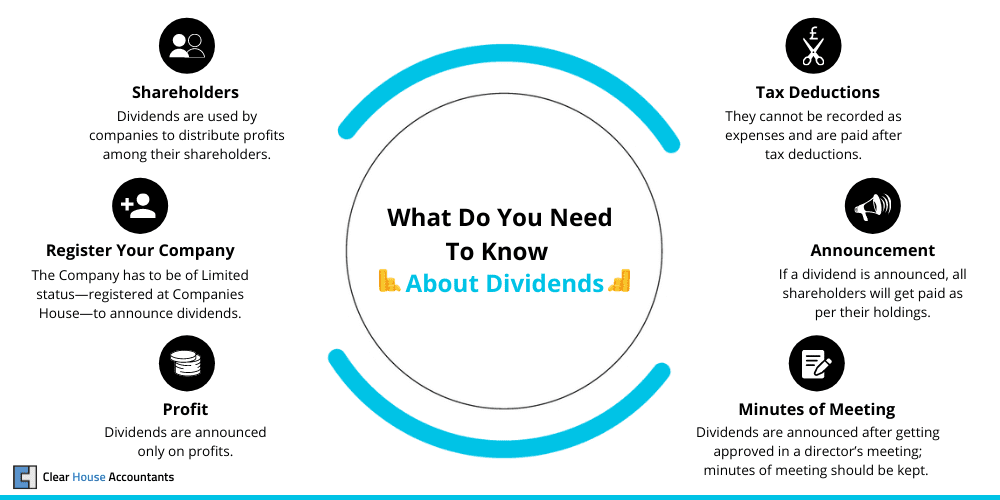

Dividends are how limited companies distribute their profits among shareholders; they are generally one of the tax-effective ways to pay directors or other employees of an organisation as part of their remuneration package, only if they own company shares. The dividend payments are proportionate to the shares held by a shareholder. Dividends cannot be recorded as expenses for taxation-saving purposes but are paid after corporation tax is deducted from the profits.

Dividend Issuance

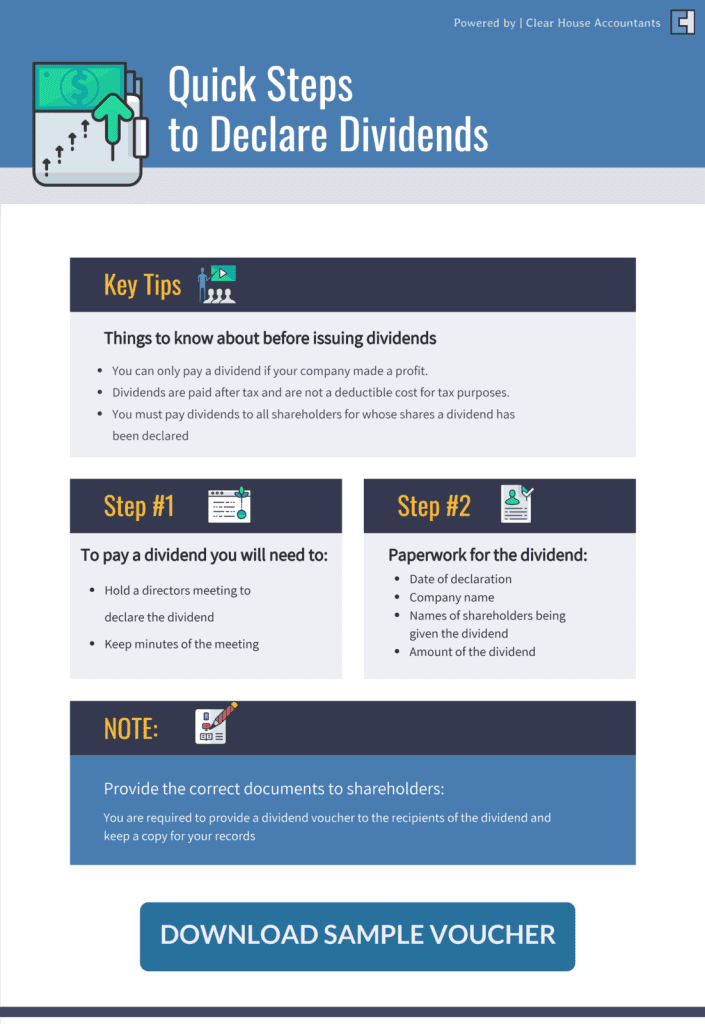

Before announcing dividends, the dividends have to be approved in a director’s meeting, and the minutes of the meeting need to be documented. Dividends are usually paid at the end of the year, but interim dividends can also be paid at the directors’ recommendation.

Shareholders are then issued a voucher with their name, dividend date, company name, and dividend amount.

Dividends are only paid on the profit, and it is incorrect for a company to announce dividends on losses. Dividends paid can be declared if a company has retained earnings, even though it might have made a loss in that specific year.

Tax on Dividends

Companies are not liable to pay taxes on dividends as they pay corporation tax on the overall profit. Individual shareholders, however, do need to pay tax on dividends exceeding the allowable limit of £2,000 for the year 2021/2022, i.e. the tax-free dividend. The tax-free dividend allowance is utilised after the personal allowance limit gets exhausted, i.e. £12,570 for the year 2021/2022

UK Dividend Tax Rates & Threshold

There are three different tax rates for dividends depending on the threshold of an individual’s savings income tax band and income tax rates. However, the dividend tax rate on total dividend income will be increasing by 1.25% from April 2022. This tax rise to taxable income from dividends is to help support social care and the NHS.

The Year 2021/2022

| Level | Tax Rate | From | To |

| Basic rate taxpayer | 7.5% | £2,000 | £37,700 |

| Higher rate taxpayer | 32.5% | £37,701 | £150,000 |

| Additional rate taxpayer | 38.1% | £150,000 + |

Proposed For the Year 2022/2023

| Level | Tax Rate | From | To |

| Basic rate taxpayers | 8.75% | £2,000 | £37,700 |

| Higher-rate taxpayers | 33.75% | £37,701 | £150,000 |

| Additional rate taxpayers | 39.35% | £150,000 + |

Let’s suppose that a person’s only source of income is dividends received, and his investment income from mutual funds or other sources in the financial year 2021/2022 is recorded at £60,000. The person will be liable to pay £5,339.75 in taxes (single person tax code 1257l), i.e.

| Amount | Tax Rate | Tax liability |

| £12,570 | Exempt—personal allowance | nill |

| £2,000 | Tax-free dividend allowance | nill |

| £37,700 | Basic rate taxpayers—7.5% | £2,827.5 |

| £7,730 | Higher rate taxpayers—32.5% | £2,512.25 |

| Total tax liability on £60,000 | £5,339.75 |

An Efficient Way to Pay Tax on Dividends

For Employees or Directors who are also shareholders, when designing remuneration packages, dividends, alongside pay, can be used to significantly reduce the tax charge of not only the public limited company but also the individual. Using a mix of dividends, salary, and bonuses is advisable as certain benefits can only be availed through salary, such as the right to state pension, etc. This needs to be carefully evaluated as to what proportion of salary and dividends should be devised to reach maximum tax efficiency.

The salary should be below both the primary threshold of Employee National Insurance Contributions, i.e. £9,568 per year (for the 2021/22 tax year) and the secondary threshold of Employer NICs, i.e. £8,844 per year (for the tax year 2021/22) to avoid any NI payments, but to remain entitled to some basic NI benefits you should make sure the salary is above the Lower Earning Limit.

Earnings between the primary threshold and the upper earnings limit are taxed at 12% on the employee earnings, whereas employers have to pay NIC at 13.8% on top of the salary payments above the secondary threshold. You should note that the upper earnings limit is set to £50,270 per year ( £967 per week and £4,189 per month)

A Case Study to Illustrate

A company director with shares or an owner of a limited company has to break down their income of £55,000 in such a way as to minimise tax. The maximum he should take as salary is £8,844 —below the secondary threshold of Employer National Insurance Contribution. The remainder should be allocated as dividends to save NIC and the additional 12.5% tax on salary, the basic tax rate of salary (20%), and the basic tax rate of dividends (7.5%). Let’s understand by calculating the tax charge in the table below. Please note this is only based on one situation; we advise you to speak to your accountant for advice specific to your situation.

| Nature of Income | Amount | Tax Rate | Tax liability |

| Salary | £8,844 | Exempt—Personal Allowance | Nill |

| Personal Allowance | £3,726 | Remaining Personal Allowance | Nill |

| Dividends | £2,000 | Tax-free—Dividend Allowance | Nill |

| Dividends | £37,700 | Dividend Basic Rate Tax—7.5% | £2,827.5 |

| Dividends | £2,730 | Dividend Higher Rate Tax—32.5% | £1,092 |

| Total tax payable | £3,919.5 |

The tax charge calculated on the same amount, using tax rates applicable on salary, increases to £9,432 not considering National Insurance, i.e.

| Nature of Income | Amount | Tax Rate | Tax liability |

| Salary | £12,570 | Exempt—Personal Allowance | Nill |

| Salary | £37,700 | Basic Salary Rate—20% | £7,540 |

| Salary | £4,730 | Higher Rate—40% | £1,892 |

| Total Tax Payable | £9,432 |

The difference between the tax charges resulting from the above two methodologies is £5,513. So, using salary and dividends both at a carefully devised mix can limit the tax outflow materially. Please also note that the Limited Company also pays tax at 19% on the company’s profit before any dividends are paid out. Always model your situation based on a number of scenarios with your accountant before deciding on the most optimal option.

Video: How are Dividends Taxed?

Paying Tax on Dividend Income Up To £10,000

If you are to pay dividend tax on up to £10,000 then you must follow few guidelines as you must notify HMRC and ask them to change your tax code and the tax will be cut from your salaries or pensions making you eligible for the self-assessment tax return. If you have already filled out the self-assessment, then you can skip this step altogether.

Tax on Shares Sold

Shares owned in listed companies in the UK are classified as investment assets, and when they are disposed of with a gain, they can give rise to a Capital Gains tax liability. A capital gains tax allowance of £12,300 is allowed while calculating Capital Gains tax liability; once this allowance is consumed, the following tax rates apply on the leftover gains depending on their respective nature.

| Nature of Asset | Basic Rate/Overall Income<£50,000 | Higher Rate/Overall Income>£50,000 |

| Shares | 10% | 20% |

| Residential Property | 18% | 28% |

| Bitcoin/Cryptocurrency | 10% | 20% |

| Miscellaneous | 20% |

Shares that might give rise to tax upon sale are:

- Non-Investment Saving Account Shares

- Units belonging to a unit trust

- Bonds excluding the Premium Bonds and Qualifying Corporate Bonds

Shares that are exempt from tax:

- Individual savings account or PEP shares

- Shares per employer Share Incentive Plans (SIPS)

- UK government introduced gilts (including Premium Bonds)

- Qualifying Corporate Bonds

- Shares as per employee shareholder schemes, such as Enterprise Management Incentive, etc., depending on the time allotted

Conclusion

Dividends have a lower tax rate compared to paying a salary; this is to promote business activity and investments in businesses. If you are not just a simple investor and are looking to find the most tax-efficient way to extract cash from your business, then a combination of salary and dividends might be the most tax-effective strategy for you and your company. Paying a Salary is also important as it allows you to maintain the qualifying years for state pension, maternity benefits and the ease with which an individual can apply for a mortgage (& insurance policies) and, being a tax allowable expense, a salary cost also reduces the company’s corporation tax.

Additional Resources