates for basic and higher-rate taxpayers will be 10.75% and 35.75%, respectively. Additional rate taxpayers will remain 39.35%. The Dividend Allowance is £500 in 2025/26 (tax-free).

UK Tax System for Foreigners

Foreigners living in the UK can be taxed based on their residence status. They need to pay taxes on UK-sourced income, and UK residents are liable to pay tax on worldwide income.

Automatic Exchange of Information (AEOI)

AEOI is an agreement that the UK has signed with several countries, facilitating the flow of information between HMRC and those countries’ tax authorities. Financial institutions in the UK, such as banks and insurance companies, are obliged to share information about non-UK residents with HMRC, which, in turn, will share it with the relevant authorities. Similarly, the UK receives information about its residents who hold overseas financial accounts or investments.

Short Term Business Visitors (STBVs)

You will be treated as a short-term business visitor for tax purposes if you have been working in the UK for less than a year and have lived in the UK for fewer than 183 days in the relevant tax year. These STBVs will be charged tax on their wages for work carried out in the UK. These taxes can be offset by double taxation treaties, provided there is one between the UK and the country of the concerned individual.

Foreign Income and Gains (FIG) Regime

From 6 April 2025, all UK residents need to pay taxes on their income and gains. The FIG regime offers relief from UK tax on eligible gains and income for the first four years of UK tax residence.

Taxes for International Students in the UK

International students who come to the UK from countries with double taxation agreements with the UK usually do not have to pay tax on tuition fees and living expenses such as accommodation, food, and study materials. However, if your living costs other than the tuition fee exceed £15,000, HMRC might ask you to account for that.

International Students might be liable to pay tax:

- If their country doesn’t have a double taxation agreement with the UK,

- If they have other income that they don’t bring to the UK, or

- If they do bring the income to the UK and use it on expenses besides the living costs or course fees, and

- If they plan to permanently stay in the UK.

Indirect UK Taxes

Indirect taxes are levied on consumption, added to the price of goods and services, collected by businesses, and paid to HMRC.

Sales & Consumption Taxes

Here is the list of sales and consumption taxes in the UK:

Value Added Tax (VAT)

Value-added tax (VAT) is a tax charged on the purchase of goods and services. VAT is administered and collected by HMRC and is the second-largest source of government income. VAT is charged at three different rates depending on the nature of the products and services purchased.

| Band | Rate of VAT | Goods and Services Covered |

| Standard Rate | 20% | Most goods and services |

| Reduced Rate | 5% | Some goods and services, like domestic energy |

| Zero Rate | 0% | Goods and services like food and children’s clothes |

Read to analyse VAT’s implications and to mitigate the liability resulting from it.

Insurance Premium Tax (IPT)

Insurance Premium Tax (IPT) is charged on all general insurance premiums. Everyone who buys insurance needs to pay IPT. It includes commercial and landlord insurance. There are two rates: a standard rate of 12% and a higher rate of 20% for certain insurances, such as travel insurance, electrical or mechanical appliances insurance, and vehicle insurance.

There are a number of exemptions from this tax, including:

- Reinsurance

- Long-term insurances (most)

- Insurance for commercial aircraft and ships

- Insurance on commercial goods in international trade

- Insurance premiums for risks involved in countries outside the UK (liable for other countries’ tax)

Soft Drinks Industry Levy (SDIL)

In 2016, the UK government introduced this levy to reduce obesity. It is applied to the production and importation of soft drinks containing added sugar. The current (1 April 2025) SDIL rates are:

- £1.94 per 10 litres of standard rate applied to drinks containing sugar between 5 grams and up to 8g per 100ml

- £2.59 per 10 litres of higher rate applied to drinks containing sugar equal to or greater than 8g per 100ml

Plastic Packaging Tax

In April 2022, the UK Government introduced the Plastic Packaging Tax (PPT) to encourage businesses to use recycled plastics in packaging manufactured in or imported into the UK. You need to register for PPT if:

- You are importing or manufacturing 10 tonnes or more of finished plastic packaging components in the next 30 days.

- You have imported and manufactured 10 tonnes or more of finished plastic packaging components in the last 12 months.

You need to pay the Plastic Packaging Tax if you have manufactured or imported plastic packaging components that contain less than 30% recycled plastic. The tax is charged on 1 April 2026 at a rate of £228.82 per tonne.

Excise Duties

Excise duty is an indirect tax on the manufacturing, sale or use of designated goods, such as those detrimental to health, e.g. tobacco and alcohol. The products on which excise duty can arise in the UK include:

- Wine and beer

- Cider and perry

- Spirits

- Imported composite goods containing alcohol

- Biofuels

- Hydrocarbon oil

- Climate Change Levy

- Tobacco products, etc.

Excise duty can arise on both UK-made goods and goods of non-UK origins. It occurs when goods are made available for consumption or goods imported for personal use are sold commercially.

Each product category is further divided into sub-categories. Each sub-category is assigned a different tax code, with different tax rates and resulting charges or liabilities.

Gambling & Betting Taxes

Remote Gaming Duty applies to gaming over the internet, by telephone, by television, or by any other electronic communication or technology facilitating communication. Providers are liable to pay Remote Gaming Duty at rates of 21% to 40% from 1 April 2026.

Similarly, gambling operators who offer remote betting are liable to pay General Betting Duty. From April 2027, the 25% remote rate applies to all remote betting, except bets on UK horse racing. Bets placed via self-service betting terminals on licensed betting locations is 15%.

Environmental / Green Taxes

Environmental or green taxes are imposed by the UK government to reduce negative environmental impacts by targeting activities, products or emissions considered harmful for the environment.

Climate Change Levy (CCL)

The Climate Change Levy is charged to reduce overall emissions produced by businesses in the UK. The CCL is charged for the energy businesses use. Some businesses are charged at the main rate and some at the Carbon Price Support rate. Energy suppliers are responsible for charging the correct levy.

The levy rate varies by commodity: kilowatt-hours (kWh) for gas and electricity, and kilograms for all other taxable commodities.

Landfill Tax

Landfill Tax is applied to the volume and weight of commercial waste deposited in landfills. The tax rates vary depending on the type of waste. Typically, a higher tax is applied to dangerous and low-quality waste. From 1 April 2026, the standard rate is £130.75 per tonne, and the lower rate is £8.65 per tonne.

This tax is paid by landfill owners and operators to the government or relevant authorities.

Vehicle Excise Duty (VED / road tax)

VED is a charge on every vehicle in the UK that uses public roads; it is collected to offset the detrimental effects of CO2 emissions from vehicles. This charge is one of the government’s significant revenue sources; its administration and collection are managed by the Driver and Vehicle Licensing Agency (DVLA).

VED during the first year of a car is proportional to its CO2 emissions, followed by a standard rate of £200 (April 2026) in the subsequent years, except for cars with zero emissions for which the standard rate is zero. Vehicles with a list price of £50,000 will attract a further £425 charge for the first five years.

Trade / Import-Export Taxes

These are the taxes levied on goods imported or exported, raising revenue, protecting domestic industries and regulating trade.

Customs Duties

Customs duty, also called import duty, is a tax charged by UK authorities on goods over £135 when crossing international borders. It is charged on imported goods, and the rate depends on the type, quality, value and country of origin. The duties typically range from 0% to 25%, depending on the value of goods.

Gifts from £135 to £630 are levied an import duty rate of 2.5% (lower for some goods). Gifts over £630 and other goods over £135 are charged based on their type, quality and country of export.

Import VAT

If goods are imported into the UK, you’ll be paying a standard VAT rate of 20%. For some goods, the rate will be 5%; for others, it will be 0%. Gifts below £39 are also VAT-exempt.

And some other goods, like food, etc., are exempt from VAT; they must be reported on your VAT returns.

Export VAT rules

To export goods from the UK, you don’t need to charge VAT. You can zero-rate the sale if you keep records and are compliant. When offering services in the UK, you are liable to charge and account for VAT. If you export to the EU from the UK, you don’t need to pay UK VAT.

If you offer services to a non-EU, you just need to include it on your VAT Return.

Local Authority Taxes

Taxes levied by local authorities to fund local services like social welfare, education and waste management. These are some of the common local authority taxes:

Council Tax

Local councils charge council tax to fund services for local communities. It is generally paid in 10 monthly instalments, followed by a 2-month non-payment period; in some countries, it can also be spread across 12 months for taxpayers’ ease.

The tax charge depends on three things, i.e. an individual’s circumstances, the valuation of one’s property, and the council’s needs. The services that the council funds with the council tax include:

- Provision and upkeep of the parks and sports facilities

- Police and fire brigade services

- Libraries and educational institutions

- Waste disposal and garbage collection

- Maintaining streets, i.e. cleanliness and lighting

- Maintaining records such as birth and marriage certificates, etc.

Special Levies / Community Charges

Special levies, or Special Expenses, are intended to ensure fairness for residents who don’t pay for services they didn’t receive. Special Levies are a portion of council tax by the district council for services offered in a particular area that are not provided anywhere else in the district.

The Community Infrastructure Levy is charged by local authorities on developers or landowners for new infrastructure. It is applied to developments creating 100+ sqm of space or new dwellings. Exemptions and reliefs are available for charitable development, social housing and self-build projects.

UK Tax Refunds and Reliefs

You might be able to apply for a tax refund if you have paid more tax than owed to the HMRC. This can be done online through the government website, following a step-by-step process that leads to the submission of an application. Generally, the refund application takes 4 to 6 weeks to process.

Conclusion

UK Taxes are a crucial source of income for the UK government and help to fund a number of welfare services and build the state’s resources. UK tax law is very intricate and requires deep insight and years of experience, as practice leads to perfection.

The number of taxes implemented, along with the bifurcation of individual taxes into various income tax bands and rates, underscores the importance of a qualified accountant overseeing the complex process and saving you money through the right tax relief claims.