When you start a limited company or similar entity, you’ll find out that corporation tax is one of the most important responsibilities as a company owner.

In this article, you’ll explore what corporation tax is, who pays it, how much it is, when to pay, how to file a corporation tax return and corporation tax reliefs and allowances.

This guide is designed to help you maximise your company’s profits and avoid potential HMRC penalties.

Before diving in, let’s begin with the definition of corporation tax.

What is Corporation Tax in the UK?

Corporation Tax is a tax on company profits, including trading profits, investment income and chargeable gains. A corporation is an entity with a separate legal identity from its business owners, who control it through the shares they own in the company. It includes the company’s profits and gains from the sale of assets (property, land, shares) that have appreciated in value.

What Profits are Subject to Corporation Tax?

Companies are liable to pay Corporation Tax on their taxable total profits (also called chargeable profits) in each accounting period. These are calculated by subtracting allowable deductions, expenses, and reliefs from income from various sources.

UK residents need to pay this tax on worldwide profits; non-residents pay only on UK-sourced profits. These are the main types of profits taxed:

Trading profits

It refers to income from core business activities, such as the sale of goods/services, minus allowable business expenses.

Investment income

Investment income can include interest, rental income and other non-trading income. Some dividends received by companies may be exempt depending on the circumstances.

Chargeable gains

Gain or profits made after selling assets like property, shares, or goodwill for more than cost or base value, after reliefs.

Who Pays Corporation Tax?

This tax is paid by companies on their profits if the business is a limited company, a foreign company with a UK office or branch, a club, a cooperative, or an unincorporated association (such as a sports club).

If your limited company makes taxable profits, it will usually need to pay Corporation Tax.

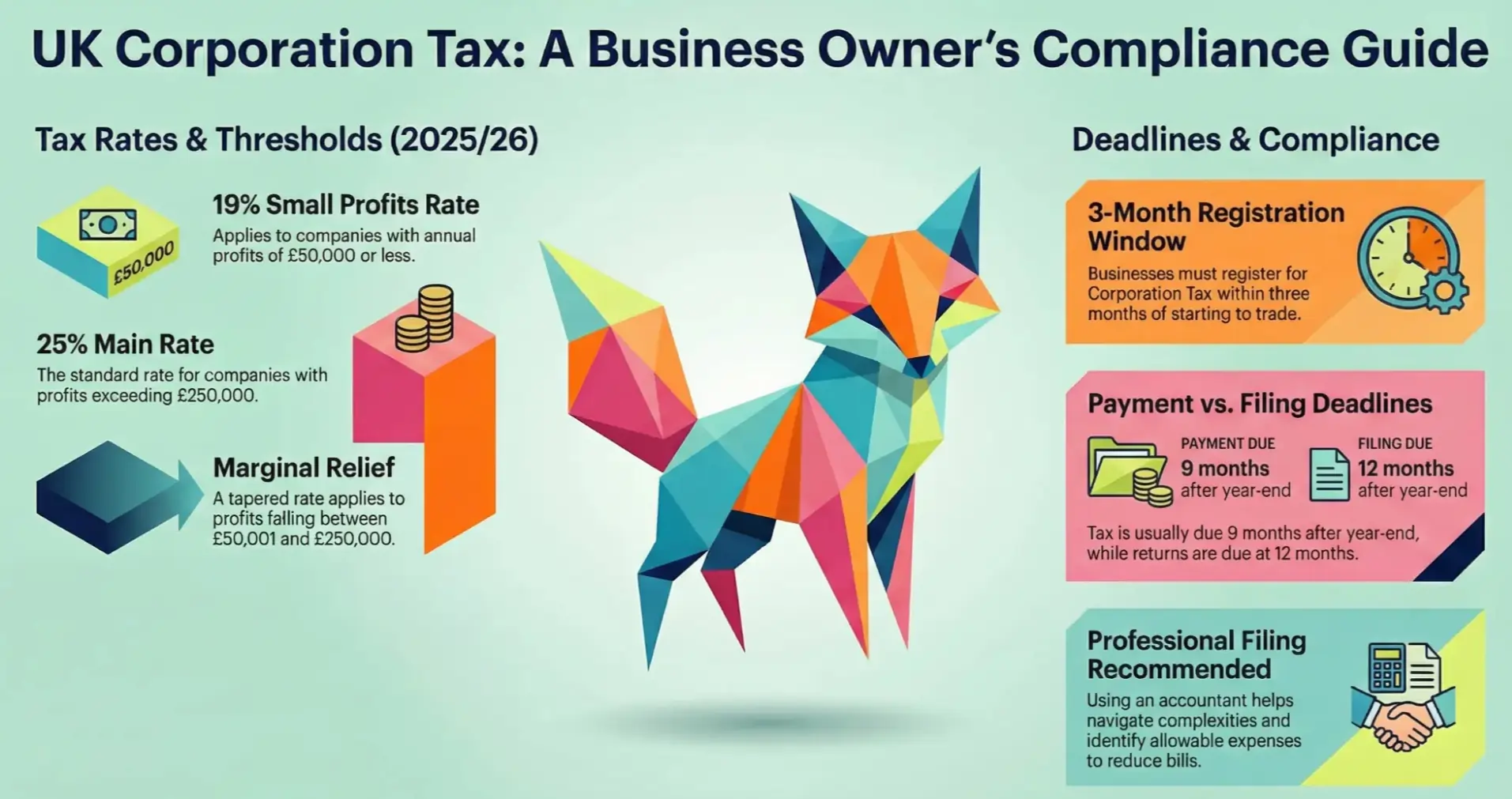

How Much is Corporation Tax?

At the moment, the main rate of corporation tax is 25% for profits over £250,000. A 19% small profits rate applies only to companies with profits of £50,000 or less. A tapered rate applies to the profits falling between £50,001 and £250,000.

| Threshold of Profit (2025/26) | Corporation Tax Rates 2025/26 |

| Up to £50,000 or below | 19% (Small Profits Rate) |

| £50,001 to £250,000 | 25% (Reduced by a Marginal Relief) |

| Over £250,000 | 25% (Main Rate) |

Corporation Tax Calculation Example

Let’s assume you’re a single company looking to calculate your corporation tax for a full 12-month accounting period. Taxable profits already take into account all allowable deductions, capital allowances, reliefs, etc.

Example 1: Small company

Taxable profits/income = £40,000

Since the amount is below the £50,000 threshold, a small profits rate applies.

Corporation tax rate: 19%.

Corporation Tax = £40,000 × 19% = £7,600

Example 2: Bigger company

Taxable profits/income = £300,000

When taxable profits are over £250,000, the full main rate applies. (Note: £50,000 and £250,000 thresholds are reduced if there are associated companies or the accounting period is shorter than 12 months.)

Corporation tax rate: 25%.

Corporation Tax = £300,000 × 25% = £75,000

Example 3: In the middle (marginal relief)

Taxable profits/income = £100,000

First, calculate tax at the main rate: £100,000 × 25% = £25,000

Then apply marginal relief: (3/200) × (£250,000 – £100,000) = (3/200) × £150,000 = £2,250

So Corporation Tax due = £25,000 – £2,250 = £22,750

The effective rate is roughly 22.75%.

Want to plan your corporation tax with an experienced accountant? Get tax planning services with us!

Do you pay Corporation Tax for your Business?

If your business is a limited company, you need to pay corporation tax on its gains from investments, trading, and the sale of assets. During the setup of a limited company, you can register for corporation tax.

How to Register for Corporation Tax?

While registering your limited company with Companies House, you’ll get the option to register for PAYE (as an employer) and Corporation Tax. You can also register for this tax separately using the GOV.UK website. The time limit to register for the tax is three months.

Once registered, HMRC will issue your Unique Taxpayer Reference (UTR), which is used for Corporation Tax filings and correspondence. It is also used for submitting corporation tax returns.

If your company is not carrying on business, it’ll be considered dormant for corporation tax purposes. Clubs, cooperatives or other unincorporated associations need to register for this tax differently.

If you are looking for an expert to handle your company accounts, tax returns, tax computations, and tax planning, get professional corporation tax services to maximise tax efficiency and keep your business fully compliant.

How to Pay Corporation Tax?

You can pay corporation tax using several methods. For fastest processing (same day or next day), use online or telephone banking, or an online bank account. Payment by Bacs, direct debit, or a corporate credit card typically takes up to three working days. In some cases, payments might take up to a week to clear, so be sure to allow enough time to meet the deadline.

Who Needs to File Corporation Tax Returns?

UK companies subject to corporation tax must file a company tax return if HMRC issues a notice to do so; dormant companies may have different obligations depending on HMRC’s requirements. It is best to seek professional expertise from accountants, as they are better equipped to handle the complexities involved in preparing company accounts and CT600 tax returns. Some people, however, prefer to make the calculations and submissions by themselves.

How to File Corporate Tax Returns

Here are some steps to file a corporation tax return:

- Register for HMRC online services to get Government Gateway credentials.

- Prepare your annual accounts and calculate your tax as per your profits.

