Due to avoidance, non-payment, and fraud, tax loss has surged to £35bn in the UK. The pandemic has caused a severe budget deficit and financial restraint, leading many individuals and businesses to adopt tax avoidance schemes to reduce their tax liabilities. Tax avoidance can be a misleading term, and there is a fragile line between tax avoidance and tax evasion. A single and simple error can turn your tax-avoiding actions into tax evasion, leading to heavy penalisation. Therefore, Clear House Accountants have curated this guide to clear any confusion between tax avoidance and tax evasion by explaining the complexities of both.

Tax Avoidance

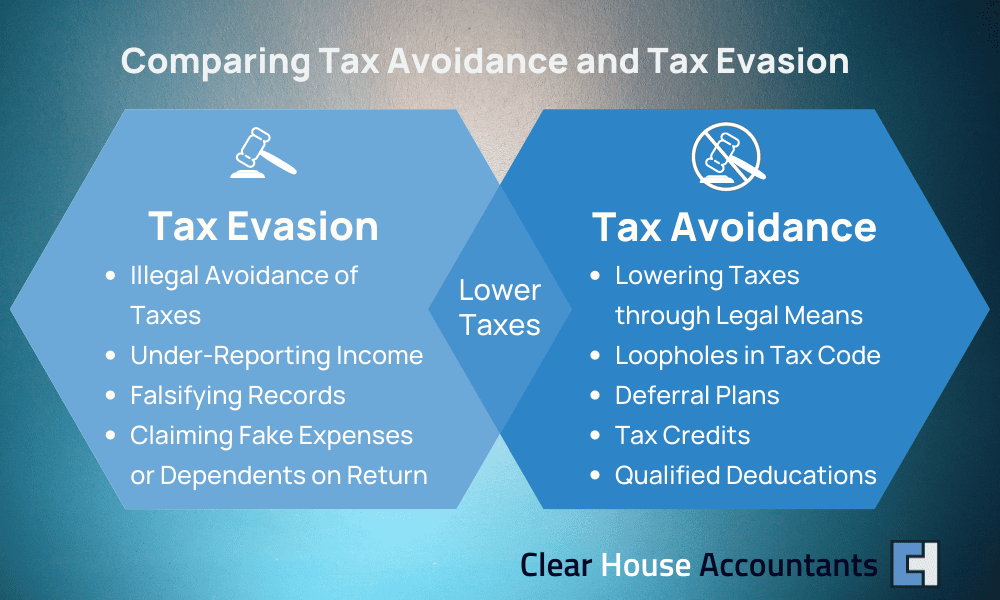

Tax Avoidance is the lawful use of rules to mitigate tax liabilities, leading to reduced tax payments. HMRC defines tax avoidance as “The moulding and contriving of rules according to one’s interest to avoid or mitigate tax liability.”

Tax avoidance promotes tax saving, and many corporates and legal professionals support the notion that tax avoidance is permitted to have an edge in tax penalties while assisting them in their quest for business growth. Most businesses opt for tax avoidance schemes to improve their cash flow while saving money on taxes.

The fake avoidance scheme promoters benefit from the vulnerabilities of individuals and companies, which leads to more tax liabilities and penalties. In most cases, companies may face heavy fines due to the inability to keep the right and timely records of business transactions, invoices, on-time return of taxes, and failure to list the new business. Therefore, it is important to consult expert tax accountants before opting for such schemes, as a professional accountant understands the consequences of not being compliant with tax liabilities.

The following are the indicators of avoidance schemes that individuals must not acquire if they’re looking for legal ways to avoid tax:

The Scheme Is Too Good To Be True

Taxation is complicated, though you may have ways to avoid corporation tax or personal tax returns. However, the avoidance schemes are designed so that they attract people by showing a considerable gain in return for little payment. Being offered a scheme where you are only suggested to pay the promoter’s fee and sign some papers, and are not asked for any further tax payments against profits, do not indulge in that scheme.

Loan Scheme

There are certain schemes only designed for small contractors, temporary workers, and agency workers where they are you’re paid a loan in some way or another through a trust or a company. The loan offered to contractors via a contractor tax avoidance scheme is sometimes referred to as a remuneration trust and contractors are not expected to pay it back.

The money might be channelled through a chain of firms, trusts, or partnerships located overseas and paid to a third party. The payment is sometimes given directly from an employer.

Some other ways to describe these payments are:

- Annuities

- Capital Payments

- Credit facilities

- Fiduciary receipts

- Grants

- Salary advances

- Shares and bonuses

In all cases, the payment that is not exerted to be paid back will be considered as income and will be tax liable.

Exploitative Benefits

Exploitative benefits are one of the prominent indicators of fake avoidance schemes. Scheme promoters attract their clients by showing them a way to generate considerable capital with reduced tax payments, with little to no risk involvement.

Money In Circle

Some fake tax avoidance schemes are fraudulent investment operations in which money is moved around in a circle or some other artificial arrangement in which transactions are made that have no apparent commercial purpose.

Misleading Claims

The plan is touted with false claims. These might include assertions like “Your take-home pay will be enhanced” or ” HMRC has endorsed or approved this program.” For example:

- ‘HMRC approved’

- ‘Retain more of your earnings after tax’

- ‘We ensure you get the highest take-home pay

- ‘Compliant tax-efficient pay’

These claims are certainly deceptive. HMRC does not endorse tax-avoidance schemes.

HMRC Has Assigned It A Scheme Reference Number (SRN)

If HMRC has found an arrangement to have the qualities of tax avoidance and is investigating it, you will be sent an SRN by your promoter. This should be included on your tax return if an arrangement has an SRN. Although having an SRN implies that HMRC has ‘approved’ the scheme, this is not the case. HMRC does not give approval for any tax avoidance plans.

It is worth noting that the absence of an SRN does not imply that the arrangement is not tax-saving and may still be reviewed.

Non-Compliant Umbrella Firms

Some umbrella firms comply with the tax regulations, while others offer tax-reducing strategies. These methods claim to be a “legitimate” or “tax-efficient” technique for retaining more of your money by lowering tax liability.

Video: 15 Ways To Reduce Corporation Tax

Few Tax Avoidance Schemes To Be Avoided

HMRC has published a list of tax avoidance schemes it is actively investigating. Even if a scheme isn’t mentioned, HMRC may still challenge it. The fake scheme promoters have introduced many tax avoidance schemes disguised so naturally that companies cannot differentiate whether they are legal or illegal. HMRC has legally fought against these schemes and prohibited their use. Anyone who adopts them will be charged with a penalty. Here are a few of the listed tax avoidance schemes.

Employee Bonus Schemes

Growth Securities Ownership Plan tax avoidance and similar schemes are designed to help employees avoid higher income tax by paying the difference on completion of the contract. At that time, the income is taxable at 28%, which is lower than the usual income tax rate.

Interest Relief Avoidance Schemes

Interest Relief Avoidance Schemes promise a considerable income to pay off the loan, either by delaying taxes or removing them. The scheme provides interest relief to the partners in trade.

Stamp Duty Land Tax (SDLT)

Stamp Duty Land Tax (SDLT) avoidance schemes promote the abusive transfer of rights under the rules.

The Employment Allowance Avoidance Scheme

The Employment Allowance Avoidance Scheme has underlying avoidance arrangements that benefit by exploiting the Employment Allowance. Through this scheme, employees can save their entire National Insurance Contributions (NIC) bill.

Employee Bonuses Tax Avoidance Scheme Involving Restricted Securities

Employee Bonuses Tax Avoidance Scheme Involving Restricted Securities provides the bonus in the form of an award share to avoid the tax and NIC bill.

VAT Contrived Schemes Used To Obtain Exemptions For Sporting Or Educational Training/Supplies

VAT Contrived Schemes Used To Obtain Exemptions For Sporting Or Educational Training/Supplies have covert arrangements that help the businesses to claim VAT by showing themselves as non-profit making bodies that provide sporting or educational supplies/training.

Business Premises Renovation Allowances Schemes

Business Premises Renovation Allowances Schemes exploit the Business Premises Renovation Allowances as investors can claim a 100% tax allowance on business renovation or set-up.

Gift Aid With No Natural Gift

Gift Aid With No Natural Gift assists the charities to claim repayment of tax on the donations given by the highest tax-paying donors.

Tax Avoidance General Anti-Abuse Rule (GAAR)

To counter tax avoidance, HMRC, in the Finance Act 2013, introduced the arrangement called the General Anti-Abuse Rule. The core objective of GAAR is to account for the individuals and companies that are liable for the use of abusive avoidance schemes. GAAR applies to the following taxes;

- Income Tax

- Capital Gains Tax (CGT)

- Inheritance Tax

- Corporation Tax

- Petroleum Revenue Tax

- Stamp Duty Land Tax

- Annual Tax on Enveloped Dwellings

- Any amount chargeable as if it were Corporation Tax (or treated as if it were

- Corporation Tax – such as a Controlled Foreign Company (CFC) charge –

- Bank Levy – Oil Supplementary Charge and Tonnage Tax)

Disclosure Of Tax Avoidance Schemes, DOTAS

Tax Avoidance scheme promoters conceal the avoidance schemes; therefore, HMRC requested the disclosure of the avoidance schemes. HMRC developed DOTAS, Disclosure of Tax Avoidance Schemes to evaluate and assess offensive tax avoidance schemes.

The DOTAS regime was created to allow HMRC to keep up with the newest types of tax avoidance techniques. HMRC has the option of requesting that promoters make a disclosure and, if necessary, alter legislation to prevent any plan that the government considers predatory and unjustifiable.

The DOTAS regulations have been expanded by the February 2016 changes, which might possibly cover more typical tax planning tactics.

A scheme promoter must disclose the main features of the plan to HMRC in accordance with DOTAS. Where disclosure is not made by a promoter, a scheme user must make it. The scheme will be registered with a DOTAS reference number (SRN).

Users of a scheme will be required to notify HMRC that they are using it by entering the DOTAS number in their tax return. HMRC will keep an eye on the scheme’s usage and, if necessary, pass legislation approving its termination.

Penalties, including fines, are imposed on those who fail to comply with the regulation. Notification must be made within 5 days of the arrangements first being made available if an obligation to disclose exists.

Penalty For Tax Avoidance

The Finance Act 2021 strengthens HMRC’s ability to penalise the promoters of tax avoidance schemes, including the off-shore promoters. All the individuals involved in the avoidance scheme and who benefited from it will be liable for a 100% fine.

The accountable must pay a security fee in advance of the penalised amount. HMRC will implement a freezing order on scheme promoters to restrain them from using their assets. Individuals caught using avoidance schemes prohibited by the HMRC have to pay back the taxes with a fine, and in some cases, they might have to go to jail depending on the legal prosecution by the HMRC.

Case Studies Of People Who Have Been Caught Up In Tax Avoidance Schemes:

Fraudsters who carried out a £100 million tax avoidance fraud have been sentenced to 27 years in prison

Four men have been handed prison terms for a fraud that tried to steal £100 million from the British public. The men said they had invested £275 million in film projects and used offshore companies to hide their tracks, but HMRC exposed it as a fraud.

The tax scam was devised by accountant Keith Hayley and London-based financial advisors Robert Bevan and Anthony Charles Savill, who presented it as a film production company named Little Wing Films. They claimed that investors would receive £130,000 in tax payments from HMRC for every £100,000 invested.

More than 275 investors – including football players, investment bankers, and pop stars put in more than £76 million under the impression that they were assisting the British film industry while lawfully reducing their tax burden.

Norman Leighton, an accountant and corporate services provider based in Monaco, assisted the three in constructing the ruse that more than £250 million was being spent on pre-production and production work, as well as film packages. The HMRC discovered, however, that these packages had cost only £4 million and were produced in the London offices of Little Wing Films.

The four individuals were sentenced to a combined 29 years in prison for cheating the Public Revenue after they were convicted of fraud at Birmingham Crown Court. HMRC will now begin attempting to recoup these repayments from the investors.

The Case Of Duncan, The IT Contractor – Abusive Avoidance Schemes

Duncan, 55 years old, started to work as a contractor. He contacted umbrella companies for the service of payroll. Duncan didn’t investigate much and signed the papers. He had no idea that these companies were luring him with tax avoidance schemes. Soon he was informed by HMRC about his non-payment of taxes.

Duncan was unable to reclaim the steep fees he paid to the umbrella firm, totalling £7,600. The umbrella company claimed that he had knowingly agreed to the terms and conditions of their payment plan and associated costs. Because the tax was late, Duncan also had to pay a penalty of just over £12,000 as well as interest.

Tax Evasion

Tax evasion is the deliberate non-payment of taxes that is illegal. HMRC defines Tax Evasion as ”Concealing of taxable income or the use of benefits to avoid the tax payment.” Tax evaders do not disclose their taxable assets, fake offshore accounts, hide the details of their income and conceal the financial reporting from HMRC.

Avoiding over £25,000 in tax is a criminal offence, and not only will you go to jail, but HMRC may “name and shame” you if you’ve evaded more than £25,000 in taxes. This can have an impact on the reputation of your business and sales as a result.

Tax evasion occurs when someone fails to disclose their taxable income or gains to the HMRC. Anyone who does not report their taxable income and gains to the HMRC may be charged with tax fraud. The HMRC must show that the taxpayer intentionally avoided or reduced their taxes in order for them to be convicted of tax evasion.

Tax Evasion Examples

The following are some actions done intentionally by the tax evaders to avoid paying taxes.

- The deliberate camouflage of trading revenues to avoid tax payments.

- Fail to report the VAT charged to consumers for the VAT-free imported goods.

- There are many expenditures that may be tax-free, such as spending on film production or an eco-forest. If the taxpayer redirects the money to other purposes rather than the stated goal, this is termed tax evasion.

- Cheating while submitting bills: This is especially prevalent in the construction sector and involves filing non-existent expenditures or personal expenditure claims for home improvements to avoid paying taxes.

- Making false claims about the shipment of imported goods or undervaluing imported products in order to avoid import taxes is a major evading of customs duty.

- Concealment of the transaction records from HMRC to avoid tax payments.

- Use fake accounts for transactions to evade tax on income and capital gains. If you believe your identity has been stolen, you may be subject to tax liability.

- Use of complex avoidance schemes that involve a complicated cycle of transactions for tax evasion purposes.

Tax Evasion Investigation By HMRC

For the quick and accurate tax gap analyses, HMRC opted for the wide-ranging analytical tool, ‘Connect’. It investigates the tax gap by evaluating data by incorporating different analytical tools and methods. The HMRC then uses it to assess tax evasion.

Tax evasion is an illegitimate non-payment of taxes and one of the leading causes of the tax gap in the UK. The Finance Act in 2013 demonstrated strict action against taxpayers, which showed non-compliance with the tax laws. The Criminal Finances Act 2017 also included businesses under the tax evasion liability. Tax evasion imposes a strict penalty that involves heavy financial fines and imprisonment. Both criminal and civil laws are used to prosecute tax evasion liability.

Tax Evasion Penalties

Tax evasion has the potential to result in significant fines and imprisonment, depending on the circumstances. Punishment and the typical tax evasion sentence can differ significantly. These are some of the penalties that may be imposed:

Income Tax Evasion Penalties

A summary conviction is punishable by a prison sentence of up to 6 months or a fine of up to £5,000. In the UK, income tax evasion may result in a maximum penalty of seven years in jail or an unlimited fine.

Evasion Of VAT

At the court’s discretion, a Magistrate may impose a penalty of up to 6 months in jail or a maximum fine of £20,000. The Crown Court can impose a sentence of up to seven years in prison or an unlimited fine.

Cheating Public Revenue

The maximum penalty for cheating public revenue in the UK is life imprisonment or an unlimited fine, owing to the serious nature of the crime.

Providing False Documentation To HMRC

HMRC tax evasion penalties may be as little as a fine of £20,000 or up to 6 months in jail under the Proceeds of Crime Act.

Evasion Of Duty (Smuggling)

A conviction for a summary offence can result in anything from a fine of £20,000 to seven years in prison. The maximum penalty for a felony charge in the High Court is an unlimited fine or up to seven years in jail.

Tax Compliance And Tax Planning To Avoid Tax Liabilities

Tax compliance and tax planning are the terms that sometimes get mixed with avoidance and evasion. But both tax compliance and planning are ways of minimising taxes without being accountable to HMRC.

Tax Planning

Tax planning is a legal way of using reliefs and claims for the tax payment to avoid taxes on businesses. It does not involve any abusive avoidance schemes. R&D Tax Relief or Capital investment relief are reliefs that businesses can claim legally to reduce their tax.

Tax Compliance

Tax compliance, on the other hand, is the accordance with the tax laws of the taxpayer. Taxpayers adhere to the reporting of taxable income and filing tax returns. The taxpayer complies with the rules demonstrated by HMRC to avoid any liability.

Conclusion:

Although taxes can be minimised through tax avoidance and tax evasion, the difference between these two deceptive terms is too narrow. The mistake has the potential to bring heavy fines to the taxpayer. So, to avoid unnecessary tax liabilities, consult qualified tax advisers and minimise your taxes the legal way.

Additional Resources