In the UK, the terms creditors and debtors hold great significance in scrutinising a company’s financial position and relationships. In simple terms, creditors are individuals or entities to whom a business owes money. Usually, creditors provide companies with goods or services on credit. In contrast, debtors are those who owe money to the business. These two terms might apparently look easy to understand, but they are vital for companies to manage their cash flow effectively and ensure business continuity.

Accordingly, this blog brings to the fore the essentials of creditors and debtors in the UK, including their meanings, types, significance, and how businesses should handle them to ensure their operations are carried out smoothly without compromising their reputation.

Learning Debtors And Creditors Meaning

It is hugely important for a business owner to understand the meaning of creditors and debtors to understand the practicalities of applying the two terms.

What Is A Creditor?

Creditors, also known as accounts payable, are individuals or institutions to which a business owes money. In simple terms, creditors are called the lenders or suppliers.

Creditors are individuals, businesses, or organisations (i.e., banks) that you owe money to because they have provided goods or services or loaned money to your business. For instance, they have offered you credit and expect you to repay the amount at a later time.

What Is A Debtor?

A debtor is a person, a business, or any other entity that owes money to another business. They are often referred to as accounts receivable. When you sell goods or services to people or companies on credit, they become your debtors since they owe you a debt (your business money).

Generally, debtors pay their debts through an agreed-upon payment plan. This payment plan can be carried out in any feasible manner, i.e., from two to three large lump sums to several smaller payments made every month over a few years. Furthermore, you can include interest as part of the payment deal.

Understanding Debtors And Creditors In The Balance Sheet

Debtors on the balance sheet usually owe money to your business. The debtor to a company can vary, such as it can be a single person, a big or small business, or even a government institution such as HMRC.

On the other hand, creditors on the balance sheet reflect the parties lending money to your business. In addition, creditors are categorised under current liabilities and non-current liabilities on the balance sheet.

What Are The Types Of Creditors And Debtors?

There are different types of creditors and debtors that companies should know to keep the distinction between them:

Types Of Creditors

Primarily, there are two main types of creditors: trade creditors and loan creditors.

Trade Creditors

These are suppliers or vendors who extend goods or services to customers on credit. A trade creditor is an entity to whom you owe money.

For instance, a brick supplier will be classed as a trade creditor for providing bricks to a construction company without upfront payment. Now, the building contractor will owe money to the brick supplier and make the payment at a later date.

Loan Creditors

Loan creditors are generally composed of banks, building societies, and other financial institutions that lend money to businesses in various forms, such as overdrafts, loans, and credit cards. When a financial institution, say a bank, lends your company funds for expansion or operations, the bank is your creditor until you repay the loan.

Types Of Debtors

The following are the types of debtors:

Trade Debtors

A trade debtor refers to customers or businesses that have received services or products but have not yet paid for them. For example, a furniture manufacturer waiting for payment from retailers who have received its products is dealing with trade debtors.

Staff Loans

Some companies offer employees loans with interest rates lower than those in financial institutions. These are called staff loans. Alternatively, a staff loan is a preferential loan that the employer gives to an employee, making the employee a debtor to the business.

Key Distinctions

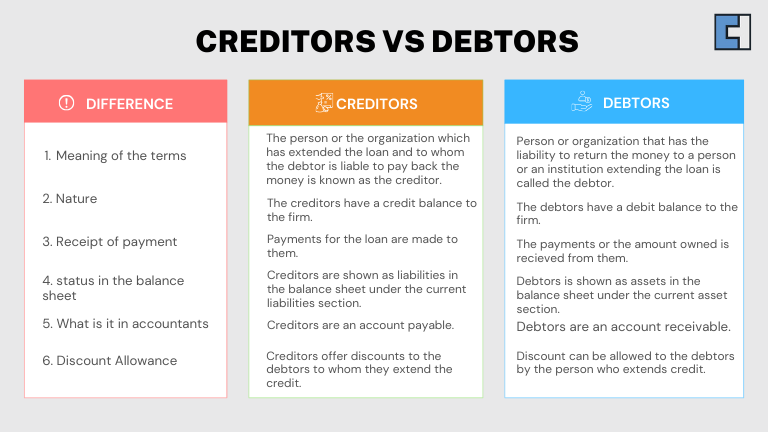

What Is The Difference Between Creditors And Debtors?

Creditors and debtors might seem like simple terms, but the practicalities of applying these two terms can be mind-boggling, and this is mostly the case if you are running a company. Basic differences are in various factors, including their meanings, nature, receipt of payment, their statuses in the balance sheet, and control of discount allowances.

What is the Difference between Suppliers and Creditors?

While comprehending the concept of creditors and debtors, it is equally important to understand the distinction between suppliers and creditors clearly. Generally, the primary difference is in the roles of suppliers and creditors.

The suppliers mainly deliver the products that are essential for carrying out a company’s daily operations, allowing it to manufacture and sell goods or provide services. On the contrary, the chief focus of creditors is to offer a wide range of resources, which are not limited to products alone. However, suppliers can become creditors if they extend credit to the business.

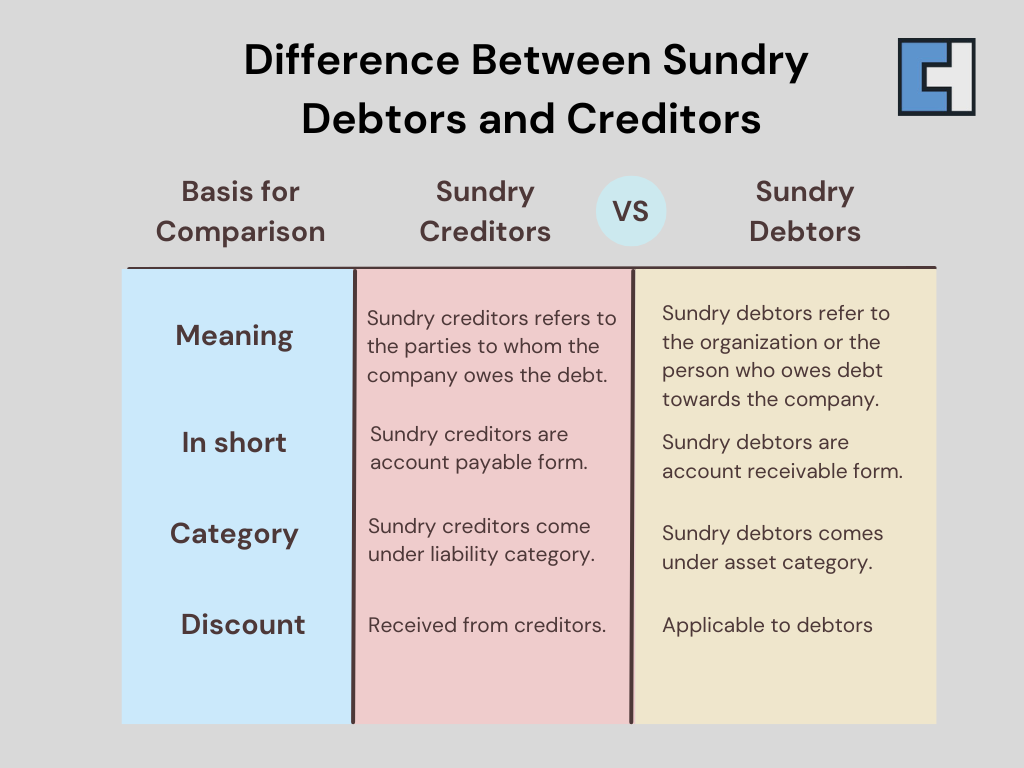

What Are Sundry Creditors And Sundry Debtors?

In brief, sundry debtors are companies or entities that owe money to another business or company for the goods and services acquired on credit. They are external parties (often called accounts payable) to whom a company owes, and they are listed under a company’s liability account.

The creditor’s account on the balance sheet shows the total amount a business owes for goods it has bought but not yet paid for. In contrast, sundry creditors represent individual accounts owed to different suppliers or vendors for purchases.

In comparison, sundry creditors are entities, companies, or businesses that provide goods and services to another company without immediate payment, expecting to be paid later according to agreed-upon terms. Sundry debtors are often distinct from a company’s regular customers since they can be individuals or businesses who have purchased something on a one-time basis or used a specific service that incurs a fee.

What Are Creditors’ And Debtors’ Days?

Debtor days and creditor days are crucial parameters that companies must take into account for managing financial relationships within a business. Debtor days measure how long it takes a company to collect payments from its customers. In contrast, creditor days represent the time it takes a company to pay its suppliers. Now, having an adequate understanding of how to calculate creditor and debtor days can considerably help business owners in effective cash flow management.

Creditors Days

The creditor payment period, or the creditor days, is used to measure a company’s creditworthiness and reputation to a certain degree. Creditor days determine the latitude allowed by its suppliers and creditors. It also reflects the value that both parties put on the business conducted and demonstrates the company’s cash flow and the extent to which it will go to finance its business with its debt.

Monitoring these metrics ensures that a business can maintain a healthy balance between incoming and outgoing funds, helping to identify the liquidity ratio, avoid liquidity issues and optimise financial stability.

What are Trade Creditors Days?

Trade creditor days represent the average number of days a company takes to settle its invoices with its suppliers.

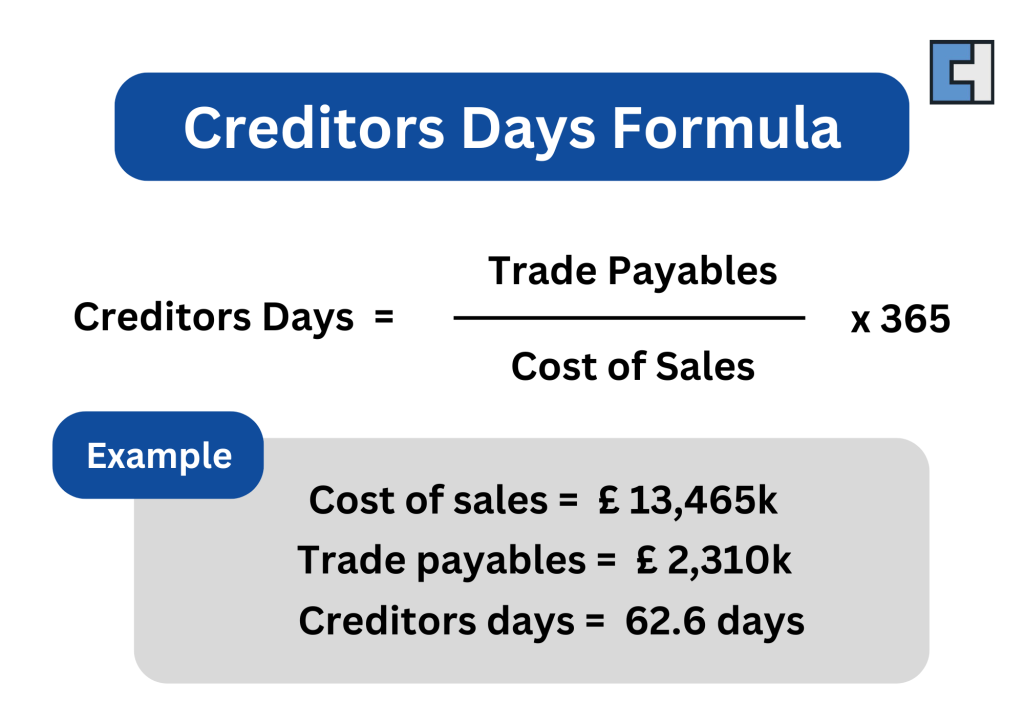

How to Calculate Creditor Days?

The calculation of creditor days involves dividing the trade creditors shown in a company’s accounts by its cost of sales and then multiplying the result by 365. This calculation provides insight into how long, on average, it takes the company to pay its trade creditors.

Dividing the total debt by sales revenue and multiplying the answer by 365 will calculate creditor days. A debt of £800,000 with sales revenue of £9 million will be calculated like this –

(800,000/9,000,000) x 365 = 32.44 creditor days

Debtor Days

Debtor days are used to indicate how efficiently a company invoices goods or services and collects from its customers. Fewer debtor days are better for a company. Payment delays tell a company that its customers have cash flow issues or are facing problems. Due to their size and power, such as big supermarket chains, they might be overstocked or held to ransom by some of their customers. These types of customers usually fall victim to harsh credit terms and lower service levels.

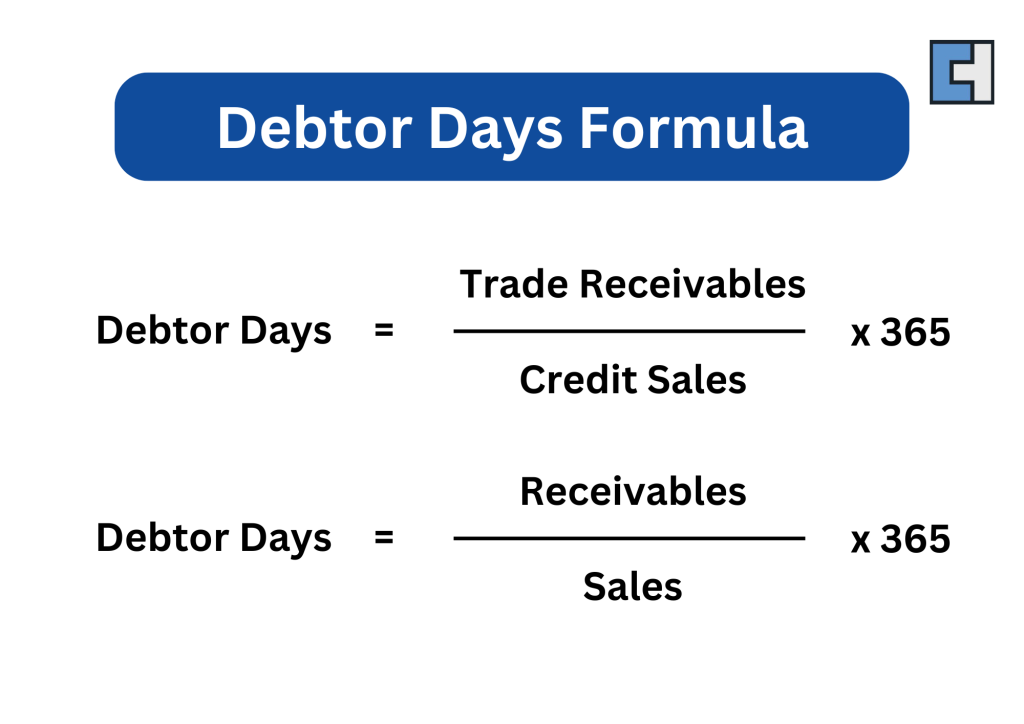

How to Calculate Debtor Days?

For the calculation of debtor days, divide the total outstanding debt by sales revenue and multiply the answer by 365 to calculate debtor days. Outstanding debt of £600,000 with a sales revenue of £9 million will be calculated like this –

(600,000/9,000,000) x 365 = 24.33 debtor days

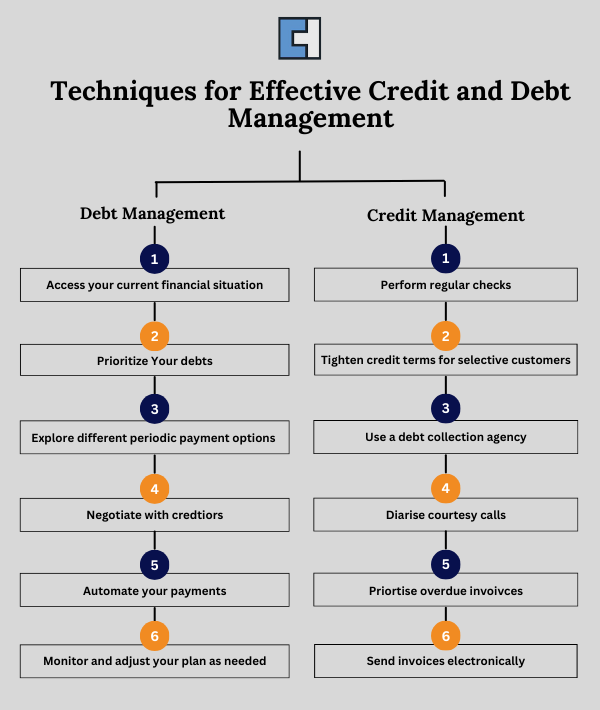

Why Is Managing Transactions Important?

Undeniably, all the transactions involving goods and services hold great significance for the operations of a business. A business owner must manage these transactions efficiently to ensure that both parties fulfil their obligations on time. Handling transactions between creditors and debtors helps maintain strong business relationships and keeps balance sheet liabilities manageable for companies.

Why Cash Flow Management Is Crucial For Creditors And Debtors?

Cash flow management is of utmost importance for both debtors and creditors. A business must ensure it receives payments from its debtors on time to maintain positive cash flow. Also, it must manage its outflows to creditors so it does not end up becoming a debtor itself and for balanced cash flow. Managing business creditors and debtors of the company provides a clear picture of the company’s assets and liabilities.

Conclusion

Overall, business transactions in the UK have two parties involved: the creditor (lender) and the debtor (borrower). A creditor is someone who lends money, while a debtor is someone who owes money to a creditor. A company must keep track of the time lag between receiving payments from the debtors and paying the money to the creditors to maintain a steady cash flow of working capital.

Hiring accountants is a great way to ensure that your creditors and debtors are managed properly without devoting extra resources to managing them in the future.

In this connection, Clear House Accountants are skilled and certified accountants in London who recognise how tedious it might become for one to understand the various accounting and business terminologies involved in running a business. Helpfully, our team of dedicated accountants has prepared highly effective and concise guides to make things less complicated and more manageable for you. Thus, if you are looking for any advice or are stuck at some point in your business, please do not hesitate to contact us.