A sole trader is the owner of their business and has control over the business’s assets and liabilities. As a sole trader, you might want to hire remote engineers, accountants, or marketers to save hiring costs or other expenses incurred on in-house employees. A sole trader does not have complexities like a limited company and is simple to run and manage. Sole traders enjoy freedom in making business decisions regarding how, where, or when they do anything for their business. He is not answerable or dependent on any shareholder or director.

Moreover, sole traders and their businesses are not different by their legal titles. If you are a self-employed person and run your own business, you are a sole trader. All the skilled people like plumbers, carpenters, hairdressers and other small business owners can be called sole traders. But not limited to it, small business owners, entrepreneurs, and self-employed trainers and consultants can also be called sole traders.

A sole trader business tells about your business structure, while self-employed means you work for yourself, not any other employer. Not every self-employed person can be a sole trader, but a sole trader is self-employed because a self-employed person can be in a partnership or limited company. So you are the sole trader when you are self-employed and the only owner of the business.

Sole traders can benefit from understanding how to start a business, manage deductible costs, and navigate self-employment registration efficiently.

How to Set up a Sole Trader Business?

If you are thinking of starting a business, a sole trader business is easy to start. Here are some steps to set up your own.

Do Research & Analyse

Before you jump into any business, you need to study the different types of businesses. You can start as a sole trader, a partnership or a registered as a limited company. But if you have decided to have your solely owned business, you need to analyse the different industries. It varies from food to outfit, tech to e-commerce and many others. It also depends on your interests and what is suitable for you. For newbies to enter the market, It is important to see that the choice of business has less competition and high chances of success.

Choose a Unique Name of Business

The next thing is choosing a name for your business. You can register it in your name or find a suitable business name that fits the industry. For sole trader business, it is not compulsory, but you use your business name and add your details, too. Because here business is not a separate identity. So you use your office or shop address, along with your own contact details and email.

- You must take care that it should be an original name meaning no other existing business should be in the same name.

- You can not use Ltd or a limited or limited company with the name.

- The trademark should also be unique and not resemble or copied from existing businesses. Doing so can create legal consequences for using the trademark copyrights.

Protect your business identity by learning How to Register a Trademark? All Questions Answered to avoid legal complications.

Register For Self-Assessment.

As a sole trader, your business income is your personal income and is not taken as a separate income in a business account. You pay income tax on the profits your business makes. To fulfil this purpose, you have to register for self-assessment with HMRC. HMRC uses this system to collect taxes.

Follow these steps and register as self-employed. Still, it depends whether you have sent a tax return before or not.

- Learn the process and forms needed for self-employment taxes with our Comprehensive Guide to Self-Assessment and Guide to HMRC Self-Assessment Forms.

Procedure to Set Yourself Up.

- You’ll have to register for self-assessment and Class 2 National Insurance using a business tax account. you can do it via a government-provided gateway user ID and password. you can create a new one if you have none.

- After registration, you will be sent a letter with your unique tax reference (UTR) which you use to file your tax return.

- You will also receive a follow-up email or letter reminding you to file your returns before their due.

- The online account keeps a record of your previous taxes and the due date for the next.

- If you have already filed your returns before, you will use the UTR (you got at the time of registration) to file a new tax return.

Keep Records of Income & Expenses

As a sole trader, you will have to keep records of all transactions, your income and expenses. You need to keep proof of all sales invoices, receipts and utility bills. So bookkeeping is required for running your business. Moreover, it also helps you make informed decisions.

Documents Required for Setting up a Sole Trader Business

You might need certain documents to operate your business as a sole trader. Based on the nature of your business, the number of documents and their types can vary. In a business, it is always recommended to settle things formally. Some of the documents you might need to create are discussed below.

Consultancy Agreement

As a self-employed, providing consultancy services irrespective of this as a main job or support job, you would be required to do it formally and put things in writing. You should close the deal with your client by signing a consultancy agreement. That would have all the contact information, services, prices, packages, duration of the deal, and limitations and scope of the services.

All the unexpected or unwanted things that can happen during service delivery should be mentioned in the agreement. So, if one party goes against the agreement, the other party can refer to the agreement rules and respond accordingly. The agreement protects the parties’ intellectual property and clarifies things between them. Moreover, it is also very beneficial when you are hiring someone else for consultancy services.

Office Sharing Agreement

Renting out an office is one of the key expenses you might incur when doing business. Businessmen try to reduce this cost by sharing office space. It can happen both ways, you can find a spare space in someone else’s office, or rent out your office spare space to another business. Sharing office space is normal and practised commonly as it benefits all the businesses party to it.

You can do it formally by signing a written office-sharing agreement. It should include all the information about the space granted to businesses to use, the duration of the sharing of the office space and limitations of the usable space, and most importantly the fees payable for the shared space.

Terms and Conditions of Business

It is essential to write terms and conditions for your business whenever you establish a business. It provides clarity about your products and services and the terms on which you are selling. Every business has its terms and conditions based on its nature and functionality.

As a sole trader, you should state terms and conditions for your business, including the rights, responsibilities, and roles of the proprietor and customers. You also ensure that all the terms and conditions comply with UK consumer laws. It provides clarity to avoid ambiguities about the exchange of the trade. It should protect customers’ rights from delays or incomplete services. Moreover, it is very useful to find a breach of contract. Terms and conditions also help minimise disputes when things go wrong, and the affected party is compensated accordingly.

Website Terms and Conditions

If you have any website, it should also have a separate page of terms and conditions. Terms should include all the information about the use of the website. It informs the users about the permitted use of the website i.e. like they can read, download and print. It protects website content by stopping visitors from using it for commercial purposes. Website owners can claim for use of their intellectual property or content copyrights.

Privacy Policy

Be careful when making a privacy policy that it should be according to the UK data privacy laws. If your website handles the user’s data i.e. names, addresses, and bank account details, it is advised to display a cookies policy. You should inform your visitors what kind of data is accessed and how it is used. It wins users’ confidence in using the website and makes them feel that their data is safe and protected.

Confidentiality Agreement

Sometimes businesses must share the business secret or sensitive information with other businesses. So to avoid the risk of leaking information and to preserve confidentiality, the business settles an agreement. In this kind of agreement, a business protects its confidential information by signing a legal contract and negotiating the deal without fear of leaking data. We call it a non-disclosure agreement in which parties can freely decide the terms. It allows the sole trader to easily protect its intellectual property or trade secrets.

Contract of Employment

Sole traders need workers to run the business. Thus, an employment contract signed between the employer and employee clearly states the parties’ roles and responsibilities. It declares the exchange of services with the wages to be paid and the relevant working rules. It covers the agreed work hours, allowed holidays, terms regarding the sick leaves, and procedure to end the employment contract. Moreover, it allows both parties to understand their duties and obligations.

Does a Sole Trader Need a Business Bank Account

It is not legally compulsory to have a business account for you as a sole trader. But it is recommended to have a business account. You can use your bank account for both your personal and business purposes. You can also have a separate dedicated personal account for it. Here are some of the reasons you should open a business account.

- Some banks restrict you to use your account for only personal use. So if a bank notices a lot of money being circulated through your account, it may ask you to open a business account for business use. Thus it is suggested that you have a business account.

- Having a business account allows you to differentiate personal expenses from business ones. Having a clear history of purchases, sales, and expenses makes it easier for you to deduct your allowable expenses from returns to calculate taxable profit. It makes it easier for you to submit your tax returns with HMRC.

- It does not include your personal finances and will help you make an informed decision regarding your business. It helps you have a clear direction of your business finances, assets and expenses and not mix it with your personal ones.

- When applying for a business loan it is required to have a business account. It builds your credit history, and based on that, you can get business finance in future, too.

- It wins people’s hearts and minds when things are practised professionally. Having a dedicated business account for your business makes it look professional and allows people to send or receive payments via a business account rather than your personal account. Some even avoid purchasing or don’t feel confident sending money to a personal account.

Moreover, it allows you to borrow money in the name of your business, have a business credit card and handle payments from customers. A business account offers greater facility and thus has separate charges for its operation.

Explore the Best Business Bank Accounts to find the right solution for managing your sole trader finances efficiently.

Does Sole Trader Need Business Insurance?

Working as a sole trader would require you to have certain business insurance. It protects your investments in adverse situations and provides you with peace of mind. People take insurance for the smooth run of their business, and if anything goes wrong, insurance will save them from the loss. No doubt, buying insurance is significant for the financial safety of the business, but buying the correct type of insurance is itself very important.

