The UK property market is seen as a safe place for investors seeking stable returns and long-term growth. Among the most popular forms of property investment is the buy-to-let option, where the investor buys a property to rent it out. It not only generates recurring cash flows but also creates equity gains for investors over the longer term.

Originally, landlords used to purchase these properties in their own personal names and then rented them out to earn a steady income. Even though this can be a lucrative source of income, such buy-to-let options do not offer protection of personal assets, which can be discouraging for many landlords, this is where the conversaion around Holding a Buy-to-Let: Personal Ownership vs SPV conversation comes into play.

As a result, a growing number of investors have turned to an alternative investment structure: Special Purpose Vehicle(SPV). An SPV is a limited company that is specifically created to hold property investments. There are about 415,000 buy-to-let companies operating in the UK, which is more than any other type of business.

The following analysis will provide you with insight into buy-to-let investment: personal ownership vs. SPV.

What Is an SPV (Special Purpose Vehicle)?

A Special Purpose Vehicle, widely known as an SPV, is a separate legal entity which is created for a specific function, such as holding and managing property investments. In the UK, landlords typically set up a special-purpose vehicle through a limited company structure to purchase a buy-to-let.

A limited company is the most common structure for owning and managing buy-to-let properties in the UK. However, there are other structures, such as trusts and partnerships, as well.

A Special Purpose Vehicle can be set up by an individual investor, a group of investors, or an organisation, either as an independent entity or a subsidiary of a parent company.

