A director’s pension is a retirement plan that enables company directors to save for their retirement in a tax-efficient manner.

Director’s pension contributions are deducted either from their wages or can be paid by their companies as direct payments, the directors can also self-fund a pension directly outside their payroll and company. These funds are then invested by the pension fund to grow over time while benefiting from tax reliefs. Lastly, the money in the retirement fund is then used to provide directors with an income in their retirement years, called as a pension draw-down.

This guide will discuss the key points around pension contributions made by limited company directors in line with the current tax year 2025/26, including the types of pension schemes a director can utilise and the types of contributions they can make.

What Are the Types Of Pension Schemes For Directors In The UK?

In the UK, there are three types of pension schemes through which a director can contribute to their pension:

State Pension

The UK State Pension is a regular payment that the government gives to all eligible citizens after they reach State Pension age. Presently, the state pension age is 66 for most citizens. Notably, it is based on your National Insurance (NI) contributions throughout your working life. To claim it, you must reach State Pension age and have at least 10 qualifying years of contributions by paying National Insurance (NI) contributions out of your income.

Private Pension

You or your employer arranges private or personal pensions to save money for your retirement. Under personal pensions, you will receive a pension depending on how much you and your employer contributed to it and how your investments perform.

Workplace Pension

A workplace pension is arranged by your employer, who automatically enrols you in it. Both you and your employer will make contributions under this scheme. As a result of auto-enrolment, contributions are automatically deducted from your wages each month to be paid into your pension pot. Ultimately, after your retirement, you can use your pension funds to meet your everyday expenses.

Understanding Workplace Pension And Auto-Enrolment System

All employers in the UK must provide a workplace pension scheme. It is called ‘automatic enrolment’. Auto-enrolment means that employers automatically enrol eligible employees into the company pension scheme. Consequently, employees do not need to apply actively or ask their employer for it. Auto-enrolment is a government initiative launched to encourage more people to save for retirement.

Who Is Eligible To Be Auto-Enrolled Into A Workplace Pension?

Notably, in line with the UK workplace pension rules, automatic enrolment applies only when:

- You are employed in the UK

- You are classed as a worker (with a contract of employment)

- You are aged between 22 and State Pension age

- Your annual earnings are either £10,000 or above this threshold

It is vital to note that while employees can choose to opt out of the scheme if they want, the initial enrollment is automatic for those who fulfil the criteria.

What Are Pension Contributions Under Auto-Enrolment?

When your employer sets up a workplace pension, you and your employer must make contributions to it every month. Essentially, the minimum contribution that you and your company must pay into a workplace pension includes:

- Your company (employer): 3% of your qualifying earnings.

- You (employee): 5% of your qualifying earnings.

- Hence, the minimum total contribution is 8% of qualifying earnings.

Qualifying earnings include your salary. However, your dividend income does not come under it.

Do Auto-Enrolment Rules Apply to Limited Company Directors?

Generally, the rules of automatic enrolment do not apply to company directors automatically, even if the directors are considered employees. It depends on whether the director is viewed as an employee with a contract of employment. A director must be auto-enrolled only if:

- They are placed under an employment contract with the limited company,

- There is at least one other employee (not necessarily a director) who also holds an employment contract with the company and qualifies for auto-enrolment.

It implies that when the company has several directors but no employees, and at least one or more of the directors have employment contracts, all the directors with employment contracts are classed as employees. Thus, in that case, the company has to run a workplace pension, and the director is auto-enrolled and treated just like any other eligible worker.

Making Personal Pension Contributions as a Director

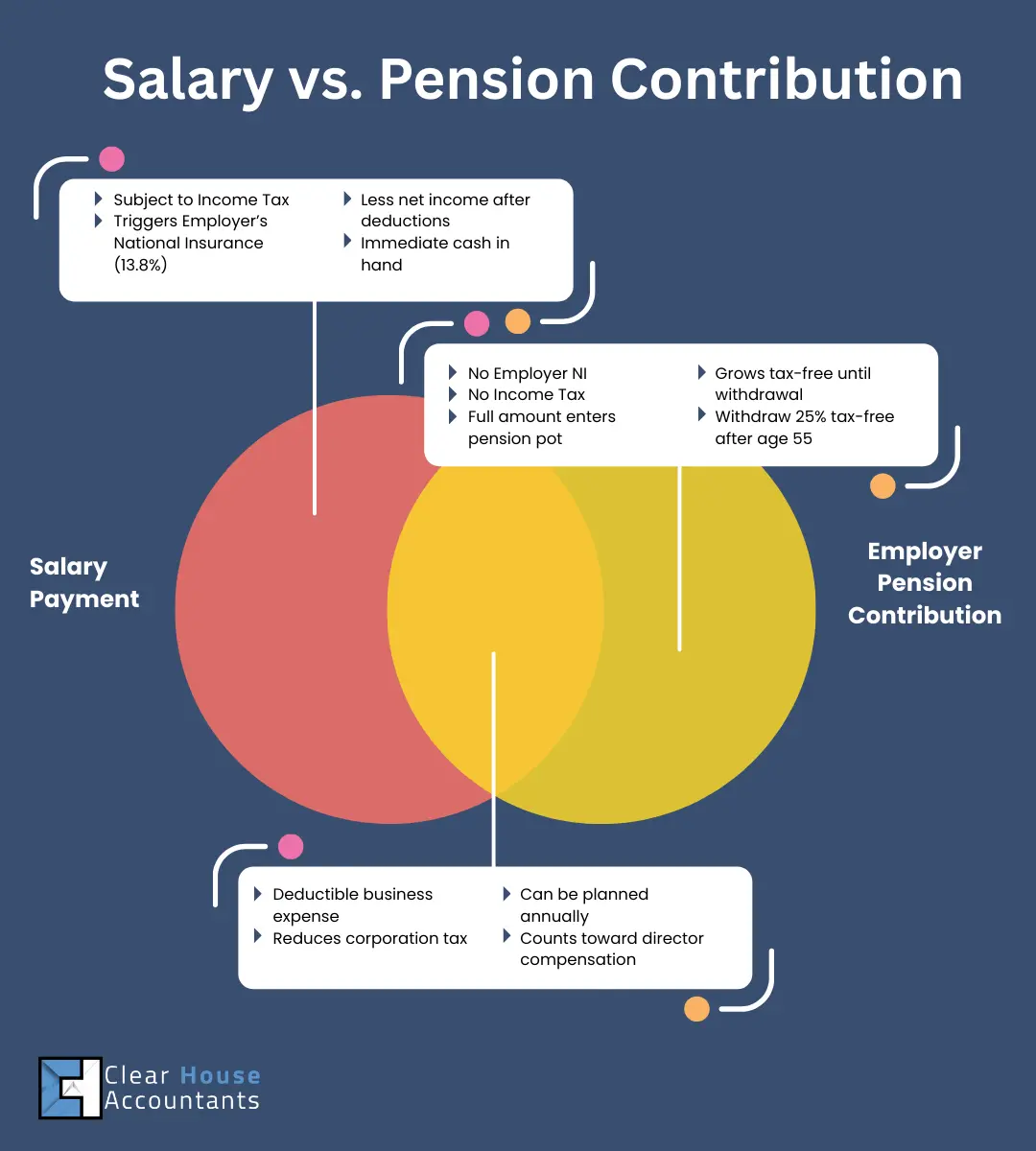

You can make personal contributions to a private pension through your PAYE director’s salary. In most cases, you can pay 100% of your salary into your pension. Further, you can add up to £60,000 into your pension pot in a tax year. Therefore, you and your company can contribute up to £60,000 to your pension(s) per year before you pay tax on it.

More importantly, the government will also benefit you by adding a 20% tax relief bonus on every contribution you make.

A director who is an additional-rate taxpayer are subject to a tapered (reduced) annual allowance for pension on income above a certain amount. To clarify, if your taxable income for the tax year is more than £200,000, your yearly allowance begins to reduce. This reduction process is known as tapering.

Can You Make Director Pension Contributions From Dividend Income?

Since dividends are not considered a part of your salary, you cannot add dividends to your pension as part of your income. However, you can use your dividend income to make additional or separate personal contributions to your pension fund. Making pension contributions from dividend income offers no tax relief, as they are paid from company profits after paying the Corporation Tax. Also, tax is applicable on dividend income beyond the £500 annual dividend allowance.

Making Director Pension Contributions Through a Limited Company

The paramount advantage of making pension contributions directly through your limited company is that the salary threshold and annual pension allowance (£60,000) limit do not restrict the contributions. Subsequently, you can continue receiving a salary of £12,570 and make contributions exceeding £60,000 into your director pension fund in a tax year.

How much can your company contribute to your director’s pension pot?

The highlighting fact here is that you can pay more than £60,000 into your private pension, given that the total pension amount does not surpass your limited company’s annual profits. For example, consider your limited company generates a profit of £55,000 in a tax year. In such a scenario, it will be the maximum amount or the pension limit that your company can contribute to your director’s pension.

Final Thoughts

In the end, if you want to earn profit from your business and amass the much-needed savings for your retirement age, setting up a private pension scheme is the ideal choice to opt for. You can benefit after retirement with your properly planned director pension contributions.

Fortunately, the expert advisors at Clear House accountants are at your disposal to help you find the ideal director pension schemes that fit your circumstances and give comprehensive consultation on how you can maximise the savings while reducing your tax obligations.

Additional Resources