The UK has maintained its position as Europe’s leading tech ecosystem over the last few years, with its technology sector rapidly flourishing. Over 60% of tech businesses consider the UK an attractive hub for tech growth compared to other key markets. Accordingly, there is fierce competition to attract top talent and qualified staff in order to remain competitive. To this end, the tech founders and directors utilise share incentive schemes for employees to retain staff and reward their loyalty in the long term. This blog lists HMRC’s top tax-advantaged share incentive schemes and also discusses flexible, non-tax-advantaged share schemes.

Tax-Advantaged Employee Share Schemes (TASS)

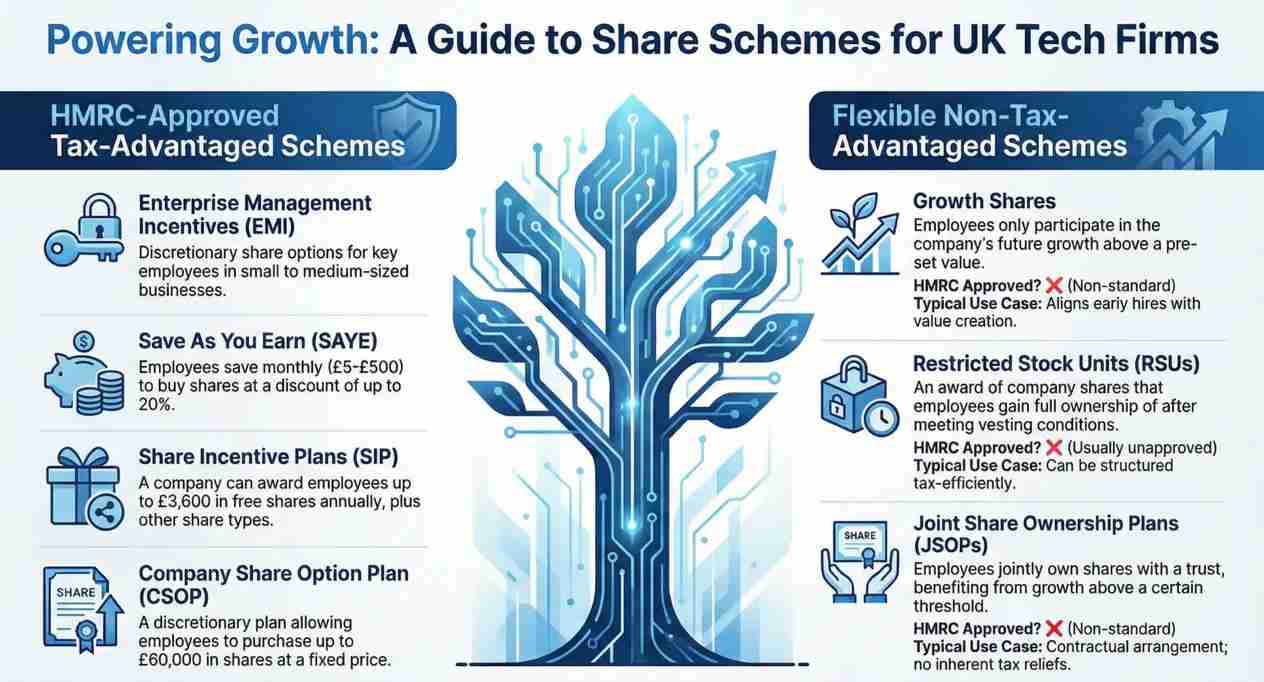

HMRC offers four tax-advantaged employee share schemes (TASS), also known as approved share schemes. These schemes generally differ in their targeting, but they are all widely designed to promote employee share ownership in the business by offering generous tax treatment. Moreover, with these schemes, the tech companies encourage their employees’ hard work by providing them with a direct stake in the company so they can also share in the company’s success. It is worth noting that of the four HMRC employee incentive schemes, two are discretionary (CSOP and EMI), and two are non-discretionary tax-advantaged employee share schemes (SIP and SAYE).

Enterprise Management Incentives (EMI)

An EMI is a discretionary share incentive plan designed to help small- and medium-sized businesses retain and reward key employees. Under EMI schemes, companies can grant share options to qualifying employees up to a specified limit. Notably, a share option is not a share itself, but a right to buy shares in the company. The employee exercises this right at a future date. These share options are typically offered at a fixed, discounted price to provide employees with a valuable incentive.

EMI has several crucial aspects, including its working, setting up requirements, eligibility criteria for businesses, advantages for employers and employees.

Tax Advantages of the EMI scheme

With an EMI share scheme, employees usually do not have to pay Income Tax or National Insurance when they buy their shares, as long as they pay at least the market value set at the time the option was first granted. However, if an employee was offered shares at a discount to their market value, they might need to pay Income Tax or National Insurance on the difference. Notably, this difference is based on what they pay and what the shares were originally worth. More importantly, if they purchase the shares within 10 years of when the option was granted, no Income Tax or National Insurance is due on that difference.

Save As You Earn (SAYE) Share Scheme

A SAYE scheme, also referred to as ShareSave, enables eligible employees to link their savings to a share purchase option. It is also an “all-employee” scheme. An employee secures the legal right (an option) to buy shares in the company with their savings at a fixed price. Importantly, the scheme requires employees to make fixed regular monthly contributions (between £5 and £500) from their post-tax (net) salary over three or five years.

At the end of their savings period/contract, they can use their savings to buy shares in their company at a set price. Notably, this price was discounted by up to 20% from the market price when the option was granted. An employee can save up to £500 a month under the SAYE scheme.

Benefits of SAYE for Employers and Employees

For employers, SAYE schemes attract and retain top talent, especially when high salaries aren’t feasible. Offering discounted shares fosters employee ownership, loyalty, and job satisfaction. This increased productivity leads to better innovation and profitability for the company.

Share Incentive Plans (SIPs)

The highly tax-efficient SIP, launched in 2000, allows immediate share purchase and lets employees save and buy shares regularly. Crucially, unlike SAYE, CSOP, and EMI, which grant options to buy future shares, the non-discretionary (all-employee) SIP awards shares directly. Therefore, the company must offer it to all eligible employees on similar terms via a dedicated trust, using four combinable parts. It is noteworthy that a SIP requires the establishment of a UK-resident trust, managed by a trustee, to hold the shares on behalf of employees and ensure statutory compliance. The SIP enables employees to acquire shares in their company at a discounted price through free shares, partnership shares, matching shares or dividend shares.

Free Shares

Employers can grant employees up to £3,600 in free shares annually, giving them a direct stake in the company. These shares may be linked to individual or team performance, but clear, pre-set targets must be communicated beforehand

Partnership Shares

Employees can use pre-tax (gross) pay to buy partnership shares, providing immediate tax and NICs savings. The annual limit is the lower of £1,800 or 10% of their total salary. Income Tax and NICs are not applied to the gross salary used for the purchase.

Matching Shares

To boost engagement and motivation for long-term tech goals, employers might offer a direct equity interest. This could involve matching each purchased partnership share with up to two free shares. Employees must check their employer’s plan documentation to confirm if they offer any.

Dividend Shares

Shareholders in a SIP trust receive dividends. They may reinvest dividends from free, partnership, or matching shares to purchase additional dividend shares within the plan, with no investment cap. Reinvested dividends are exempt from income tax if kept in the plan for at least three years. Otherwise, dividends are taxed normally, requiring higher-rate taxpayers to report them on their Self Assessment tax return.

Tax advantages of SIPs

When an employee obtains shares through SIP and keeps them in the SIP trust for five years, the shares remain completely exempt from any Income Tax or National Insurance on their value. Similarly, there is no Capital Gains Tax due on shares sold, provided they were held in the plan until the point of sale, transferred to an ISA within 90 days of withdrawal, or transferred to a pension, directly from the scheme when it ends.

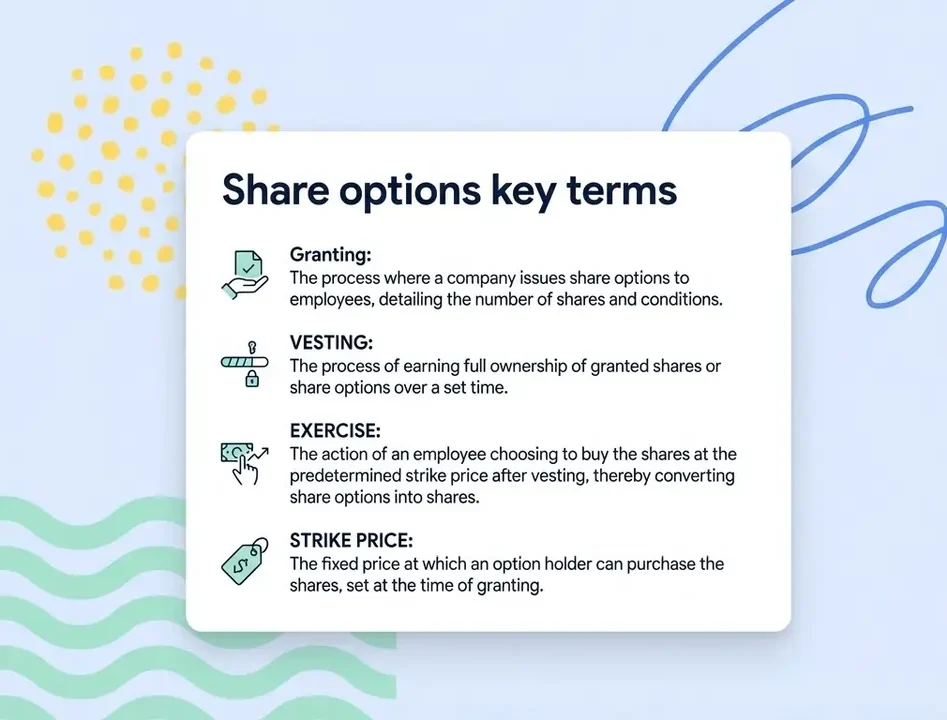

As all employee incentive schemes UK involve granting share ownership, it is significant to understand the key terms associated with share options.

Company Share Option Plan (CSOP)

A Company Share Option Plan (CSOP) is another tax-efficient, discretionary employee share incentive scheme for UK tech firms, motivating employees and full-time directors. Recipients can purchase up to £60,000 in shares (since 6 April 2023) at a fixed option price set initially, based on market value. If the company performs well, employees profit by buying at the lower original price, aligning their interests with the company’s mutual goals.

Unlike Enterprise Management Incentive (EMI) schemes, Company Share Option Plans (CSOPs) do not have limits on company size (employee count or assets) or business type. The two schemes also differ in taxation and qualifying criteria.

Tax Advantages of CSOPs

Employees buying shares 3 to 10 years after the option grant avoid Income Tax and NI on the difference between the market value and the purchase price.

Non-Tax advantaged Share Schemes (Unapproved Share Schemes)

Unapproved Share Schemes are non-tax-advantaged because they lack HMRC approval for tax relief. These flexible, fully taxable schemes generally trigger income tax and NICs upon exercise, unlike tax-favoured counterparts. They are useful when statutory schemes like EMI or CSOP aren’t suitable.

Growth Shares

Growth shares are a class of shares that give employees the right to participate only in the company’s future growth, not its current value. Their value depends entirely on the company’s growth after they are issued. Hence, they will be worthy only when the company grows beyond the preset value.

Growth shares suit smaller, high-growth tech companies lacking the financial resources for high salaries. Their lower initial value allows employers to use them as a share incentive plan to minimise initial tax liability while aligning employee rewards with long-term company growth.

Restricted Stock Units (RSUs)

RSUs, or Restricted Stock Units, are an equity compensation plan that awards employees with a specific number of company shares at a predetermined price. It works as an alternative to a share option that a tech company can use for compensation.

RSUs are shares granted upfront, but employees gain full ownership (vesting) over time or upon meeting conditions (e.g., employment duration, performance goals) outlined in the RSU agreement. RSUs are typically granted at no cost, thus incurring no immediate tax. However, once RSUs vest and become actual shares, their market value is treated as taxable income, subject to Income Tax and National Insurance.

Joint Share Ownership Plans (JSOPs)

Joint share ownership plans (JSOPs), also known as Joint ownership arrangements, permit a company to grant employees an interest in the business without immediately conferring complete share ownership. These arrangements are also referred to as jointly owned equity and shared growth plans.

A Joint Share Ownership Plan (JSOP) allows an employee and a third party, often an Employee Benefit Trust (EBT) trustee, to jointly own shares. The trustee holds legal ownership and the original value of the shares, while the employee is entitled to the future economic benefit of any increase in the share value above a pre-set starting price (the hurdle or threshold) at the time of the award.

Understanding the taxation of JSOP

As the employee’s benefit comes from growth in the assets (shares) they beneficially own, it is considered a capital gain rather than employment income. Consequently, the value of these shares is subject to capital gains tax. It is noteworthy that, unlike traditional share options, which often result in income tax and social security charges when exercised, shares awarded under a joint ownership plan are more tax-efficient. It is because the capital gains tax rates are usually lower than income tax rates. As a result, a JSOP becomes a tax-efficient alternative to other non-tax-favoured options for companies to reward the long-term value creation of their employees.

Conclusion

Employee share schemes and rewards are intended to incentivise the employees in tech firms and recognise their contributions to the business. Each share incentive plan comes with several setup requirements and tax obligations, though tax-optimised schemes have fewer liabilities. The tech directors sign up for these company incentive schemes to retain the best players, uplift their morale and productivity, and bolster their long-term commitment towards the business. Nonetheless, this post has been written for general information only and should not be considered final advice. For guidance tailored to your specific circumstances, it is advisable to speak to a qualified technology accountant.