Understanding the Legal Structure of an SPV vs Personal Ownership

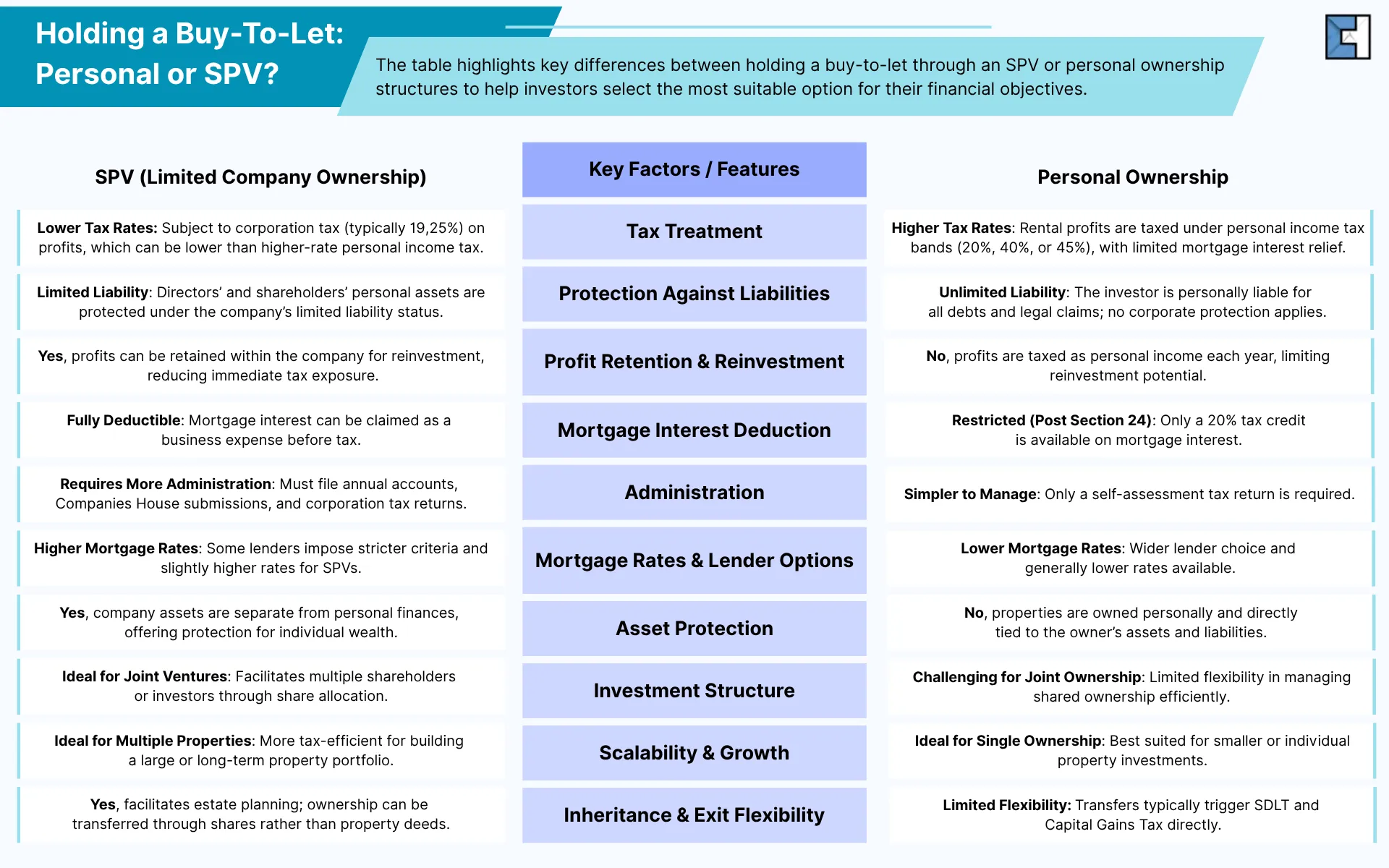

Under personal ownership, an individual landlord purchases a property under their personal name, rents it out, and pays income tax on the rental profits they earn within their personal income tax bands, which can sometimes end up in the high-rate tax band. There are no registration requirements involved, other than having a UTR with HMRC.

On the other hand, since an SPV is a limited company, it:

- Operates under its own name.

- Has its own assets and liabilities.

- Has its own legal status, i.e., it remains legally distinct from its directors and shareholders.

Moreover, an SPV must be registered with Companies House to be incorporated. Likewise, it will have its own company number, bank account, and accounting obligations.

Why Landlords Prefer Setting Up an SPV Over holding a Buy-To-Let personally?

Landlords have two options when it comes to holding a buy-to-let: personal ownership vs SPV. However, the option of an SPV is quite popular among investors in the private sector for:

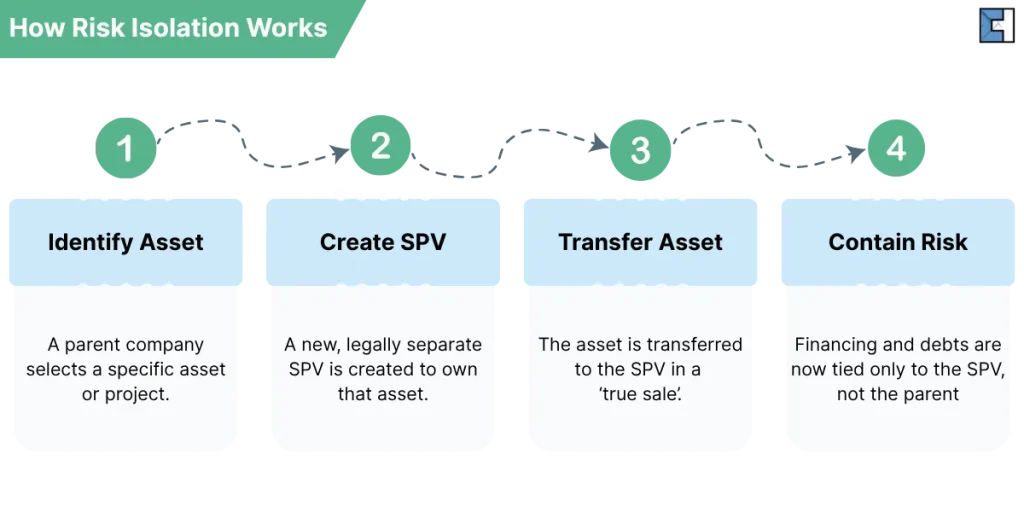

Isolating Assets

If an SPV incurs losses or debts, they will have no impact on the assets of the parent company or the individual who ultimately invests in the property. Should an SPV face insolvency, the repercussions are restricted to that entity, thereby safeguarding the owner’s personal assets and other business ventures.

