Property accounting encompasses a vast array of specialisations, but, in simple terms, can be considered a combination of financial management tasks carried out within the property industry, tailored to the specific niche involved. The process can include generic accounting and tax practices, but also contains niche-specific property accounting areas that cater to the industry’s requirements. These can include, but are not limited to, areas such as trust accounting, leasehold accounting, fund accounting, and buy-to-let accounting. The specialised financial management and reporting services ensure that key compliance requirements, savings and strategies are not missed.

A variety of specialised property accounting software can be used to manage specialised finance areas, generate reports and assist in everyday accounting tasks. A few of these software are MRI Global, Hammock, and Propman, among others. Some of these can be straightforward to implement, whereas others may require assistance from specialists. It is always advisable to include your CFO or accounting firm in the decision-making process when selecting software for your business that meets your specific needs.

Maximise returns on your buy-to-let investments with our extensively researched guides to help you understand complex tax rules.

What Are The Key Areas Of Property Accounting?

Accounting for property management companies and landlords can be divided into different areas depending on the property type, its usage, and the income generated. The property can be used for passive income (by renting it out), for capital appreciation as an asset, or as part of an investment portfolio. Each type of income and usage demands bespoke accounting.

Property Accounting for Investment Property

Investment property accounting involves how companies or individuals account for the properties that they hold as an investment. These can be rentals, or they can be kept as assets to sell once they appreciate in value.

Rental Income

Profit from rented property is subject to income tax, which is payable by the owner. The tax treatment of each portion of the income is different. For example, if the owner uses half of the property for personal use and the other half for renting out, the tax calculation includes the rental income for the portion rented only, minus allowable expenses.

Should a corporation own the property, corporation tax will be due on the rental income. Tax rates, property ownership, available incentives, depreciation, capital allowances, location, and relevant tax treaties all affect the amount of tax due.

Company and individual tax reliefs are not the same. On rental income, people might be qualified for tax breaks, such as personal allowances and deductions for authorised costs, but mortgage interest is not a tax-deductible expense for individuals; instead, they can be eligible for a basic rate reduction on their financing costs.

Property maintenance is one of the expenses that both individuals and businesses can claim against their taxable income. Depreciation, capital allowances, mortgage interest, and some tax benefits for rental properties may also be deductible for corporations.

Capital Gains

Individuals are supposed to pay capital gains tax if they sell a property they purchased as an asset that has increased in value. The capital gains tax rate for gains received by selling residential properties is generally higher than other asset types. The capital gain tax, according to HRMC, is applicable for a residential property if:

- It is not the home you currently reside in

- You are using it for business

- You have not lived there for a long time

- Or it is bigger than your needs

Non-resident Capital Gains Tax (NRCGT) applies to non-residents of the UK, including companies and individuals who sell or buy property in the UK. Private residence relief might also apply in certain scenarios.

Chargeable Gains Eligible for Corporation Tax

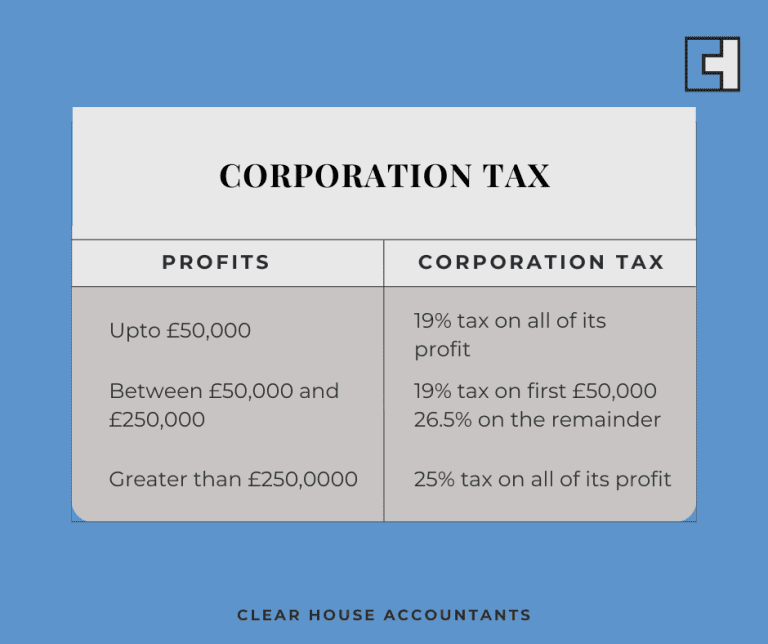

Companies must pay corporation tax if a property is disposed of and generates a chargeable gain; this is applicable when the gain on disposal is made by a company instead of an individual. The tax rates to calculate the tax liability can vary each year; the UK government has announced two new corporate tax rates from 1 April 2023.

- Companies making small profit pay 19%

- The primary profit tax is 25%

Non-resident UK companies will not be eligible for the 19% tax rate.

Recording and Accounting Standards

Correctly recording investment property transactions within accounting standard regulations is essential for corporations. Depending on their size and nature, companies must adhere to different investment property accounting policy standards, such as The International Financial Reporting Standards (IFRS) or UK Generally Accepted Accounting Practices (UK GAAP). For companies reporting under UK GAAP, tools that support FRS 102 lease accounting software can streamline lease classification and compliance processes.

Further, according to HMRC, a Corporation Tax Return (CT600) must also be submitted annually if you are a limited company landlord.

- If you are an individual looking to move your company to an LTD, read our Guide on Transferring Property To A Limited Company

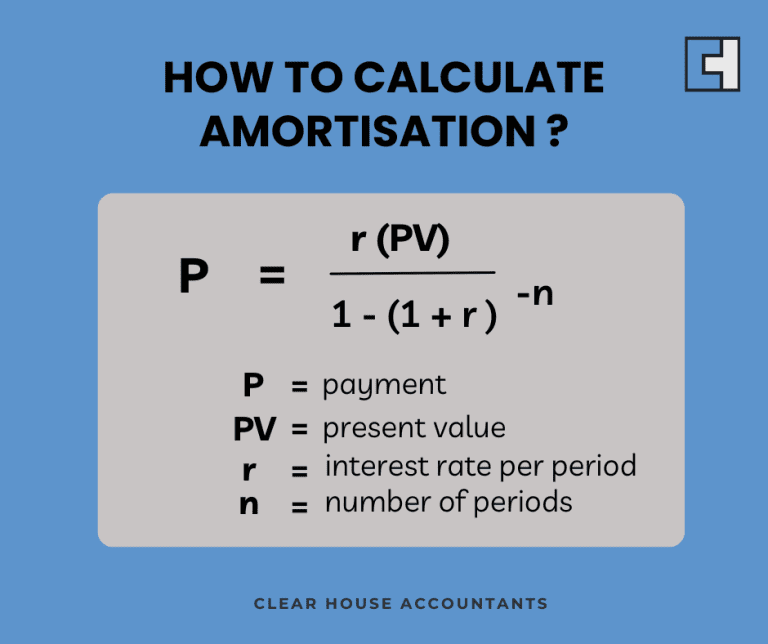

Depreciation or Fair Value Measurement

Depreciation, Amortisation, and Fair Value are methods to determine the value of property assets once their initial recording is made on the balance sheet.

Depreciation is the written-down value of the assets used in a business over their useful life. Depreciation is not a deductible cost for tax purposes but is deducted from the company’s profit in the profit and loss statement. To calculate the depreciation, you need to:

- Add the time since you started using the asset

- The useful life of the asset

- The original cost of the asset

- The value of an asset after its useful life

- Any costs that are included while disposing of the asset

Land is not depreciated, but buildings, plants and machinery are depreciated.

Fair Value is the measurement of investment property or assets at their current market value. Losses and profits are included in the company’s net profit or loss accounts when they crystallise, such as when the asset is sold. Fair value treatment is not allowed as per FS105 micro-entity accounts, in which case the depreciation route would have to be followed. We recommend speaking to your accountant about these areas to make the best decision for the business.

- Benefits of integrating fair value with “The Profit And Loss Account: A Tool To Increase Business Profitability” to optimize your financial strategies.

Value Added Tax or VAT

VAT can be charged depending on the nature of the transaction and the status of the parties involved in that transaction. VAT on residential properties is exempt, but VAT can apply when the property is a new residential development being sold.

VAT is charged on the sale and lease of commercial properties. The rate can vary depending on certain factors, such as whether the property is new or old or has undergone any major alterations.

- Standard rate of 20%

- Reduced rate of 5%

- Zero-rated at 0%

Stamp duty land tax (SDLT)

Stamp Duty Land Tax (SDLT) is payable in England and Northern Ireland if you purchase land or property above a specific amount. SDLT applies when purchasing a freehold, leasehold, or shared ownership property or when a property is transferred in return for money. For residential properties, the SDLT threshold is £250,000; for non-residential buildings, it is £150,000; and for first-time purchasers, it is £425,000 on properties up to £625,000. The use of the property, the buyer’s residency status, and their eligibility for relief all affect SDLT. The value paid—including any debts or extra payments—is used to compute SDLT.

