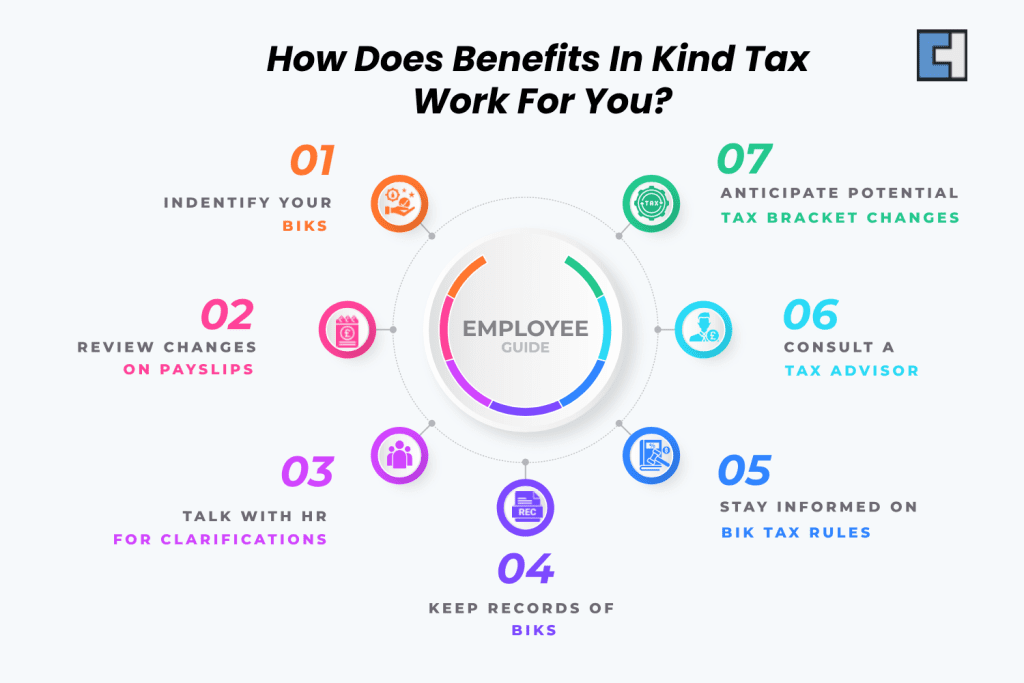

Benefit in Kind Explained

Non-cash benefits, known as Benefits in Kind (BIK), are what companies provide to staff members as benefits within their remuneration package. Things such as company vehicles, private healthcare, gym memberships, and wellness initiatives are a few examples. These perks are meant to draw and retain top talent, But they are not cash; they are liable for taxes, and each has a different taxation approach.

Benefits in kind Taxation Rate

The nature of the benefit significantly impacts the Employers’ need to report BIK to HMRC using forms like the P11D, which records the benefits and their taxable values and tax rate applied. Generally, the value of the benefit is added to the employee’s income and taxed accordingly. However, the method of valuation varies depending on the type of benefit. For instance, the taxable value of accommodation is determined by its rental value, while the company car tax rates are calculated based on factors such as CO2 emissions and the vehicle’s list price. This variation underscores the importance of understanding how different benefits are assessed for tax purposes.

Read our complete guide on company car tax that answers most questions like how does company car tax work and how much is company car tax.

Electric Car Benefit in Kind Tax

BIK rates vary significantly, ranging from 2% for zero and low-emission vehicles to as high as 37% for higher-polluting cars. Notably, the BIK rate for electric vehicles increased from 1% to 2% on 6th April 2022 and is set to remain at 2% until April 2025. These rates reflect the government’s commitment to incentivising cleaner vehicles while progressively discouraging those contributing more to environmental pollution.

As an employee receiving a Benefit in Kind, you are liable to pay income tax on the taxable benefit in kind, considering its value, which means its cash equivalent, as determined by HMRC. To calculate your tax obligation, apply your income tax rate—20% for basic rate taxpayers, 40% for higher rate taxpayers, or 45% for additional rate taxpayers—to the cash equivalent of the benefit. For instance, if your employer provides you with a gym membership valued at £600 annually, and you fall within the basic rate tax band, you would be required to pay 20% of £600 in income tax for this benefit.

HMRC’s Role in BIK Taxation

The taxes of BIK are under Her Majesty’s Revenue and Customs (HMRC). Usually, using Form P11D for every employee receiving BIK, companies must follow HMRC’s instructions in valuing and reporting these benefits. Penalties include fines and interest on unpaid taxes that can follow from non-compliance.

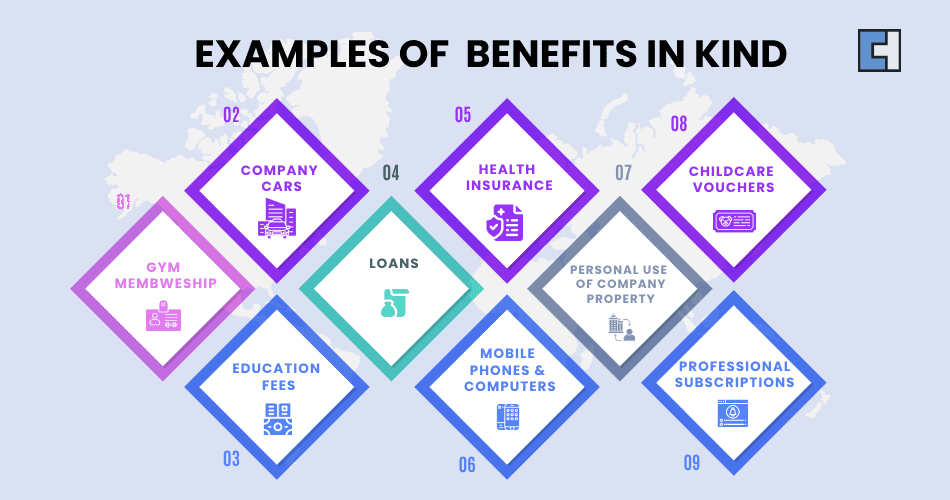

Common Examples of Benefits in Kind

Company Cars: Vehicles provided for personal use by the employer.

Health Insurance: Employer-paid medical services or private healthcare insurance.

Childcare Vouchers: Financial support provided by the employer to cover childcare costs. If your employer does not provide support , there are childcare schemes that government provides that you can avail.

Gym Memberships: Access to fitness facilities paid for by the employer.

Personal Use of Company Property: Allowing personal use of company-owned assets, such as property or equipment.

Loans: Interest-free or low-interest loans granted by the employer.

Education Fees: Payment of tuition or other educational expenses by the employer.

Mobile Phones & Computers: Devices provided by the employer for both personal and professional use.

Professional Subscriptions: Membership fees for professional organisations or subscriptions paid by the employer.

Differentiating Cash from Benefits in Kind

Cash Benefits: Direct payments like bonuses, taxed as income.

Benefits In Kind: Advantages not in cash form, indirect compensation appraised for tax considerations.

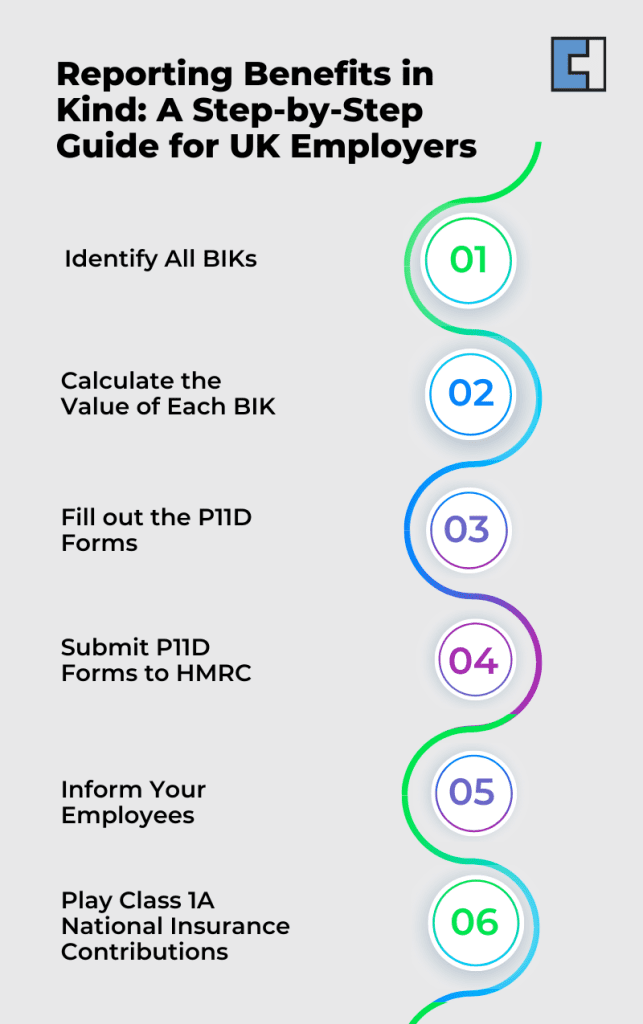

Reporting BIK to HMRC

Employers must report BIK to HMRC using forms like the P11D, which records the benefits and taxable values. For proper tax assessment, this covers employee information, benefit kinds, and cash values. Employers must also pay Class 1A National Insurance on most taxable perks and ensure all filings by the July 6th deadline to prevent fines.

Calculating BIK Tax

Companies must precisely estimate BIK to avoid penalties. The method is broken out here in a condensed form:

- Identify the Benefit: Determine the benefits provided.

- Determine the value of each benefit by applying HMRC rules.

- Compile the values: Add together all the values of every advantage the staff member gains.

- Add the employee’s whole value to their taxable income.

- Determine the tax depending on the employee’s general income, including the benefits’ value.

HMRC offers an online BIK tax calculator for individuals who would rather figure BIK on their own.

Calculate BIK Tax

Payrolling Benefits in Kind

Paying BIK lets companies distribute their tax payments across the year instead of performing an annual filing. Including the value of the perks in the monthly taxable salary of the employee helps to pay taxes gradually. Aiming to simplify the tax procedure, this approach, first presented in 2016, will become required by 2026. You should always get an update from your payroll accountant to understand the latest implications and avoid any unnecessary tax burdens.

Salary Sacrifice Scheme in the UK allows employees to trade part of their monetary salary for non-cash benefits. This arrangement is acknowledged by HMRC as a change to the employee’s pay structure, mainly used to access non-monetary benefits.

Changes with Mandatory Payrolling

Employers today have to turn in P11D forms by July 6th and pay Class 1A NIC by July 19th (or 22nd online). Payrolling taxes on benefits allow payroll to manage them in real-time, therefore lessening the requirement for end-of-year forms. Companies still have to turn in a P11D(b) form for perks not covered by payroll.

Benefits of Payrolling for Employers and Employees

For Employers:

Simplifies reporting lowers documentation and guarantees real-time compliance.

For Employees:

Streamlines year-end procedures, replace payslips with BIK information, and smooths out tax payments.

Payrolling with HMRC: Registration

Before the tax year starts, companies have to register with HMRC or your payroll services provider can use it in your behalf. The simple online procedure tells HMRC to change staff tax codes.

Tax Implications for Common BIK

Taxable BIK: Personal use of corporate assets, meals and entertainment, company automobiles, lodging, private health insurance, non-cash gifts and vouchers.

Exempt BIK: Employer pension contributions, work-related training, small staff discounts, office facilities, and business travel expenditures.

Further Details Regarding Kind Benefits

Little Advantages

Trivial benefits are minor perks provided by employers that are exempt from tax, provided they meet specific criteria. These typically include small gifts or tokens given on occasions such as birthdays or other special events without any upper limit on their value.

Cycle to Work Scheme

This tax-free advantage lets workers get safety gear and bicycles, therefore promoting ecologically sustainable ways of transportation.

Staff Event Allowances

Up to a certain point, companies can offer tax-free allowances for staff activities, including yearly festivities. This encourages team-building actions and a good workplace.

Impact on Employees and Employers

Employees:

- Will see the tax on their benefits in kind withdrawn from their pay throughout the year, enabling them to budget and plan free from unanticipated tax liabilities at the end of the tax year.

- Revised Payslips will clearly show employees their pay package by including information on the perks in kind and the pertinent payroll tax deduction.

- HMRC will change workers’ tax codes to match the payrolling of benefits, ensuring the exact amount of tax deducted all year long.

- Employees won’t have to wait for P11D papers to know their tax obligations connected to benefits in kind. The consistent payroll method will manage everything.

Employers:

- The administrative load of end-of-year reporting will be immediately reduced. No more long hours filling in and turning in P11D papers for pay-rolled benefits.

- Employers will include the value of benefits in kind in employees’ taxable pay each payroll period, deducting taxes as the perks are given.

- Payroll systems will have to be changed to manage the kind of benefit inclusion. Employers may have to invest in changes to current systems or payroll software to ensure correct processing.

Training and Interaction:

- Any significant change will demand that businesses clearly explain it to staff members and offer tools or training to help them grasp the new system.

- Regular deduction of tax on benefits instead of lump-sum payments at the end of the tax year could cause employers to see fluctuations in cash flow.

Additional Resources

Conclusion

Knowing Benefits In Kind and its tax consequences will let companies and staff members better control their tax responsibilities. See a tax services provider for more specific help to guarantee compliance and save money. Contact our staff, who can assist you with all your tax and payroll issues, saving you a bit in the process, for more information and help.