The following image illustrates how asset isolation from risks works:

Holding and Managing Buy-To-Let Properties

For landlords and property investors, SPVs serve the particular purpose of holding and managing buy-to-let properties. Separating property investments from personal finances can yield potential tax benefits. This distinction conveys a more professional image to prospective lenders and partners. Personal ownership does not provide these benefits or project the same level of professionalism.

There are several responsibilities associated with renting out a property as a landlord. Learn what they are:

Allowing Investors and Fund Managers To Pool Capital Into One Entity

Unlike personal ownership, SPVs allow investors to pool their capital into a single entity and contribute their funds to it. As a result, each investor can individually track who owns what percentage, how profits should be distributed, and who is responsible for what.

Tax Efficiency

Buy-to-let developers who deal in real estate can benefit from lower corporation tax rates. Moreover, with buy-to-let mortgages, landlords can deduct mortgage interest and arrangement fees from rental income.

Buy-to-let landlords can maximise their tax efficiency with certain useful tax tips:

Raising Capital

The opportunity to raise capital through asset securitisation with an SPV is quite convenient. If an investor wants to raise funds for a business, they can use an SPV to convert the non-liquid assets into cash that are normally hard to sell into investment products. These products can then easily be bought by other people, such as loans or mortgages.

Easy Transfer of Ownership

An SPV allows easy transfer of ownership. In case the SPV owner wants to transfer ownership, like selling the property or passing it to family members, they can do so through the SPV shareholding without transferring the property itself. It is because since SPV owns the property, it can transfer it in the form of its shares held by shareholders.

The Tax and Administrative Implications of Holding a Buy-to-Let: Personal Ownership vs SPV

The landlords should consider the following tax and administrative implications of holding a buy-to-let property personally or through an SPV to make an informed decision:

Income Tax vs Corporation Tax

Under personal buy-to-let, the landlords pay Income Tax on any profit they make from renting out property. They report their income and pay tax by completing a self-assessment tax return.

On the other hand, SPVs are subject to corporation tax payment, which is significantly different from personal taxation applied to individual landlords. The corporation tax rates range from 19% (small profits rate) to 25% (main rate), in line with the current tax year, 2025/26.

At 25%, corporation tax is often more favourable than personal income tax, which can reach 45% for high earners.

There are some key steps involved in filing corporation tax with HMRC, including important dates, accounting period, and the filing process. Find out by referring to the following guide:

Buy-to-let Mortgage

Some specialist brokers cater to mortgages on buy-to-let properties but require that the property be held in an SPV. Most buy-to-let mortgages are structured as interest-only loans. This means the landlords’ monthly repayments will only cover the interest charged on the amount they borrowed rather than the loan itself. Lenders ask landlords to create an SPV (Special Purpose Vehicle) when holding buy-to-let property to separate the property from the landlord’s personal finances or from the risk of other trading companies. It makes it easier for lenders to assess risk and underwrite the mortgage.

Since rental income cannot be accurately predicted in buy-to-let property portfolios, lenders consider buy-to-let mortgages a relatively riskier option compared to a residential mortgage. Consequently, the interest rates and fees on SPV mortgages are generally higher than those for personal buy-to-let mortgages.

When landlords take out a buy-to-let mortgage, lenders will take the following into account:

- A limited company holds the buy-to-let property

- The landlords are higher or additional-rate taxpayers

- Rental yield

- The landlords plan on expanding or remortgaging their property portfolio to a maximum of three residential lettings

- Deposit size (minimum 25%).

- Landlord’s credit history.

- Their existing debts.

In 2025, buy-to-let mortgages will have become more competitive with a wider and larger variety of products available in the market. At the beginning of September 2025, there were 4,597 mortgage products available, the highest count since records were initiated in 2011.

