The Landlord and Tenant Act 1985 is a significant legislation governing the relationship between landlords and tenants in the UK. It puts in place guidelines for landlords and tenants to ensure tenants’ rights are protected while landlords meet their obligations when managing properties. Furthermore, one key section of this act is Section 20, which specifically discusses fulfilling the consultation requirements when performing major works in leasehold properties. This blog explains the three stages of the Section 20 consultation process, when it is applicable, and its objectives.

What do you need to know about section 20 of the Landlord and Tenant Act (1985)?

Section 20 of the Landlord and Tenant Act 1985 is a UK legislation that places certain requirements on landlords. As part of these requirements, landlords must consult with their tenants before carrying out certain types of qualifying works or entering into long-term agreements with liable leaseholders. Liable leaseholders pay a variable service charge to cover the costs of a building/property.

Notably, when major works on a building are carried out and the cost per leaseholder exceeds £250, the leaseholder has certain rights under Section 20 which have to be followed by the landlords for the price to be claimable from the leaseholder. Moreover, during the consultation process, the freeholders are required to provide the tenants with the details of the proposed works, the estimated costs, and the contractors involved. However, if the landlord fails to follow the proper procedure, tenants may not be liable for paying the full amount of service charges for the work.

What Is The Main Objective Of Section 20 Of the Landlord And Tenant Act 1985?

The basic purpose of issuing a section 20 is to put in place a consultation process with which to notify the leaseholders about the major work costs affecting their homes. In addition, this law aims to keep the tenants or the leaseholders well informed of any works that can have a significant impact on the property’s value or the tenant’s quality of life. For instance, any tenant must be consulted over any modification, renovation, or repairs being done to their properties, along with the consideration of their consent. Ultimately, the Section 20 consultation process ensures there is complete transparency and fairness when landlords pass on costs to tenants.

When Do The Consultation Requirements Of Section 20 Apply?

A landlord must consult with tenants before:

- Undertaking qualifying works that will result in the individual leaseholder (or tenant) contributing more than £250 to the cost of the works.

- Entering into a long-term agreement that costs the tenant more than £100 in any 12 months of the agreement.

Furthermore, the Section 20 consultation requirements apply to all dwellings and residential leases, including flats, where tenants are required to pay service charges.

Similar to Section 20, the 18-month rule of Section 20b is also essential in understanding the dynamics of service charges between landlords and leaseholders. To learn more about it, read the following guide:

Understanding the Section 20 consultation procedure

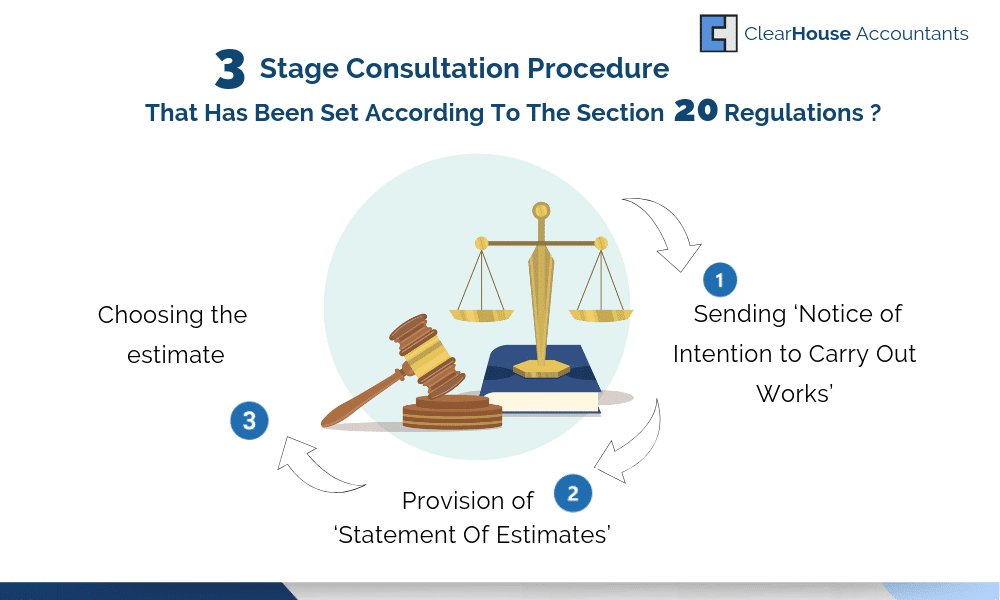

A three-stage consultation procedure has been set according to the section 20 regulation. Essentially, the residential management company (RMC), property management company, or Right to manage (RTM) company must follow this procedure if they want to carry out qualifying works to the apartment/building where the contribution (payment to service charges) from any one of the leaseholders goes beyond £250 or exceeds £100 in a financial year, given a qualifying long-term agreement is in place. Moreover, consultation with all leaseholders is required if the RMC plans to carry out qualifying works or enter into a long-term contract. They must also include any Recognised Tenants Association (RTA) if applicable.

It is noteworthy that a Service Charge Accounting firm can provide valuable help on all major work projects, in preparing a detailed CAPEX, feasibility report, and correctly recording the transactions in the service charge accounts.

Learn more about the Right to Manage Company by referring to the following guide:

What are the three stages of the consultation procedure?

The consultation procedure can be divided into three stages:

- Sending ‘Notice of Intention to Carry Out Works’

- Provision of ‘Statement of Estimates’

- Notice of Reasons

Sending ‘Notice of Intention to Carry Out Works’

According to section 20, ‘Notice of Intention to Carry out Works’ will be sent to all of the leaseholders. The notice must state and elaborate on the proposed work, the reasons behind it, and include an invitation to leaseholders to submit written observations within 30 days. The notice should also include the correspondence address for observations.

Leaseholders are provided with an opportunity to give the name of the desired contractor with whom the RMC can contact and acquire an estimate for the proposed works.

Provision of ‘Statement of Estimates ‘

Two estimates should be acquired, with one of these estimates given by a person who is completely independent of the residential management company (RMC) or the landlord, after the expiration of the consultation period of 30 days.

However, at least one estimate should be acquired from the nominations, only if the nominations were made during the period of consultation.

Next, the residential management company (RMC) or the landlord must list down all the details related to the estimates that have been acquired, along with the summary of observations obtained within the period of consultation, in the ‘Statement of Estimates’ and must ensure its provision. All the estimates, along with the estimates provided by the nominated contractor, must be available for the leaseholders so that they can investigate if they want to.

Lastly, it is important to send a ‘Notice to Accompany the Statement of Estimates’ along with the ‘Statement of Estimates.

For greater clarity, the ‘Notice to Accompany the statement of Estimates includes the details of:

- Time and location where the details may be investigated.

- An invitation to the leaseholders to record written observations made on estimates within a period of 30 days, and

- The address to which the recorded observations should be sent.

Sending ‘Notice of Reasons’

A ‘Notice of Reasons’ is to be delivered to all the leaseholders if the chosen contractor, through this process, fails to provide the lowest possible estimate within the period of consultation. ‘Notice of reasons’ lists down the reasons given by the residential management company (RMC) or the landlord for choosing the contractor.

Though the requirements of section 20 have been met, it is wise to issue a ‘Notice of Reason’ so that the estimate’s reasonableness could be tested according to Section 19 of the Landlord & Tenant Act by the First-tier Tribunal (FTT).

To learn more about the dynamics of the First-Tier Tribunal, read:

Bottom Line

All in all, understanding the workings of the Section 20 consultation process is tremendously important for leaseholders, as it ensures they are informed and involved in decisions that could affect their finances. By requiring consultation for significant costs spent on major works, Section 20 of the Landlord and Tenant Act 1985 promotes fairness and protects tenants from bearing unexpected financial burdens. Although understanding this section is vital for both leaseholders and landlords to ensure compliance and avoid unnecessary disputes, dealing with its technicalities might not be smooth sailing for everyone.

To your relief, Clear House Accountants are specialist and leading Service Charge Accountants, who work with a large number of RMCs, RTMs, Property Management Companies, and Landlords.

Additional Resources: