Details of Pension for Contractors and Its Working

If you are employed in an established firm or serving as a government employee in the UK, then there is not a lot to worry about in relation to your taxes and pensions, as they are sorted out at source. However, if you are providing contracting services as a contractor in the UK, you will have to fulfil most of the obligations yourself.

Though contractors have the benefit of additional flexibility and higher levels of income compared to employees within a similar role, they do have added stress due to the extra tax and compliance responsibilities.

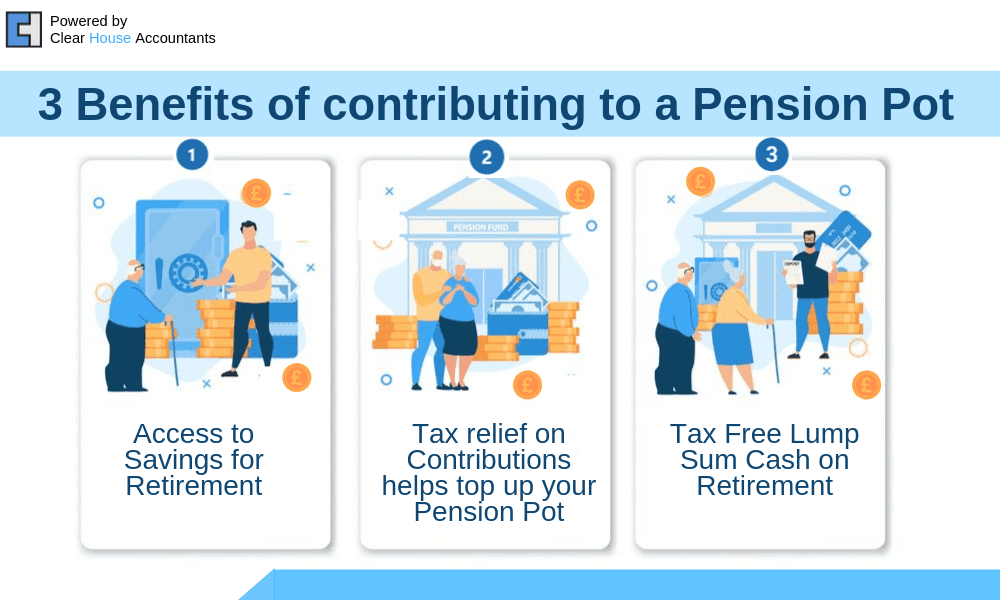

Whilst many contractors focus on their current earnings and work out their taxes accordingly, few pay attention to the prospects of investing in a pension fund. Pension not only has the potential to provide substantial tax relief, but it also has the potential to leave the contractors with more money to spend after retirement. Contractors have the opportunity to contribute to a pension fund to reduce the amount of tax they have to pay.

Facts About Pension Savings for Contractors

- For the 2026/27 tax year, most contractors have an Annual Allowance of up to £60,000. However, it is important to note that if you have already started drawing from your pension flexibly, a Money Purchase Annual Allowance (MPAA) of £10,000 may apply instead. High earners (with an adjusted income over £260,000) may also see their allowance tapered down to a minimum of £10,000.

- 25% of your pension pot can usually be taken as a tax-free lump sum, which is currently capped at a maximum of £268,275 (Lump Sum Allowance), with the remaining 75% taxed as income.

- Family members of the contractors can get access to their pension on their death before the age of 75, given that no annuity has been bought.

- Pension funds are protected from insolvency by law, hence your pension savings will be secure

- If the contractor is a risk-averse individual, they can keep their pension pot in cash, similar to an ISA.

Contractors, business owners and employees are required to pay tax on the income earned. However, if they decide to invest a certain proportion of their total income into a pension fund, they can save money in the form of tax relief.

There are two ways through which contractors can invest their funds into a pension fund, either by investing personally or through their business. Contractors who don’t have any pension set up and are not paying much attention towards the contributions and available tax reliefs are potentially losing money through potential high amounts of taxation.

Speak to your Contractor Accountant to see the potential savings you can achieve by contributing to a pension scheme.

What if You Are Within IR-35

If you are working ‘Inside IR35’, your tax is typically handled via the off-payroll working rules. While the old 5% expense allowance is now largely restricted, pension contributions remain one of the most effective ways to reduce your tax liability. Contractors can contribute up to £60,000 annually to their pension, which is deducted before tax is calculated, providing significant relief.

How Does Tax Relief Work?

Let us consider an example of a contractor working through a limited company; the individual takes a small tax-free salary and receives the remainder in the form of dividends. This contractor falls outside the scope of IR-35 and is a higher-rate taxpayer based on the total earnings. Let us consider two scenarios to understand how the tax relief for pension contributions would work.

In the first scenario, the contractor decides to take the income instead of contributing to a pension fund. For every £100 generated as profits, the company may be liable for Corporation Tax ranging from 19% to 25%, depending on the profit levels. By contributing directly to a pension, this amount is treated as a business expense, potentially saving the company up to 25% in tax. If the contractor contributed to a pension fund, the amount would be a tax allowable cost, reducing the corporation tax payable.

In the second scenario, the contractor gets a contribution made on their behalf to a pension fund from their limited company budget. The contribution amount is tax allowable, which means lower corporation tax; the amount contributed also grows with time.

Tax relief is basically the percentage of tax saved- in this case, the amount of cash deposited into the pension fund instead of paying out as tax to the concerned authorities. It’s safe to conclude that the contractor was successfully able to enjoy a huge tax relief when contributing to a pension fund. This also provides him with security for the future when he retires.

Selecting a Pension Provider

Contractors have the flexibility to control the amounts of their contributions, but they need a provider who can cope with these requirements. Furthermore, the provider needs to be a well-recognised one so as to ensure the provider does not disappear. It might be a good idea to ask your contractor accountants to refer a financial adviser who can help you set up the most lucrative pension scheme.

Clear House Accountants are specialist Accountants in London for business, who have been working with contractors from a variety of industries, helping them save money and reduce the amount of tax they pay.

Additional Resources