Fund Accounting for Property Asset Management

Property fund accounting involves the management of the financial records for the property investment fund. It includes figuring out the fund’s Net Asset Value (NAV), monitoring rental revenue and expenses, and routinely valuing properties. For investors, their accountants will generate financial statements and reports that guarantee correct tax reporting and regulatory compliance within fund accounting rules and regulations.

To keep the liquidity ratio high and enable the possibility of issuing investor dividends, the fund accountants will also help improve the management of cash flow. In this process, fund analysis will help in assessing the effectiveness of the fund and the investment choices, which will further help in determining the choice to add or remove assets from the portfolio. For efficient management and reporting of property investments, this specialised fund accounting blends conventional accounting concepts with real estate expertise.

Types of Real Estate Funds

REITS:

Companies that hold, manage, or finance income-producing real estate are known as real estate investment trusts or REITs. They give private investors a means of participating in the profits generated by owning commercial real estate without actually having to purchase, manage, or finance any properties. Dividends from REITs must equal at least 90% of their taxable income. Since most REITs are listed on large stock exchanges, they provide a high degree of liquidity. Equity REITs own and manage assets; mortgage REITs lend money to real estate operators and owners. Real estate assets can be included in the portfolios of investors thanks to this structure, which also benefits from the income and possible capital appreciation.

Property Unit trusts or open-ended investment companies

OEICs are investment vehicles that work by issuing shares and are considered companies. Unit trusts include pooled money that issues some units to each investor.

Property Syndicate

Property Syndicate is the second most popular property asset-holding fund in the UK, where a group of investors pool together to purchase or invest in a property. It can be either long-term, such as ownership investment, or short-term, such as property development.

These investments are called open-end investments as they are actively managed, and there is no limit on how much money you invest.

Property Crowdfunding

It includes different platforms where investors invest a small amount in a real estate project and receive returns in the form of capital appreciation.

Residential and Commercial Service Charge Accounting

In residential buildings, including apartment buildings or housing estates, residential service charge accounting refers to the management of the expenses related to the upkeep and servicing of common areas. Usually, these expenses cover management fees, insurance, common area utilities, security, landscaping, and repairs. In order to estimate the necessary service charges for the next year, annual service charge budgets are created and sent to tenants. The service charge fee is then collected monthly, quarterly, or yearly from the property owners. Financial statements, issued annually, guarantee openness and demonstrate the use of the money, with the remaining balancing charges also communicated for collection.

Contrarily, commercial service charge accounting addresses the expenses for the upkeep of common spaces in business structures such as malls or office buildings. Cleaning, security, utilities, upkeep, repairs, and administrative expenditures are all included. As with residential service charge accounting, tenants receive yearly budgets that include the projected costs. The business tenants pay their charges as per the terms of their lease. In-depth financial records are provided to the tenants to ensure accountability and to provide transparency around the use of service charge monies, with the balancing charge communicated.

RICS and ARMA are the regulatory bodies to ensure best practices within the industry according to the following regulations.

- Landlord and Tenant Act 1985 (UK)

- Commonhold and Leasehold Reform Act 2002 (UK)

- Commercial Leases and Lease Agreements

- Code of Practice for Commercial Leases (UK)

The FCA(Financial Conduct Authority ) also plays a key role when it comes to investing regulations.

Market Valuation of Properties

Independent market valuation is crucial for property owners, as it helps determine SDLT, CGT, and mortgage conditions. Property Valuation can be done through:

- A comparative market analysis, or CMA, compares the property to recently sold comparable ones in the neighbourhood.

- Taking into account the rental income, you can use the Gross Rent Multiplier (GRM) or Capitalisation Rate (Cap Rate) to calculate a value.

- Employ an Agent or a Chartered Surveyor.

Elements Influencing Appraisal

- Location: Close to shops, transportation, and nice neighbourhoods.

- Size and state of repair of the property are included, as is its layout.

- Market Conditions: Interest rates, economic environment, dynamics of supply and demand.

- Comparable Properties: Locally comparable properties’ most recent sales figures

- Economic Elements: Employment rates and changes in the local economy.

- Land use and zoning laws control how property is used and how much growth is possible.

Conclusion

Property accounting is divided into several sub-sectors. The regulations, compliance requirements and tax implications that will impact you will depend upon the type of property asset you hold or the income it generates. Over the years, many new regulations have been introduced in the property industry, realising that what impacts your business can be key to reducing risk and minimising tax. Due to the intricate complexities involved in property accounting, it is advisable to consult expert property and Service Charge Accountants before making any major decisions.

Additional Resources