The Patent Box Scheme was designed for UK companies to pay less corporation tax while protecting their intellectual property or IP. Businesses can benefit from a lower 10% Corporation Tax rate on their profits through the owned patents.

The Patent Box scheme was introduced in April 2013 and underwent major changes in 2016 to match international standards.

What is a Patent?

A patent gives you exclusive rights to your invention. No one else can make, sell, or use it without your permission. Your patent must be granted by one of these organisations to qualify for Patent Box benefits:

- The UK Intellectual Property Office (IPO)

- The European Patent Office (EPO)

- Specific EEA countries with similar patenting standards

To qualify for a patent, an invention must meet three critical criteria:

- Novelty

- Inventive Step

- Industrial Applicability

Novelty is one of the most important requirements. A fundamental question to address early in the patent process is: “Has the invention already been disclosed to the public?” If it has, securing a patent may not be possible.

When evaluating the inventive step, it’s useful to consider what a skilled technician in the field might do when faced with the same problem. If the solution seems obvious or predictable, the invention may not qualify for a patent. However, if the technician could have chosen from multiple approaches and the one taken by the inventor isn’t immediately apparent, the invention is more likely to involve an inventive step.

Many inventors mistakenly believe their invention is “obvious,” often because they undervalue their unique contributions. This perception can lead to missed opportunities for protection.

If you’re unsure whether your invention qualifies for a patent, we’re happy to offer initial tax consultations to explore its potential and guide you through the patenting process.

Benefits of the Patent Box for Reducing Corporation Tax

The Patent Box can save your business substantial tax money by reducing its corporation tax:

| Standard Rate | Patent Box Rate | Potential Savings |

|---|---|---|

| 25% | 10% | Up to 15% |

The lower rate applies to profits from patent-related activities like product sales, licencing revenues, and infringement income.

Need a reminder about corporation tax for businesses?

Our guides explain everything you need to know about corporation tax and ways to reduce your tax bill:

When Does a Patent Have to be Granted?

It would help to claim the reduced tax rate if you had a granted patent. The good news is you can claim Patent Box relief retroactively. After getting your patent, you have two years from the end of your accounting period to join the regime, which protects your tax savings during the patent application process, which usually takes 12-18 months.

You can only claim relief once your patent is granted. However, your first claim can include profits from the pending period if you join the regime within the allowed timeframe.

Eligibility Criteria

Your company must meet specific criteria and conditions to qualify for the Patent Box tax relief. A clear understanding of these requirements plays a vital role in accessing the reduced 10% Corporation Tax rate.

Criteria to qualify for the scheme

These fundamental requirements apply to your company:

- UK Corporation Tax liability

- Profits from exploiting patented inventions

- Ownership or exclusive licence of patents

- Qualifying development work on the patents

- Active ownership conditions for group companies

What makes a patent-eligible?

Your patent qualifies for the Patent Box regime when granted by these authorities:

- UK Intellectual Property Office (UKIPO)

- European Patent Office (EPO)

- Specific EEA countries including Austria, Bulgaria, Czech Republic, Denmark, Estonia, Finland, Germany, Hungary, Poland, and Portugal

Qualifying intellectual property (IP) rights

Your company can benefit from several qualifying IP rights beyond standard patents:

| Type of IP Right | Qualification Status |

|---|---|

| Patents | Primary qualifying right |

| Supplementary Protection Certificates | Eligible |

| Plant Variety Rights | Qualifying right |

| Plant Breeders’ Rights | Qualifying right |

Do Companies Need To Profit From Their Inventions To Qualify?

No, you don’t need to profit directly from your inventions. The Patent Box benefits apply when you:

- Hold licences to use others’ technology

- Have rights to develop and exploit the patented invention

- Maintain exclusive rights within at least one national territory

- Possess the right to defend patent rights

Patent Box legislation and rules

The Patent Box scheme was introduced for accounting periods beginning on or after 1 April 2013, aiming to incentivise companies to invest in research and development (R&D) while strengthening the UK’s global competitiveness in technology and innovation.

On 1 July 2016, the Patent Box legislation was amended to increase the level of compliance. To enjoy the benefits, companies are now required to prove that there is a “nexus” between their Research and Development activities and the benefits obtained from the tax as per the Patent Box scheme.

One of the major updates was the introduction of the R&D (‘nexus’) fraction that determines the percentage of qualifying Intellectual Property income that will attract the lower Corporation Tax rate. From 1 July 2021, this fraction will be computed based on all days between 1 July 2016 through to the end of an accounting period. Pre-1 July 2021, the computation considers data from 1 July 2013. Optionally, a firm can include R&D expenditure from a date that should not be more than twenty years before in the nexus fraction computation.

These changes were precipitated by an October 2015 OECD report in which it identified the Patent Box as a potential ‘harmful tax practice’ and particularly pointed out that the scheme relieved some claimants without R&D in the UK. It also noted how multinational companies were able to use this incentive as a base for their tax headquarters in the UK. Such revelations raised concerns of possible tax avoidance through such schemes.

Need clarity on reducing your tax compliance while staying within the law?

Our posts explain the differences and legal practices to get tax benefits:

Who Can Benefit from the Patent Box?

To qualify for the benefits under the Patent Box scheme, your company must meet certain conditions. It should be chargeable to Corporation Tax and make relevant profits that arise from patented inventions. Also, it must be in a position either as the proprietor of the patents or having exclusive rights that are licensed to it. Finally, has to begin the qualifying development activities concerning those patents – which could mean making the patented invention, designing it, or enhancing it.

If your company is elected into the Patent Box regime after 30 June 2016, the benefits are subject to certain restrictions. Specifically, the relief may be limited if your company has incurred expenditure to acquire the patents or has paid to connected parties for their research and development (R&D) activities. These restrictions ensure that the tax benefits are closely tied to genuine R&D efforts directly undertaken or funded by your company.

Group companies and their eligibility

Companies in a group can still benefit from the Patent Box regime if they meet the active ownership condition. Your company must:

- Make the most important management decisions about leveraging patents

- Actively manage your patent portfolio

- Bear the risks and expenses associated with the patent development

Did You Know that Patent Box is not the only tax relief for Group Companies?

Exclusively licencing-in patents

You don’t need to be the original inventor to benefit from the Patent Box. Licensees can qualify by meeting specific requirements:

| Licencing Requirement | Description |

|---|---|

| Exclusivity Rights | Must have sole rights in at least one territory |

| Development Rights | You retain control to develop and exploit the patent |

| Defence Rights | Knowing how to defend patent rights |

| Territorial Scope | Rights must cover entire national territories |

When A Group Company May Hold An Exclusive Licence

Patent ownership and exploitation work differently in group structures. Your group company can hold an exclusive licence in these situations:

- The intellectual property holding company grants exclusive rights within specific national territories

- All but one of these entities (including the licensor) can’t hold these rights in the designated territory

- The group company keeps substantial control over the patent’s commercial exploitation

Important: Group companies don’t need enforcement or assignment rights. They must show genuine commercial involvement with the patented breakthroughs. The Patent Box regime rewards active patent exploitation rather than passive ownership.

Note that your company’s role in developing and commercialising the patent is vital. Your active involvement in patent exploitation can qualify you for the reduced tax rate under the Patent Box scheme, even if another group company owns the patent.

Types of Qualifying Income

Understanding which income streams qualify for Patent Box relief significantly maximises your tax benefits. Your patent exploitation strategy works better when you know which revenues are eligible.

Income sources that qualify for the reduced tax rate

The reduced 10% tax rate can benefit your company through various income streams related to your patented innovations:

| Income Type | Description |

|---|---|

| Product Sales | Revenue from patented products and those incorporating patents |

| Licencing | Income from licencing out patent rights |

| Patent Sales | Proceeds from selling patent rights |

| Compensation | Damages from patent infringement and related insurance claims |

The following income sources do not qualify:

- Regular business income unrelated to patent rights

- Marketing asset returns (income from branding rather than technical innovation)

- Income from partial territorial rights

Related Resource: How to register a Trademark?

Identifying Income From Exploiting Patented Inventions

Your income source needs careful analysis to identify qualifying income. At least one of these activities must generate your qualifying intellectual property income:

Direct Patent Exploitation

- Sale of the patented product

- Products that embody your patented invention

- Ones that supply fitted spare parts to patented products

Manufacturing and Service Uses: The Manufacturing or service sector can qualify for income in the following ways:

- Patented processes used in the manufacturing process

- Services provided using patented equipment

- Patented innovations used in their operations

Pro Tip: Notional royalties can count as qualifying income— when your patent is part of a larger product or service. This way, the value contribution of your patent to the overall revenue stream is represented.

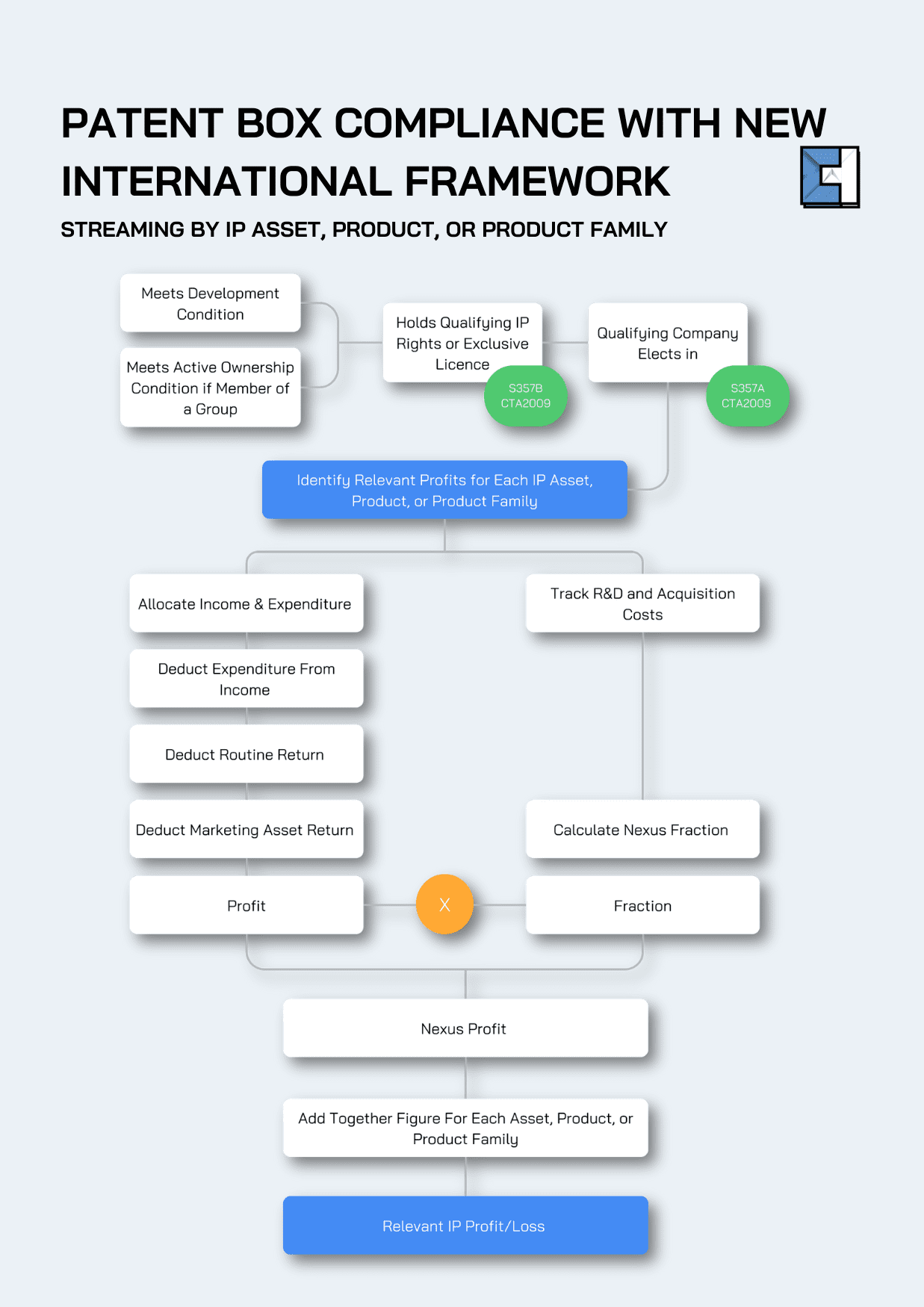

You must stream your income separately for each patent or product family since July 2021. You need detailed records that clearly show— qualifying and non-qualifying revenue streams and the difference between these two.

Calculating Profits Under the Patent Box

Patent Box benefits calculation needs attention to detail and knowledge of specific computation methods. You need to identify eligible profits and apply the right calculations to determine tax savings.

Identify Profits From Intellectual Property

Start by separating your IP-related income from standard business revenue. This process includes:

- Identifying direct patent-related sales and licencing income

- Calculating notional royalties for embedded patents

- Allocating appropriate costs to IP-related activities

Which Profits To Enter Into The Patent Box

Since July 2021 the best thing about the streaming method is that it is now mandatory to calculate Patent Box profits. The approach allows you to allocate income and expenses to separate streams for each patent or product family. Your streaming calculation should then be focused on profits that in essence:

- Come directly from patented innovations

- Generate from qualifying IP rights

- Have proper documentation with supporting evidence

Calculating R&D fraction / Nexus R&D Fraction

The R&D fraction is critical in computation of the benefits of the Patent Box. This fraction basically ties your tax relief to the actual R&D activities and uses this formula:

| Component | Description |

|---|---|

| Numerator | In-house R&D + Qualifying External R&D |

| Denominator | Total R&D + Acquisition Costs |

| Maximum Value | 1 (or 100%) |

Your R&D fraction hits 1 when you have no acquisition costs and all R&D is in-house or through third-party contractors.

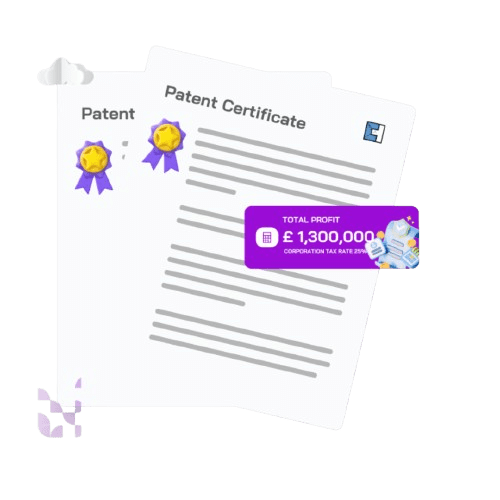

Patent Box Example Calculations

We take a company whose earnings come from its intellectual property and amount to £1.3 million. Here is how the benefit from Patent Box is calculated as well as the potential savings.

| Year Ending 31 December 2024 | |

|---|---|

| IP Profits | £1,300,000 |

| R&D Fraction | 1 (indicating all R&D activities are qualifying) |

| Relevant IP Profits | £1,300,000 |

| Patent Box Deduction | £780,000 |

| Corporation Tax Saving | £195,000 |

At a 25% Corporation Tax rate, the Patent Box deduction is calculated as:

((25% – 10%) / 25%) x £1,000,000

Important: Your actual tax savings will be different and depend on several other factors, including the R&D fraction and profit share from patented innovations. Maintain detailed calculations and supporting documentation for HMRC review.

A tax specialist can help ensure accurate computations and maximum eligible relief. The calculations get complex with multiple patents or product streams.

How to Claim Patent Box Relief?

Timing, documentation, and procedures are involved in claiming the Patent Box successfully. For a claim to be successful, the innovation must also be certified by the U.K. Intellectual Property Office (IPO). A company is a key beneficiary of the Patent Box if its staff are mainly involved in research and development during employment. Furthermore, the company’s expenditure on direct research and development must be significant as well. The following is a guide on the steps and requirements that one has to follow to receive tax relief.

Timing and Form of the Patent Box Relief Election: The Patent Box relief election is time-barred. It has to be made two years after the accounting period that the profits arise. There are two ways to elect: either including it within your computations as part of the Company Tax Return or making a written election directly to HMRC.

Note: There is no prescribed format. However, your election has to be in writing, with the document making it clear that you wish to claim Patent Box relief.

Patent Box Corporation Tax Relief Claim Process

Follow these key steps to a successful claim

| Step | Requirement | Documentation |

|---|---|---|

| 1. Income Identification | Separate IP income streams | Detailed revenue records |

| 2. Profit Calculation | Apply streaming methodology | Calculation worksheets |

| 3. R&D Fraction | Calculate for each IP stream | R&D expenditure evidence |

| 4. Documentation | Prepare supporting evidence | Patent certificates, licences |

| 5. Submission | File with tax return | Election statement |

The following steps and requirements are outlined by HMRC for electing into the Patent Box regime:

| Step | Details |

|---|---|

| Notice to Elect | The company must give written notice of the election (CTA10/S1119). The notice must specify the first accounting period for which the election will apply. |

| Timing of the Election | The election must be made within 12 months of the fixed filing date of the tax return for the first accounting period to which the election applies. |

| Methods of Election | The election can be made separately in writing before the relevant accounting period begins. It can be made in the computations accompanying the tax return or an amendment to the return, provided this is done within the 12-month timeframe. Note: There is no special format required. A corporation tax computation including a deduction for relevant IP profits can be treated as an election if it clearly indicates the intent to claim Patent Box relief. |

| Effect of the Election | he election takes effect from the start of the specified accounting period and applies to all trades and subsequent accounting periods until revoked. |

Your claim must demonstrate a direct nexus between R&D activities and profits from patented innovations. In respect of accounting periods beginning on or after 1 July 2021, you must reference the streaming method and allocate income and expenses to different streams for each patent or product family.

Potential challenges in the claiming process

The Patent Box claim process comes with several complex aspects:

- Keeping detailed records for each patent stream

- Splitting costs accurately across revenue sources

- Working out the R&D fraction for qualifying streams

- Acquiring Patent certificates and licencing agreements

- Maintaining records that show qualifying activities

- Keeping financial records of profit streams

- If you own multiple patents or product families

- Getting patents through licencing from other companies

- Working as part of a group structure

Professional guidance can be valuable when preparing your claim. A tax specialist helps ensure accurate calculations and proper documentation that meets HMRC requirements. They can also help you get the maximum relief while complying with current Patent Box rules.

Note that your Patent Box claim fits into your overall tax strategy. Your calculations and documentation should line up with R&D tax relief claims and other tax matters.

Can R&D tax Credits and Patent Box Work together?

Many people think that they might have to pick between the Patent Box and R&D tax relief. The truth is these two tax incentives can work together and maximise your tax benefits throughout your innovation trip.

R&D tax relief and the Patent Box regime serve as complementary tools in your tax planning toolkit. Let’s look at their differences and how they work together:

| Aspect | R&D Tax Relief | Patent Box |

|---|---|---|

| Focus | Development costs | Commercialisation profits |

| Timing | During R&D phase | After patent grant |

| Tax Benefit | Relief on R&D spending | Reduced rate on profits |

| Rate | Up to 27% for SMEs | 10% effective rate |

Using both reliefs gives you multiple advantages:

- Tax relief during the development phase through R&D credits

- Reduced Corporation Tax on resulting profits via Patent Box

- Improved return on your innovation investment

- Protection for your intellectual property with maximum tax efficiency

The key difference between these reliefs is in their timing and focus. R&D tax relief rewards your research and development spending. The Patent Box offers a lower effective tax rate on profits from your patented innovations.

Strategic use of both reliefs creates an in-depth tax strategy that supports your innovation from original research to commercial success. The Patent Box regime’s 10% rate on qualifying profits adds to the upfront support from R&D tax credits. This creates a powerful combination for innovative businesses.

These reliefs work together but have different calculation methods and eligibility criteria. Your R&D activities strengthen Patent Box claims through the nexus fraction. Your patent strategy helps maximise the commercial benefits of R&D investments.

Additional Resources

- The Complexities of UK Corporation Tax for Non-Resident Companies

- 12 Biggest Mistakes While Claiming R&D Tax Allowance

- UK Tax: A Brief Overview of Taxation in the United Kingdom

- Guide to Creative Industry Tax Reliefs

- Entrepreneurs’ Relief: This is what you need to know

- Which Investment Relief is for you: IR, ER, SEIS or EIS?

- Claiming tax relief on employment expenses

FAQs

What are the tax advantages of the Patent Box?

The Patent Box scheme offers a deduction that lowers the profits subject to the standard Corporation Tax rate. Essentially, this results in the same tax liability as if the profits from the Patent Box were taxed at a favourable rate of 10%, with other profits taxed at the main rate.

What intellectual property tax relief is available in the UK?

Introduced on 1 April 2013, the Patent Box is a tax relief initiative allowing companies to pay a reduced corporation tax rate of 10% on income earned from qualifying patented inventions and certain other intellectual property rights.

Is it possible to claim both the Patent Box and R&D tax credits?

Yes, businesses can benefit from both Patent Box and R&D tax relief simultaneously. These schemes complement each other and support the entire innovation process within UK businesses, dispelling the myth that one must choose between the two.

What does the IP box tax relief entail?

Introduced in 2019, the IP Box tax relief, or Innovation Box or Patent Box, is designed to foster research and development by offering a preferential tax rate of 5% on income derived from protected intellectual property rights.