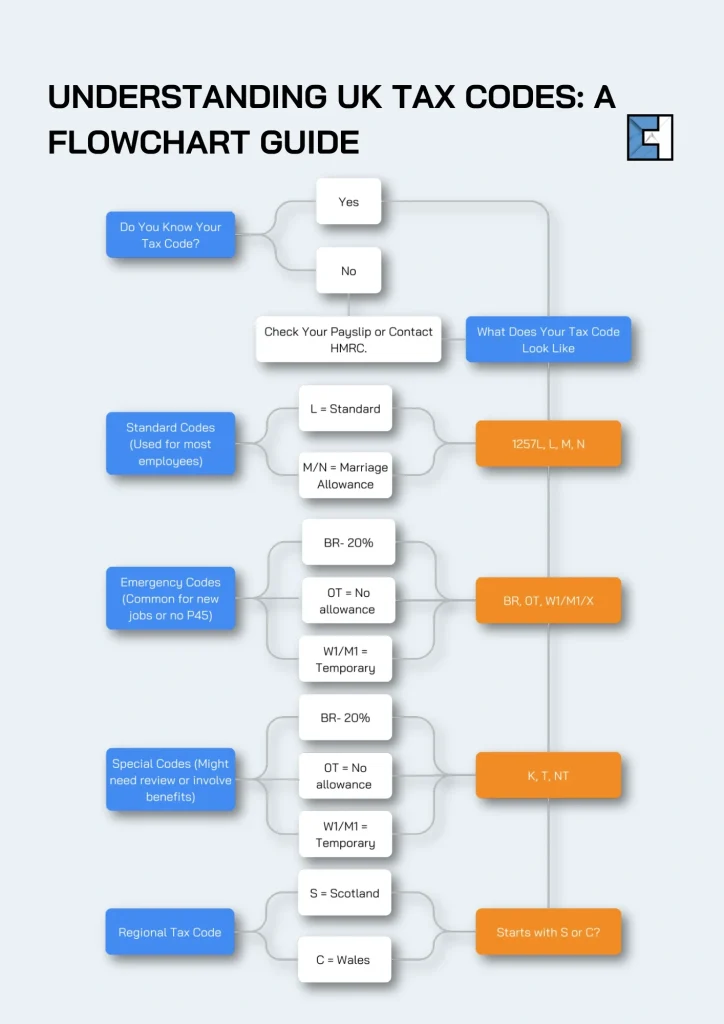

1257L is a common tax code that appears on most UK employees’ payslips. While it might seem like a puzzle, it provides important information. Many people just overlook this combination of numbers and letters, however this code can have a significant impact on your net pay.

The 1257L tax code represents your personal tax-free allowance and directly impacts your take-home pay. Understanding this code will help you verify if you are paying the correct amount of tax. An incorrect tax code could result in you overpaying hundreds or even thousands of pounds to HMRC.

This comprehensive guide explains everything about the 1257L tax code, how it affects your salary calculations, and what steps to take if your tax code needs updating.

What Is Tax Code 1257L, and Who Gets It?

1257L is the most common in the UK, with millions of employees throughout the country being issued with this tax code. This standard code imparts basic information on your tax status to both your employer and HMRC.

The numerical part “1257” directly refers to your tax-free personal allowance of £12,570 for the 2025/26 tax year. HMRC simply removes the final digit when creating the tax code. This allowance represents the amount you can earn annually before paying any income tax. If you earn £30,000 annually with the 1257L code, the first £12,570 is completely tax-free, while the remaining £17,430 is taxed at the basic rate of 20%.

The tax code will change when personal allowance figures are updated. Previously, the standard codes were:

- 2024/25: 1257L

- 2023/24: 1257L

- 2022/23: 1257L

- 2021/22: 1257L

- 2020/21: 1250L (reflecting the £12,500 allowance)

- 2019/20: 1250L

- 2018/19: 1185L

What Does the ‘L’ Mean in Your Code

The ‘L’ in your tax code refers to the fact that you receive the full personal allowance without any matters affecting your tax standing. This letter is very critical, considering it compares your tax situation against those of others with differing circumstances.

Once your income goes over £125,140, you will lose all your tax-free Personal Allowance, and your code will go from ‘L’ to ‘0T’. Equally, if it reads 1257L ‘W1’, ‘X’, or ‘M1’, you have been put on an emergency tax code, which usually happens when the HMRC has not received enough information regarding your income.

Salary sacrifice schemes can reduce your taxable income, potentially helping you stay within the threshold for receiving the full personal allowance

Who Is 1257L Code For?

The 1257L coding is commonly applied to people who:

- Have only one job or pension

- Earn less than £125,140 a year and do not receive taxable benefits from their employer

- They have no untaxed income to report

- Do not receive tax relief for job expenses or professional subscriptions

Conversely, you probably wouldn’t get this standard code if your circumstances are out of the ordinary. For example, a Marketing Manager’s salary £30,000 plus company car benefits of £5,000 and health club membership worth £1800 results in receiving code 577L. This modification reflects their actual personal allowance of £5,770 (£12,570 – £5,000 – £1800).

When your financial setup isn’t so straightforward, these tax strategies can help you plan smarter and stay compliant.

Furthermore, if you get extra allowances e.g., £300 a year for a professional subscription to the British Design Association as a Graphic Designer, your code will change to 1287L, indicating the increased tax-free allowance to £12,870 (£12,570 + £300).

Your tax code varies if you have two jobs since your personal allowance has to be apportioned between them or if you draw a retirement pension as well as earnings from employment.

Where to Find Your 1257L Tax Code?

Your tax code appears on your payslip, where the code typically displays prominently near your personal details. Additionally, both your P45 (received when leaving a job) and P60 (issued annually by your employer) clearly list your current tax code, and on any official correspondence from HMRC regarding your tax affairs, including tax code notices sent at the beginning of each tax year.

For those with multiple income sources, bear in mind that each employer or pension provider will have their tax code for you, as your allowance may be split between different income streams.

Managing multiple income sources or staying on top of your records? These guides can help you keep everything aligned.

What to Do if Your Code Looks Wrong

If you spot any error with your tax code, you should contact HMRC directly using their dedicated helpline at 0300 200 3310 and keep a record of it. Alternatively, you can raise concerns through your Tax Accountant via an online account, which is faster and more straightforward.

If you discover you’ve been overtaxed because of an incorrect code, you’re typically entitled to a rebate. HMRC usually issues a P800 form detailing any overpaid tax and instructions for claiming your rebate. You can then claim online through your personal tax account or by contacting HMRC directly.

Multiple income sources commonly create tax complications. For instance, if you receive both employment income and a pension, your 1257L code should reflect this dual income situation. If your payslip doesn’t show an updated code after starting a pension, you might face unexpected tax underpayments or overpayments.

When and How to Claim a Tax Rebate

If you have overpaid tax because of the emergency code, you can claim back the difference. Usually, you will receive a P800 form from the HMRC that details any overpaid amount along with instructions on how to claim your rebate.

To claim tax back:

- You need to log on to your Personal Tax Account available at the HMRC website

- Follow the online claim process; or

- If you would like to talk to someone, get in touch with an advisor from HMRC

It is usually, the overpayment is picked up by HMRC automatically but stay alert with your tax code, especially after getting a new job or any big changes in life that would impact your income.

Conclusion

Tax code 1257L is, of course, one highly important indicator in determining how much money you bring home, yet many ignore its importance. So we broke down in this manual what this standard code means, what it equates to your personal allowance of £12,570, and why it’s crucial to check its accuracy for the sake of your financial health.

Bear in mind the fact that HMRC operates millions of tax codes each year, almost making mistakes certain. Thus, checking your tax code on a regular basis could save you hundreds, if not thousands of pounds, in tax that you do not need to pay. This becomes especially necessary as and when your circumstances change, be it when you start a new job, start receiving benefits from a company, or have more than one source of income.

Additional Resources