Overview of Capital Allowances in the United Kingdom

When you spend money on something from which probable economic benefit will flow over the long term, you can claim these expenses against your taxable profit using capital allowances instead of claiming the cost directly. These expenses are also called capital expenditures. The process of identifying capital expenses can get complicated as there is no hard and fast rule; there are brief guides, toolkits, and resources available to help, but there are also other options which might help, such as hiring a tax accountant, chartered accountant, or accountant.

Capital allowances can be claimed on assets that are purchased for business purposes. These may include:

- Equipment

- Business vehicles (Cars, Trucks, etc)

- Machinery

A portion or all of the value of items can be subject to deductions from your profit before you pay your taxes.

What Can Capital Allowances Be Claimed On?

In its simplest form, you can claim allowances on capital assets purchased, which will generate probable economic value. If you have spent money on purchasing a capital asset and/or performing commercial property renovation, you can claim capital allowances. Generally, capital assets purchased in business are mostly plant and machinery; items not included in these are:

- Assets that you lease instead of owning

- Things such as buildings and parts of these buildings, such as doors, gates, etc

- Structural Items such as roads, docks, bridges, etc

- Capital items only used for entertainment,t such as Yachts or Pinball machines

Items considered as plant and machinery include:

- Items used in business

- Parts of business are considered fundamental

- Certain fixtures, e.g. kitchen

What is the procedure?

Capital allowances can be complicated, and with a large amount of complex data and resources out there, it is advisable for you to use our capital allowance accounting service,e which works as follows:

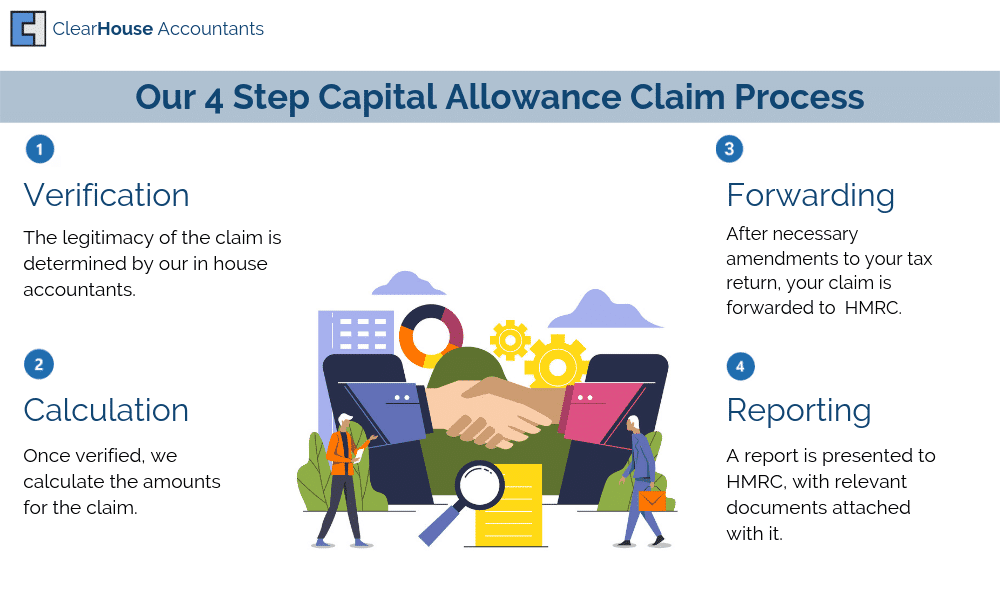

The process has to pass through 4 different stages:

Stage 1 (Verification):

The expert guidance provided by our in-house accountants helps in identifying whether our client has purchased an asset or spent money on improving a commercial property. It is very important to determine if the client can benefit from any capital allowance and how they are liable to benefit from it before the claim is forwarded for further processing.

As your trusted accountants, our primary responsibility is to guide and assist you to ensure that you are a compliant taxpayer, as further processing of the claim highly depends upon it.

After successfully passing through different stages of verification, the legitimacy of the claim will be declared by our tax accountants.

Stage 2 (Calculation):

The process of calculating the claim begins soon after the claim is declared legit. Our team of personal tax accountants will then take note of the asset or the integral parts of the asset and conduct a thorough assessment of each item.

Based on the assessment, our accountants will then differentiate between the items and the type of claims these items are eligible for. A sound approach is required to prepare a full and accurate claim; developing this approach requires the expertise of professionals from multiple disciplines, such as asset accountants, business accountants, and tax accountants.

The real challenge is estimating the method and type of allowances to claim, such as first-year allowance, annual investment allowance, written down allowance, etc., whilst ensuring that the conditions that apply to every claim that is submitted do not deviate from the legislation.

Stage 3 (Forwarding):

Before your claim is forwarded to HMRC through your tax return, your claim is attached to your tax profile, and amendments are made to your tax returns by our accounting firm. Our accountants then contact the HM Revenue & Customs to continue the process further.

Stage 4 (Reporting):

At the final stage, we will present a report to HM Revenue & Customs, which will outline the methods used to complete the calculations, with copies of amended tax returns (if any) attached. We will also include an invoice for the services you were provided by our accounting firm in the tax return.

However, you might be charged a certain percentage of your secured claim if the experts find it to be an unclaimed capital allowance. You might not find it troubling, as the refunded taxes are enough to pay the charges. If there aren’t enough, your claim will be processed back to the first stage, where re-verification will come into action.

Our accountants have taken and worked on almost every type of claim.

Can You Claim Capital Allowances if You Are Renting a Property?

To clear any misconception, claims can be made on rented property and not just on a property that is owned.

Important Amendments in the Clauses:

Legislation has introduced several changes in the clauses related to capital allowances in recent years. The following are the amendments:

- The special rate pool of plant and machinery on claiming writing down allowances has been reduced from 8% to 6%.

- Enhanced capital allowance (ECA) will be eradicated by 2020; this allowance could previously be claimed entirely through the first-year allowance on the plant and machinery, which is considered energy-efficient and environmentally friendly. It is expected that clients can claim for ECA till 2021.

- The first-year allowance on the capital purchased has increased from £200,000 to £100,0000 for two years, effective from January 2019. The Increase might be the result of the eradication of enhanced capital allowance (ECA) and the reduction in integral features allowance. To ensure a timely review of the property expenditures, the two-year time frame is enough.

- Structural Buildings allowance helps minimise the cost of constructing a new building for commercial purposes and is available to compensate for expenditures incurred after 29th October 2019. This allowance is also applicable for renovating existing structures, but is not applicable to integral features such as electrical or heating systems.

If you think you are in a position to claim any capital allowances, feel free to contact our expert in-house Tax accountants.

Clear House Accountants are expert Accountants. Our team of in-house tax accountants guides clients in identifying and claiming capital allowances based on the type of asset purchased and the client’s industry. Our tax accountants help businesses keep up with daily business activities by foreseeing the potential benefits that may result, whilst claiming capital allowances on the purchase of a particular type of asset, while helping improve cash flow and saving time and money.