- Use a filing software (easier to manage) or HMRC online service for CT600.

- Fill your company tax return (CT600) with details of income, gains, losses and reliefs.

- Submit the returns and keep an online receipt from HMRC as proof of submission.

If HMRC issues a notice to file a Company Tax Return (CT600), you must submit it even if your company makes a loss or has no tax to pay.

Corporation Tax Deadlines & Timelines

The corporation tax deadlines are specific to each company. These are the timelines for UK corporation tax in 2026 to remember:

Corporation Tax Registration Deadline

After incorporating your limited company, you must register for corporation tax within three months of starting your business. You can do it online via your Government Gateway.

Corporation Tax Payment Deadline

You need to pay any Corporation Tax due (or notify HMRC if not) within 9 months and 1 day after the end of the accounting period.

CT600 Deadline

You need to file your Company Tax Return (CT600 form) within 12 months after the end of the accounting period, including:

- Tax computations

- Full statutory accounts

- Any supplementary pages

Filing incorrect returns or failing to file the Corporation Tax returns on time usually attracts penalties from the government.

How to Reduce Corporation Tax?

Tax avoidance or evasion in the UK is not acceptable. There is tough legislation requiring all disputed taxes to be paid upfront. This will either leave you completely bankrupt or with a myriad of lawsuits that won’t put you in a better position.

However, you can reduce Corporation tax legally without breaking any laws. Here’s how:

- Claim every allowable business expense.

- Maximise capital allowance on assets

- Make employer pension contributions.

- Optimise the director’s salary and dividends.

- Claim R&D tax credits/relief.

- Use loss relief to offset profits.

- Keep on top of records and get advice early.

- Explore other reliefs, such as the Patent Box or charitable donations.

Corporation Tax Allowances for Businesses

You can claim allowable expenses to reduce your corporation tax bill. Allowable expenses are costs directly related to running a business that are essential. Here are some examples:

- Office costs

- Travel costs

- Clothing expenses

- Staff costs

- Premises/property costs

- Business insurance

- Legal & financial costs

- Marketing & advertising

- Other costs.

Corporation Tax Reliefs

You can claim corporation tax reliefs if you are a limited company or pay corporate tax. You can claim for:

- Marginal Relief (taxable profits between £50,000 and £250,000)

- Research and Development (R&D) Relief

- The Patent Box reliefs

- Overpayment relief

- Reliefs for creative industries (CITR)

- Relief on goodwill and other assets

- Disincorporation Relief

- Terminal, capital and property income losses

- Trading losses

Corporation Tax Penalties

If your company doesn’t meet HMRC’s deadlines and requirements for corporation tax, it may face penalties. The main reasons that attract penalties are:

- Not telling HMRC your company is liable for tax.

- Late filing of Company Tax Return

- Wrong or careless information on the return

- Not keeping proper records.

Penalties get much smaller (or are cancelled) if:

- You tell HMRC quickly yourself (unprompted disclosure)

- You help them fix it and give all the info.

- You had a reasonable excuse (e.g. serious illness)

- You took proper care but still made an honest mistake.

Late filing penalties are usually £100 immediately after the deadline, another £100 after 3 months, then additional tax-based penalties after 6 and 12 months.

The rate of corporation tax you pay depends on different cases:

- For a careless mistake, you pay up to 30%

- For a deliberate mistake, you are charged up to 70%

- For deliberate & concealed error, you are liable up to 100%

Late filing has fixed penalties that get larger the longer you delay. You can appeal any penalty you think is unfair.

Final Words

In conclusion, paying corporation tax on a company’s profits is one of the key responsibilities of limited company owners. Business owners can legally claim allowable expenses and reliefs to reduce their corporation tax bill. Clear House Accountants are specialist accountants available in London. Our in-house tax accountants can help you keep more of your money while submitting taxes correctly.

FAQs

How is corporation tax calculated?

This tax is calculated by applying 19%, 25% or a tapered effective rate via Marginal Relief to the taxable profit of your company.

Is an accountant necessary when filing corporate tax returns?

It is not required, but it is a good idea to use a chartered accountant or a chartered tax adviser when filing your returns.

Do you pay corporation tax on dividends?

No, dividends are not subject to corporation tax at the company level. This tax is based on the company’s profit before dividends are distributed.

Can you pay corporation tax in instalments?

Large companies (typically with profits over £1.5 million) must pay Corporation Tax in quarterly instalments under HMRC rules.

When does MTD for corporation tax start?

Making Tax Digital for Corporation Tax is not yet mandatory, and HMRC has not announced a start date.