The type of insurance you should buy depends upon the nature of the business, business assets, turnover, employees, and the business’s location. Let us discover some of the business insurance types for a sole trader.

- What Business Insurance do I Need for My Business? to safeguard your sole trader operations from unforeseen risks.

Public Liability Insurance

It is one of the most commonly bought insurance which takes your responsibility to a third party. It can protect you from the claim made against you or your business by third parties for the loss to them or their property.

Professional Indemnity Insurance

This type of insurance covers the legal fees and compensation for the claims against you by the client or third party for having a loss due to a mistake or inadequate advice or service. It does not cover the bad workmanship and reputational loss made to the party. It is mostly required for businesses providing architectural design services or consultancy.

Product Liability Insurance

If you are dealing with the manufacturing, installation or supply of the products, you must have this kind of insurance. Customers can claim the loss, damage or injury caused due to the product, or they can sue you for it. So, product liability insurance protects you from liability for the loss made due to your product. It is mostly taken by the businesses dealing with or handling the products.

Cyber and Data Insurance

Any business dealing with customer data and storing it on the cloud needs cyber insurance. If you are dealing with the customer’s data or have an online business setup, this data can be exposed to hackers or cyber-attacks. Thus, any loss or data breach can be covered by cyber insurance.

Portable Equipment Insurance

It covers the loss made to the portable equipment of the business. It can include laptops, printers, cameras, or other electronic equipment. It repairs or replaces the equipment exposed to damage or loss. This kind of insurance is beneficial when there are chances of theft, breakage or other unwanted event causing damage to the equipment.

What Expenses can be claimed back as a Sole Trader?

A sole trader pays tax on their taxable earnings via self-assessment. As a sole trader, there are some expenses that you can claim as allowable expenses and can be deducted from returns to calculate taxable income. This way you avoid paying more by claiming expenses.

The idea behind it is that HMRC does not want to tax the money you need for regular business operations. Here is the list of expenses discussed below which you can claim as deductible expenses.

- Office Supplies

These supplies include office stationery, ink, phone and internet facility, software used for business operations (subscription-based) and postages.

- Office Equipment

You can claim computer hardware, printers, scanners and software (if used for more than two years) as expenses for business equipment. It is only doable if you are using cash basis accounting, otherwise, for traditional accounting, you can claim capital allowances on these.

- Business Premises

Expenses to business buildings that can be deducted include building rent, utilities, building insurance, maintenance, and security costs. While it should be clear that buying a building can not be claimed as an expense.

- Transport

A sole trader can claim transport expenses if it is done for business purposes. It should be clear that your commute from your residence to your office does not qualify for deductible transport expenses.

- Legal and Professional Costs

Hiring services of professionals such as an accountant, surveyor, consultant or legal advisor for business purposes can be taken as deductible expenses.

- Raw Materials

You can also claim the cost associated with buying raw materials because it is taken as a direct material cost.

- Professional Insurance

It includes public liability insurance, professional indemnity insurance, and travel insurance and can be claimed as professional insurance.

- Clothing

Some jobs require you to wear special clothing i.e. costumes or uniforms, and it falls into tax-deductible.

- Marketing and Trade Subscriptions

Marketing and promotional costs pile up to a big expense. It can also be counted as a deductible expense. Moreover, costs associated with membership in professional organisations or trade bodies are also tax-deductible.

- Household Expenses

As a sole trader, if you are head of the family and responsible to pay all household expenses and bills, you can enjoy some deductions or lower taxes. But if you are self-employed and working from home partially or completely. You can have some relaxation in taxes or enjoy deductions as you are using part of your house as an office. Following household expenses are tax deductible and deducted according to their percentage of use for business.

- Mortgage interest expense is a type of household expense. Thus mortgage interest periodic payments are tax deductible.

- Rent can also be deducted if it is rented out to by a lender for the only portion of the building that is utilized by the business.

- Council Tax is also tax deductible.

- Property repairs to the portion of the building that is used for business purposes.

- Utilities: Water, electricity and heating or other utilities can be deducted for the portion that is used for the business.

Can Sole Traders Hire Employees?

Yes, sole traders can be employers and can hire other working staff or employees. It is unnecessary to set up a limited company to hire other workers for your business. A sole trader solely owns a business and is authoritative to hire or fire people. It can be seen that sole traders keep support staff to run the business. A sole trader business does not mean that the owner has to be the only individual contributing to business operations.

You might be thinking about whether a sole trader is an employee of its business, and the answer is no. Because the owner is self-employed and has no contract with the business. In a limited company structure, the directors can be employees of their own business and need to sign employment contracts because a business is considered a separate legal entity.

- Understand the essentials of hiring staff with Sole Traders Employing People – Employ People As A Sole Trader!

Personal Liabilities for Sole Traders

Liability is the total amount a business owes to another person or entity. It is the responsibility of business or business owners to pay these debts. Owners in a sole trader business, where a business and owner are not separate entities, are personally responsible for paying debts to debtors if the business fails to pay. The liability of a sole trader is not limited to business but it might require the trader to sell his or her personal assets to pay back the liability. Thus in this kind of business setup, you incur unlimited liability.

Tax Payable as Sole Trader

Before you step into the sole trader business, it is important to understand all the tax rules and obligations.

If you are earning more than £12,570, you have to pay tax for a sole trader. The personal allowance of the tax year is £12,570, which means you will only be taxed if you are earning more than this amount. However, it is a necessary obligation to complete a self-assessment tax return irrespective of whether you pay tax or not.

Here are the Tax Bands Discussed Below.

- 20% is the basic rate tax band applicable when you earn £12,571- £50,270.

- 40% is the upper rate tax band and applicable if your earnings range from £50,271 – £150,000

- A 45% upper rate tax band is applied when your income exceeds £150,000.

National Insurance Contributions

We already discussed how to register for self-assessment, and to inform HMRC to make sure you are paying tax each year. Likely, you also need to pay national insurance for which you need to apply for a national insurance number.

You pay national insurance through the self-assessment form discussed above. There are two categories of insurance, you will have to pay based on the category you fall in.

- If your profits exceed £6,725, you will have to pay Class 2 National Insurance.

- If your profits exceed the £9,880 Lower profits limit for Class 4 NICs to the Upper profits limit for Class 4 NICs which is £50,270 a year, you will have to pay Class 4 National Insurance.

VAT Registration

As a sole trader, you might need to register for Value-Added-Tax. You only need to register if your turnover is more than £85,000 which is the threshold. If you have registered for VAT, you can charge VAT to all your customers and claim back on all purchases.

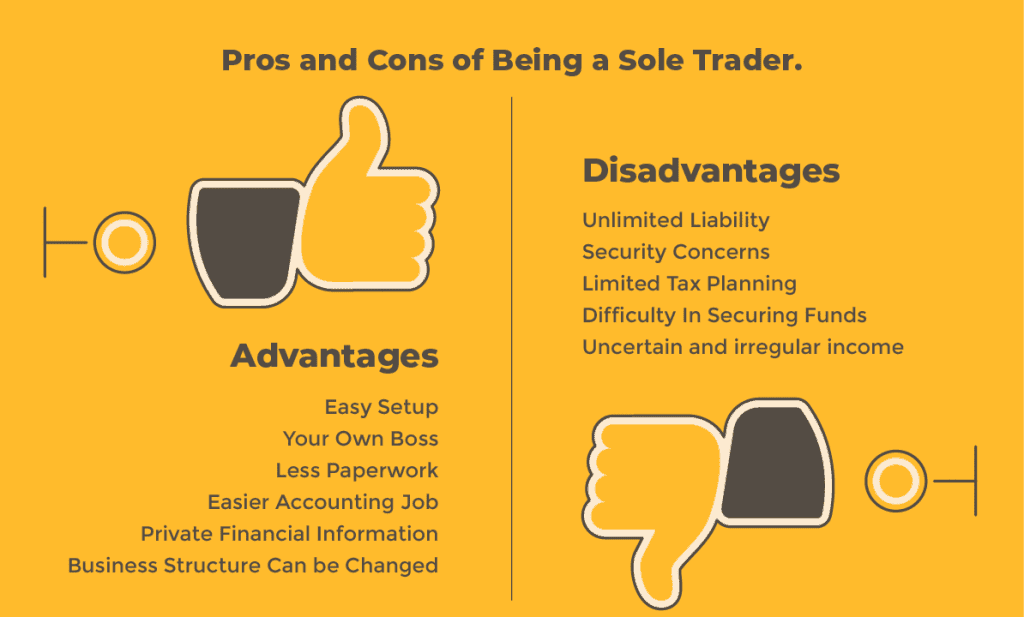

Pros & Cons of Being a Sole Trader

There are different advantages and disadvantages of any business based on its type, and structure. Here we talk about some of the common pros and cons of the sole trader business, you should consider before starting any self-employed business.

Advantages

- You are the only boss and decision-maker of your business. You have full control over your business assets and are free to use them the way you want to. You do not need approvals from any board, or partners in share.

- Less paperwork is involved in the sole trade business. You just need to keep a record of your business transactions which are required at the time of submitting returns.

- In this form of business, you keep your records, partners, and annual returns private. Whilst in the company form of business, you must provide this information to Companies House, which is then accessible to everyone when published.

- It can also prove your self-employment to help you provide your child with tax-free healthcare.

Disadvantages

- A sole trader business has unlimited liability, and the owner is responsible for all kinds of debts and losses. Here, you and your business are taken as single entities, not separate ones.

- Much attractive factor for setting up a limited company, a sole trader business is less tax efficient. The personal income tax rates vary from 20% to 45% for sole traders while corporate tax for limited companies is 19%. The company structure allows you to enjoy a potential reduction in national insurance contribution, shareholder tax allowance and sometimes special tax evasions by the government.

- Limited companies have made their records, statements and list of directors public, attracting more money from shareholders and creditors. Lenders feel more confident when financing it.

- Being personally employed as a sole trader would require you to give more hours to your business. Because you would be self-responsible for all the activities of the business. Also to avoid extra costs, you would try to do things by yourself rather than hiring an employee for it, which increases the burden.

Switching From Sole Trader to a Limited Company

Setting up a new business as a sole trader is a good start, however, if your annual income and profits increase, it is good to switch to a limited company. It will lower your taxes, provide limited liability and offer greater borrowing power. Not only this but will enhance your business credibility in the market.

If you are interested in converting your business from a sole trader to a limited company, here is the list of actionable steps you need to take.

Register Your Business as a Limited Company

Registration of your business is the first step as a limited liability company. It is an online process and can be easily done through an agent. You will need to register a unique company name, the company address, atleast a director and a shareholder each with his or her address and Standard Industrial Classification (SIC) code describing the nature of your business.

Inform HMRC About Business Conversion

When you have finally set your business as a limited company, you need to inform HMRC that you are no longer self-employed. HMRC will stop taking your business as a sole trader. HMRC allows you to do it through an online form. You will be required to send the following details to the HMRC.

- The date on which you stopped working as self-employed

- Unique Taxpayer Reference

- National Insurance Number

- Your Name

- Date of birth

- Address

- Nature of the business

Moreover, you need to send final self-assessment tax returns as a sole trader that include your earnings and tax liabilities as self-employed. You will also need to add allowable expenses, capital allowances and capital gains tax on any sole trade assets converted to the company.

Transfer Your Sole Trader Assets

When you have finally closed your sole trader business, you would then transfer some assets, such as machinery and equipment, to your company. Transferring assets to the company can be done in a way that you get payment from the company in exchange for these assets. Or create a director’s loan account and the company pays for the transferred assets over time. Transferring some assets may result in CGT liability, but it can also be reduced by claiming tax relief like Incorporation Relief, Business Asset Disposal Relief or ‘Hold-over’ Relief.

Create a Business Bank Account for the Company

Although it is not a legal requirement for a company to have business bank accounts. But it is commonly advised to have a business account in the company’s name to keep business finances separate from personal finances and look professional.

Public Announcement

Regardless of whether you continue business with the same name or a new one, you will have to notify all the stakeholders that you have switched your business from a sole trader to a limited company. Stakeholders include your creditors, banks, debtors, employees, suppliers and clients. It is necessary to announce because the change in business structure will bring a new set of terms and conditions and legalities.

Tax Liabilities as a Limited Company

Once your business is registered as a company, the Companies House informs HMRC about it. HMRC then sends you a letter describing the tax obligations and containing a 10-digit unique taxpayer reference. You also need to register your company for corporate tax within 3 months of set-up. Moreover, if your turnover exceeds £85,000, you need to register the company for VAT too.

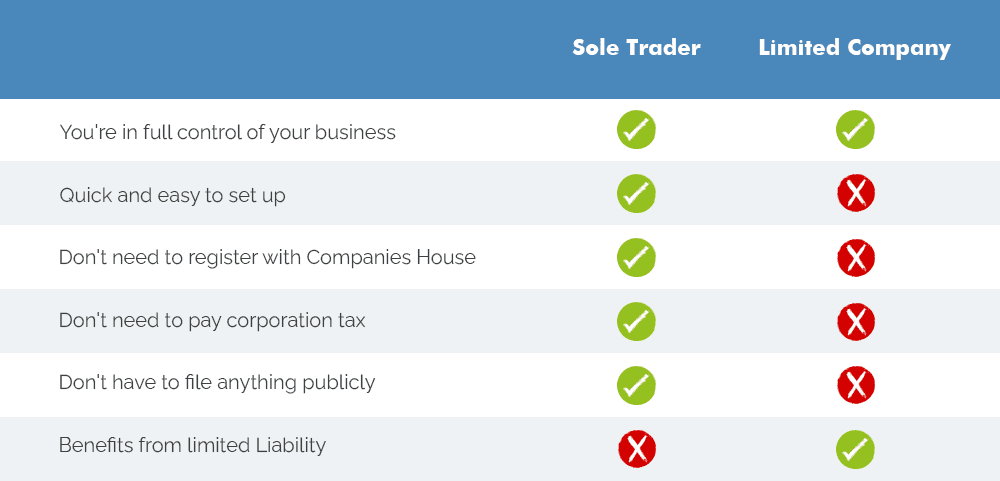

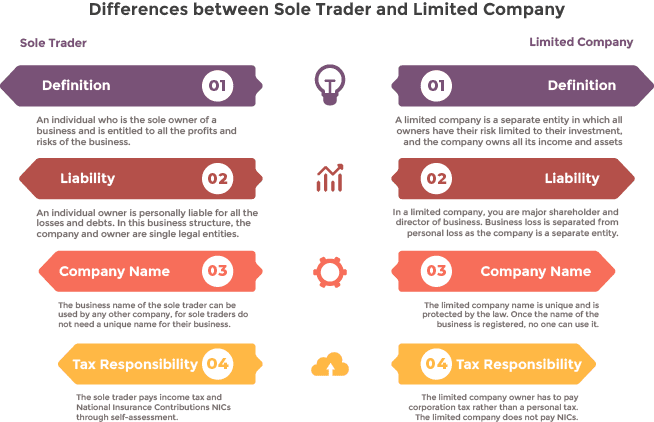

Sole Traders vs Limited Company

Are you confused to start as a sole trader or a limited company? The choice depends on your circumstances and lifestyle. Here we compare these two different business structures making it easy for you to decide and choose from.

Registration

As a sole trader, you can set up by registering for self-assessment with HMRC. While in the company form of business, business is registered with Companies House.

Liability

A sole trader is personally responsible for the loans of the business, while his stake is only limited to the amount invested in the company. As a sole trader, your personal finances are also at risk in case of insolvency.

Management

A sole trader business is easy to run and has a lesser burden on the employer. While a company is very time-consuming and hectic to operate for its increased scope, complex structure and additional responsibilities.

Documents and Paperwork

There is a lot of paperwork involved in a limited company every year. While in the sole trader business you only need a self-assessment document annually.

Information Access to the Public

As a sole trader, you can keep the business records, partner details and financial statements private. While as a limited company, your data and records are displayed on the Companies House Website public to all.

Director’s Fiduciary Responsibilities

You don’t have any director’s fiduciary responsibilities as a self-employed sole trader. Whilst you own additional legal responsibilities as a director in a company called Director’s Fiduciary Responsibilities.

Taxes

Despite having many complications, a limited company is more tax-efficient. The personal income tax can be 20 – 45% as a sole trader while corporate tax is fixed at 19%. Also, in the company form of a business, you can reduce it by claiming certain allowances and deductions such as shareholder tax allowance.

Access to the Profits

As a sole trader, you can take the profits out of the business whenever you want. Contrary to it, it is very complicated in the limited company and requires you to have a director’s meeting to distribute the dividends.

Conclusion

We hope you got enough information about setting up a sole trader business, its liabilities, tax implications and insurance types. We discussed the documents you would need, payable taxes and the pros and cons of sole trader business. A comparison of a sole trader business and a limited company has also been made so you get to know about the alternative, too. Since we have provided enough information about it, it is now up to you to start as a sole trader or limited company.

Additional Resources