Mortgage Interest Tax Relief

Since April 2020, individual landlords are no longer able to fully deduct mortgage interest from rental income to reduce tax. Relief is now limited to a 20% basic-rate tax credit on mortgage expenses. However, for an SPV, mortgage interest is fully deductible and can be claimed as a business expense before tax.

When an investor purchases a property through an SPV, it falls under the company’s ownership. On this account, they might face mortgage limitations since not all lenders are willing to offer loans to companies. The interest rates on SPV mortgages are often slightly higher when compared to those an individual can get on personal buy-to-let loans, which can also dissuade one from the option of an SPV.

Tax Deduction Through Allowable Expenses

Both landlords and SPVs can reduce tax bills by deducting allowable expenses. Allowable expenses are the costs necessary for running a business. For instance, in the buy-to-let context, maintenance and repair costs, utility bills, accountancy and legal fees, etc., are allowable expenses.

Apart from the allowable expenses, certain tax planning strategies can further reduce the corporation tax bill.

Ineligibility To Claim Personal Allowances

While an SPV can claim allowable expenses, it cannot claim personal allowances, such as the £12,570 income tax allowance that individual landlords receive, because it operates as a standalone entity.

Dividend Taxation

Apart from the corporation tax, when shareholders withdraw or extract rental profits personally via dividends, it triggers dividend taxes based on the tax bracket their dividends fall within. Hence, landlords should consider the combined tax effect of both Corporation Tax and Dividend Tax if they choose an SPV limited company.

Stamp Duty and Capital Gains Taxation

Since an SPV is a limited company structure, any property transfer into it can give rise to Capital Gains Tax, SDLT (Stamp Duty Land Tax), and legal fees.

Administrative Responsibilities

It is among the crucial duties of SPV directors to diligently manage the company’s detailed records, accounts, and tax submissions. As a result, an SPV can bring increased administrative responsibilities. On the contrary, buy-to-let under personal ownership is simpler in terms of administration since only a self-assessment tax return is required.

Set-Up and Running Costs

The personally held buy-to-let has no set-up requirements. Conversely, an SPV involves set-up and running costs. For instance, SPV incorporation, fulfilling annual filing obligations, and hiring accounting services come at a price.

Accounting for property companies and landlords depends on the property type, its usage, and the income generated. The property can be used for several purposes. Find out more:

Bottom Line

Generally, for smaller landlords (with one property), a buy-to-let under personal ownership can be a viable choice. In contrast, for those with a portfolio of assets or multiple properties, setting up an SPV can be a shrewd decision.

Establishing an SPV for property investment and managing its requisite obligations can be streamlined with expert assistance.

At Clear House Accountants, our skilled property accountants in London can help property investors and landlords with the fundamentals of an SPV and the accounting and tax implications around it.

Frequently Asked Questions

What is an SPV in buy-to-let?

In the context of UK property investment, an SPV is a popular limited company structure for a specific, narrow purpose: purchasing buy-to-let properties. A Special Purpose Vehicle isolates the assets of the parent company from any potential losses and liabilities it may encounter.

Can I directly own a property through an SPV?

No, you cannot directly own a property through an SPV. When you set up an SPV (Special Purpose Vehicle), it becomes a separate legal entity from its owners or shareholders. Now, any property will be purchased under the SPV, and it will be its legal owner. In contrast, you own the SPV through your shareholding in it. Thus, your ownership of the property is indirect, through shareholding in that SPV.

Are there any costs associated with setting up an SPV limited company online with Companies House?

Yes, incorporating an SPV limited company with Companies House costs £50 when done online. However, if sent via post or on paper, the cost is £71.

Should a small landlord with a single property choose to set up an SPV limited company?

Technically no. For smaller landlords (with one property), holding a buy-to-let under personal ownership can be a viable choice. On the other hand, if they manage a portfolio of assets or own multiple properties, they should create an SPV.

Additional Resources: