Most directors don’t take money out in just one way. The typical structure is a small salary plus dividends, then layering pensions or expenses depending on goals.

This means you can take money out of your limited company through director’s salary, dividends, director’s loans, business expenses, benefit-in-kinds, and workplace pension contributions.

In this article, we’ll explore the most common methods for withdrawing money from a limited company. We’ll also cover how to withdraw funds when closing a limited company and how to do so without incurring huge tax bills.

To help you choose the most tax-efficient method, we’ll also highlight the tax implications of each method with its pros and cons.

Let’s get started!

Methods to Take Money Out of a Limited Company

A limited company is a separate entity, meaning all the income it generates legally belongs to the company, not its directors and shareholders. Some of the legal ways to take money out of a limited company are through:

- Salaries

- Dividends

- Director’s loan

- Expenses

- Benefits-in-Kind

- Workplace Pension Contributions

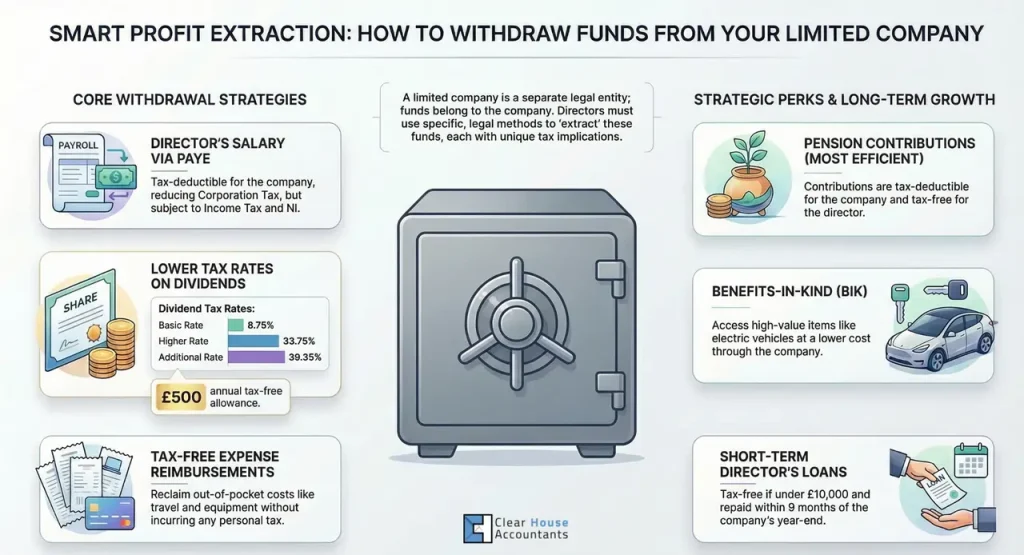

Take Money Out of a Limited Company by Paying Yourself a Director’s Salary

The most common method is paying directors a salary as employees via the PAYE system. Salary is a tax-deductible expense exempt from Corporation Tax. Directors pay income tax on their salary and, if it exceeds £5,000 (2025/26), the company pays 15% National Insurance.

Get in-depth information on Income tax and NI in this quick guide.

Advantages of taking money out of a limited company as a director’s salary

Here are some of the benefits of taking money as a director’s salary:

- The salary of a director is tax-deductible, reducing your company’s profit and corporation tax.

- Earning up to the national wage lets you receive monthly maternity benefits.

- When you earn up to £10,000 per year (and are eligible to be enrolled in a workplace pension scheme), your company will need to contribute to your pension pot, which is tax-deductible.

- By getting a salary, you can apply for mortgages and take out insurance.

- You can still receive a salary even when your company is not making significant profits.

Disadvantages of taking money out as a director’s salary

These are some of the major drawbacks of receiving a salary from the company as a director:

- Both you and your company may need to contribute to NICs.

- Income salaries are taxable and charged at a higher rate compared to dividend tax.

Explore the responsibilities of company directors and how they are paid:

Take Money Out of a Limited Company by Paying Dividends

When you are a shareholder of a company, you can take dividends to increase the amount of money you take out of a limited company. Dividends are taxed at a lower rate compared to salaries. Dividends can only be paid by the company when it earns enough profit.

How a limited company issues dividends

Dividends are issued by companies to shareholders as per the percentage of ownership or profit entitlement to their shares. The sole shareholder of a company with 100% ownership receives 100% of the profit.

Tax implications of taking money out of a limited company as dividends

Dividends are exempt from Income Tax and National Insurance up to a £500 yearly allowance. Tax above this depends on your income tax rate.

- 8.75% (basic rate)

- 33.75% (higher rate)

- 39.35% (additional rate)

If you want to learn how dividend tax works, read our guide.

Advantages of taking money out of a limited company as dividends

Here are the advantages of paying yourself dividends:

- They are charged at a lower tax rate.

- Unlike salaries, dividend receipts are not subject to salary tax.

- There’s no fixed time for issuing dividends, unlike the periodic payment of salaries.

- You can issue as many dividends as you would like, as per the dividend rule.

- You can seek funding and investment by issuing regular dividends.

Drawbacks of taking money out of a limited company as dividends

There are some drawbacks to withdrawing money through dividends:

- Dividends are paid from the company’s profit, and they are not tax-deductible like salaries.

- Dividends are only paid out where a majority vote agrees.

- These are not considered part of relevant UK earnings, so you can’t get relief even if the amount you’re allowed for pension schemes starts rising.

- There is a strict formal procedure to follow when issuing dividends, which adds extra administrative work.

Take Money Out of a Limited Company as a Director’s Loan

As a company director, money taken out as a loan must be recorded in a Director’s Loan Account and shown on the company balance sheet, tax returns, and your self-assessment. Loans over £10,000 must be reported to HMRC.

You can’t take money from the company, assuming it’s your own funds that you won’t repay.

Tax implications of taking money as a director’s loan

Loans above £10,000 not repaid within 9 months and 1 day after year-end face a 33.75% Corporation Tax charge under section 455.

If the director’s loan is within the limit of £10,000 and is repaid within nine months and one day of a company’s year-end, it will be tax-free and without any interest.

Benefits of taking money out of a limited company as a director’s loan

- You can get cash quickly and won’t have to pay taxes right away (no income, national insurance, etc., taxes at withdrawal).

- You can repay it anytime (as long as there’s no strict deadline to repay if overdrawn < £10,000).

- You won’t lose corporation tax relief (unlike salary/dividends, which lower your profit that’s taxable).

- You can avoid taxes and benefit-in-kind if you repay within 9 months and 1 day of the accounting period. This can be helpful for your company’s short-term cash needs.

- You won’t pay taxes and benefit-in-kind if you repay it within 9 months + 1 day of the end of the accounting period. This can be helpful for your company’s short-term cash needs.

Disadvantages of taking money out of a limited company as a director’s loan

- Section 455 tax: If, as at 9 months + 1 day after the end of the financial year, the loan has not been repaid, the company has to pay a temporary tax of 33.75% (which can be reclaimed when the loan is repaid).

- If a loan of £10,000 or more is interest-free, the director must pay Income Tax on the benefit received.

- The loan must be repaid, or it will be treated as a dividend/salary, triggering tax and National Insurance contributions.

- Large or repeated loans may result in an investigation or reclassification as a dividend/salary.

- Until loans are repaid, the company’s working capital is reduced.

Looking for more details on the Directors Loan Account? Don’t miss this post.

Take Money Out of a Limited Company as Expenses

Sometimes you have to pay your business expenses out of pocket. However, if you are spending money as business expenses, you can reclaim it from your company. To recover the money spent on the company’s expenses, you need to keep proper records of receipts and complete the claim forms.

These are the tax-deductible expenses which you can reclaim from your business:

- Working from home costs

- Mileage and parking charges

- Travel and accommodation

- General office expenses

- Professional services – e.g. accountancy fee

- Business insurance costs

- Computer and office equipment

- Mobile phones

- Training fees

A company can reimburse expenses when you get your monthly salary or at any other convenient interval. The company needs to save the receipts for all transactions over the last 6 years and record the expense refunds in its accounts.

Benefits of taking money out of a limited company as an expense

- You can get tax-free cash as a director.

- It helps the company deduct its corporation tax.

- No NIC for directors or companies to pay.

- Straightforward process for everyday business expenses.

Disadvantages of taking money out of a limited company via expense

- Heavy burden to keep records for business expenses.

- HMRC enquiries are common for high-frequency expense claims.

- Risk of reclassification as salary dividend plus penalties if corrected.

Reporting expenses and benefits to HMRC

- No P11D needed for reimbursements.

- Trivial benefits are tax-free without reporting.

- You need to report taxable benefits on a P11D or PSA, if applicable.

- Need to keep detailed records for HMRC inspection.

Tax implications of taking money out of a limited company by reimbursing expenses

Expenses incurred by a business or company are tax-free if genuinely business-related and properly documented; otherwise, they are treated as taxable salary (Income Tax + NICs) or as a dividend. The company can also benefit from corporation tax relief if it is allowable.

Take Money Out of a Limited Company via Benefits-in-Kinds

Along with the other methods of taking money out of a limited company, there are others. In a limited company, you can remunerate yourself as the director of the company by receiving benefits from the company. It is the legal way for your company to follow the benefits-in-kind (BIK) rules.

Benefits-in-kind may be subject to income tax and National Insurance. They are valued for offering substantial benefits at reduced cost to both employers and employees.

Advantages of using benefits-in-kind for taking money out of a limited company

- You can get tax efficiency on high-value items. Like, if you buy an electric car through BIK instead of buying it personally, it’ll cost you less.

- You can reduce the taxable profits by considering the full cost of the benefit as business expenses.

- There are certain benefits, such as the cycle-to-work scheme, that attract minimal Class 1A NICs for the company.

- By receiving valuable perks like insurance, phone, and office equipment without paying personal cash upfront

Disadvantages of benefits-in-kind for taking money out of a limited company

- Your company needs to pay Class 1A NICs (13.8%).

- Tracking, recording and determining the correct BIK value on P11D forms is a difficult process.

- If you are running a sole tradership, you have limited options for tax-free benefits.

- Higher taxes on petrol/diesel cars with high BIK rates (up to 37%) make them more expensive than personal purchases.

- Using company assets for personal use can trigger an investigation.

Tax implications of taking money out through benefits-in-kind

Benefits in kind can be tax-efficient for items such as EVs, pensions, and trivial benefits, but they must comply with strict rules to avoid unexpected tax bills or penalties. You need to always check the current HMRC and Gov.UK rules on expenses and benefits.

Take Money Out of a Limited Company via Workplace Pension Contributions

Company contributions to a workplace pension scheme are a highly efficient way to take money out of your limited company. Unlike salary or dividends, the workplace pension contributions are taken as tax-deductible business expenses. It reduces corporation tax and incurs no Income Tax or National Insurance for you or the company.

Advantages of taking money out via pension contributions

- Workplace pension contributions reduce corporation tax liability.

- Contributions are tax-free on entry, which means there’s no Income Tax or National Insurance.

- Companies also don’t need to pay Class 1 or Class 1A NICs.

- There are no salary restrictions. Companies can contribute to the annual allowance of £60,000 regardless of the director’s salary level.

- It is great for building long-term wealth and tax efficiency.

Disadvantages of taking money out via pension contributions

- Funds are locked until the minimum pension age, and you don’t get immediate access to cash.

- Annual allowance limit applies.

- For short-term needs, there is less flexibility. Not suitable for quick money.

- Needs to have a proper setup, a registered scheme with HMRC, and comply with auto-enrolment rules.

Tax implications of taking money out through pensions

It is one of the most tax-efficient ways to extract money from a limited company. This method is best, especially for higher-rate taxpayers or those planning for retirement. It is always recommended to get help from a personal tax accountant or financial advisor to ensure compliance and suitability.

Take Money Out of a Limited Company When Closing the Company

If your company has no use and you wish to close it by taking the money and assets, the right way to do so is via Members Voluntary Liquidation if the assets exceed £25,000. The first step is to settle any outstanding company debts.

If you qualify for Business Asset Disposal Relief, you may pay lower Capital Gains tax. Once the debts are cleared, assets can be distributed to shareholders.

Take Money Out of a Limited Company Without Huge Tax Bills

With the help of a qualified and professional accountant, you can get the right advice to take money out of your company as tax-efficiently as possible. Clear House Accountants has been helping business owners for over a decade.

Final Words

When withdrawing funds from a limited company, you should always prioritise tax efficiency and HMRC compliance. The best methods are through the director’s salary, dividends, expense reimbursement, pension contributions, and benefits in kind to minimise income tax, national insurance, and corporation tax while building long-term wealth. The right tax strategy depends on your personal tax position, profits and future goals.

It is always recommended to seek professional advice from our qualified accountant to avoid penalties and maximise your take-home pay.