Trusts are very useful for keeping assets safe and managing them. If you are thinking of establishing one, you could be wondering why they are so popular and how they will help your estate or your beneficiaries. Trusts serve various purposes, including tax planning, asset protection, and guaranteeing that your wishes are followed—even long after you are gone. Should you be considering establishing one, here is a summary of the main ideas and advantages you should be aware of.

What is a Trust Fund?

Some people (the settlor) give other people (the trustee) assets, like money held in trust, property in trust, or investments, to manage for the benefit of someone else (the beneficiary). This is called a trust. Although the trustee holds legal title to the assets, investments, or trust property, they have to behave in the best interests of the beneficiaries per the rules set down by the settlor of a trust.

Types of Trusts

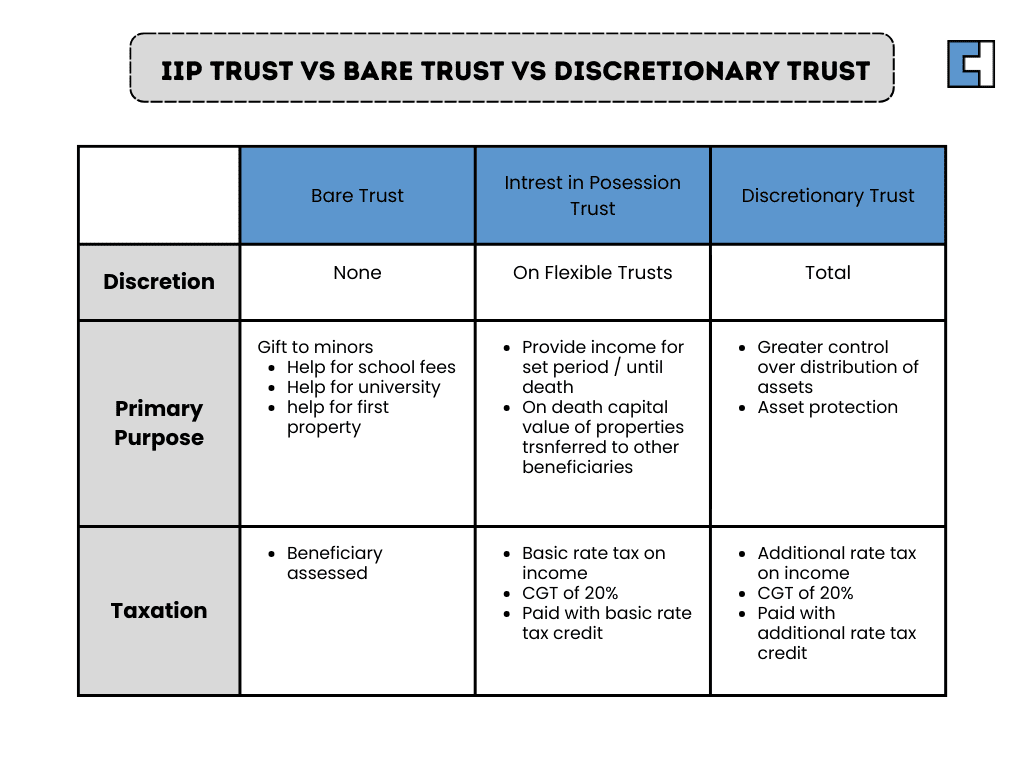

Though there are other forms of trusts, the two most often used ones are interest-in-possession (IIP) trusts and discretionary trusts.

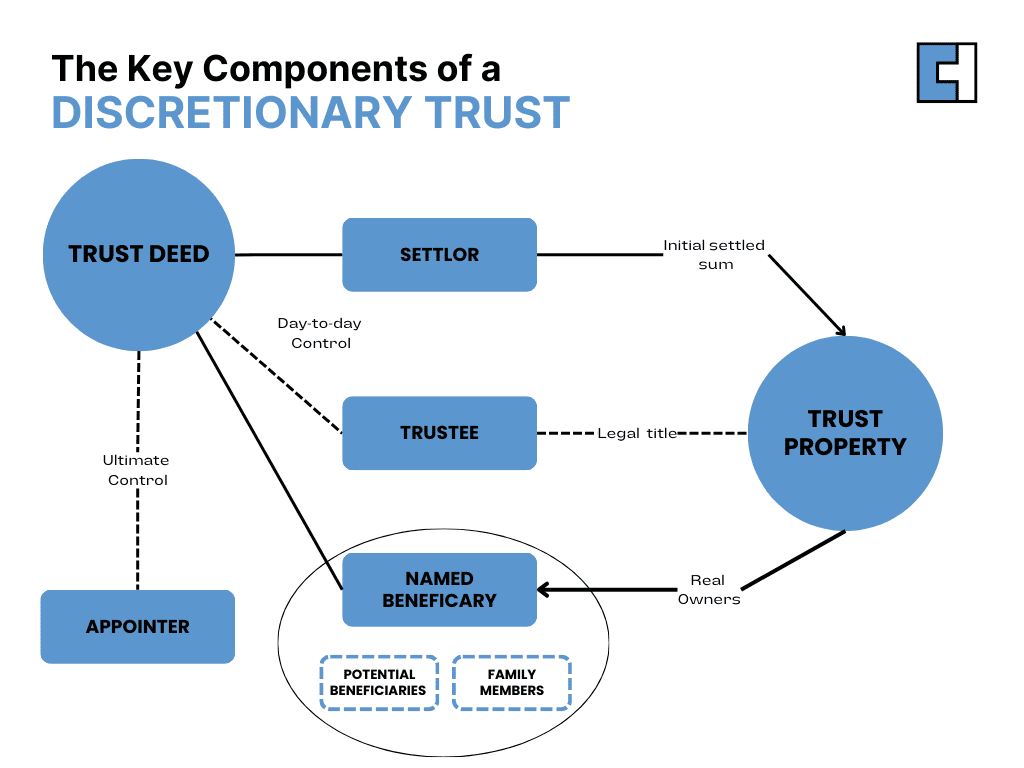

What is a Discretionary Trust?

Discretionary trust meaning a type of trust where the distribution of shares to each beneficiary is not predetermined by the settlor in the trust deed. Instead, the trustees have the authority to decide how the assets are allocated among the beneficiaries. These offer maximum flexibility. Depending on what the settlor wants, the trustee can choose which beneficiaries get the assets and when. When the settlor is not clear about how assets should be divided or if beneficiary circumstances might evolve over time, this adaptability comes in really handy.

Interest in Possession Trust or IIP Trust

Interest in Possession Trust or IIP Trust structure means the trustee and beneficiary control the capital, while a designated beneficiary may instantly get income from the assets. When a settlor wants to make sure a spouse is supported for life and then passes assets to children or another beneficiary upon the spouse’s death, this method of arrangement may be employed.

Other types of trust in the UK are:

- Bare Trusts

- Accumulation Trusts

- Mixed Trusts

- Settlor-Interested Trusts

- Non-Resident Trusts

As the Child Trust Fund scheme was closed in 2011, The Junior ISA account is another option that you can opt for as a family trust.

Why Consider Setting Up a Trust?

For those organising their estates or seeking structured asset management, trusts present a number of convincing advantages.

These are the most often occurring reasons people decide to set one up:

1. Protection of Assets from People or Circumstances

Trusts protect you from risks like beneficiaries making bad financial decisions, divorce settlements, and even creditors. You might want to transmit assets to your kids, but you worry they are too young, unskilled financially, or in unhealthy relationships. A trust can make sure that the assets are safe and that they are only given to the children when they are old enough to handle them properly.

Trusts can also help to stop events including family conflicts, remarriage, or legal claims causing assets to be lost.

2. Control Over How and When Beneficiaries Receive Assets

Using trusts is one of the key benefits in that it allows one to control the distribution of assets and, hence, their timing. Unlike giving assets immediately, which gives the beneficiary instant power, a trust lets the settlor decide when and under what circumstances assets should be given. This is very helpful to guarantee that resources are applied for specific uses, such as financing education or saving money for the next generations.

3. Tax Planning and Efficiency

Although trusts used to be more usually connected with tax avoidance, current legislation has cut the tax benefits for many different kinds of trusts. Still, they can offer considerable tax relief, especially in relation to trust Inheritance Tax (IHT) and Capital Gains Tax (CGT). Trusts, for instance, let you place assets under the tax-free allowance (the nil-rate band), therefore helping to lower the IHT load provided specific requirements are satisfied.

Many people include trusts within a more general estate planning scheme to reduce the tax load for their beneficiaries. Setting up a trust, however, may not always result in appreciable tax savings immediately. Evaluating how a trust might meet your particular tax circumstances depends on working with a personal tax accountant or a lawyer.

4. Flexibility to Adapt to Changing Circumstances

Life is erratic, hence a trust gives flexibility to fit unexpected developments. Whether it’s a family matter or legislative changes to taxes, a well-organised trust lets you make changes without having to overhaul your whole estate plan. This is particularly true with discretionary trusts, where trustees have the power to change asset allocation in response to beneficiary present demands.

5. Privacy and Confidentiality

Trusts allow more privacy than wills, which are public records following death. A trust protects your assets and beneficiaries by not requiring public disclosure of its contents, therefore safeguarding their confidentiality. For persons with high net-worth or those who value secrecy, this can especially be crucial.

Costs and Considerations of Setting Up a Trust

Though trusts have many advantages, maintaining and putting them up can be costly. Particularly if they must handle complicated assets or investments, trustees may also collect fees for running the trust. Professional advice is also quite important and can help to lower starting setup expenses.

Additionally, depending on the type, there may be tax charges that apply. For example, certain types are subject to ongoing charges on their ten-year anniversary and an Inheritance Tax charge when the value of assets transferred into the trust exceeds the nil-rate band.

People who are thinking about setting up an offshore trust usually have slightly different reasons. For them, privacy and tax benefits are the main reasons.

The Role of Trustees

When establishing a trust, selecting the appropriate trustee is among the most important choices one makes. Managing the assets and carrying out settlor wishes will fall to the trustee. While many people name a close friend or relative, professional trustees including solicitors or accountants are also somewhat frequent. Although they will probably fee for their services, a professional trustee can offer experience and objectivity.

Should You Set Up a Trust?

Your objectives for your assets and beneficiaries will determine whether or not you want to create a trust—a very personal matter. Though they call for careful planning and legal knowledge, they can be great tools for asset preservation, tax efficiency, and control. Dealing closely with a legal counsel or financial planner who fits your particular circumstances can help to guarantee that it is set up properly and satisfies your long-term goals.

Finally, they can give you peace of mind by ensuring that your assets are managed the way you want them to be, even if you can’t do it yourself. Whether your estate planning calls for flexibility, safeguarding loved ones, or future generations, it could be a crucial component of your approach.

Additional Resources

Most Asked Questions

What is a bare trust?

A bare trust is a type of trust in which assets are held in the name of a trustee, but the beneficiary has the right to the entire capital and income of the trust as soon as they reach a certain age—18 or over in England and Wales, or 16 or over in Scotland. This ensures that the assets designated by the settlor will go directly to the intended beneficiary without any conditions.

When does a trust become liable for tax?

A trust becomes liable for tax when it earns income (like rent or interest), sells assets for a profit (capital gains tax), or when assets are transferred (inheritance tax). Trustees are responsible for handling these tax payments, and the rates depend on the type of it and local tax laws.